Executive Summary

Do I get paid for my stock options if my company goes bankrupt?

Usually not in the way employees hope. In liquidation, common equity is last in priority after secured debt, unsecured creditors, and preferred stock. Options are contractual rights—not ownership of assets—so they may expire worthless if the underlying stock has no value or the plan is terminated under bankruptcy.

Are my unvested RSUs safe in Chapter 11?

Unvested awards are often subject to cancellation, amendment, or assumption by a debtor-in-possession or buyer as part of a restructuring. Treat unvested equity as highly uncertain once insolvency is probable—read your plan’s change-of-control and forfeiture provisions.

What should I do first if bankruptcy is announced?

Gather grant agreements, confirm post-termination exercise windows for vested options, and avoid relying on verbal HR summaries. If you hold shares, understand whether they are freely tradable or restricted. Consult securities and employment counsel for deadlines—especially ISO 90-day rules after job loss.

Bankruptcy is a legal process for resolving claims against a company, not a fairness mechanism for employees. Equity compensation sits in a fragile position: it is often not “money owed to you” like unpaid wages (which can have priority in some cases) but contractual and securities rights that can evaporate when the enterprise value goes to zero or the plan is rejected.

This guide explains typical patterns for U.S. employees holding options, RSUs, or shares—not legal advice for your specific case.

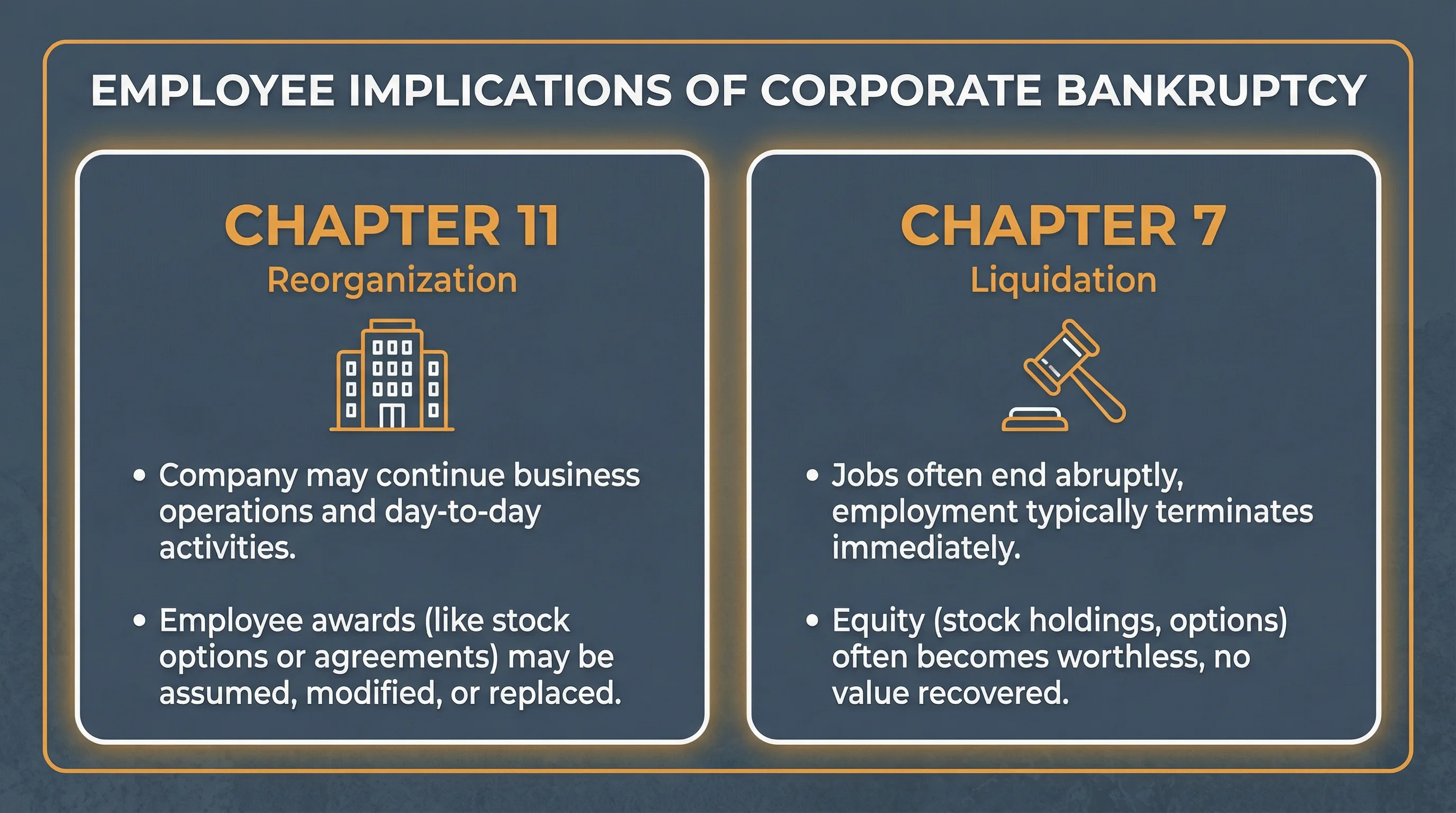

Chapter 7 vs Chapter 11 (High Level)

| Chapter | Common pattern | Employee equity angle |

|---|---|---|

| Chapter 11 | Reorganization; company may keep operating | Awards may be assumed, replaced, or terminated; jobs may survive |

| Chapter 7 | Liquidation; assets sold, entity winds down | Employment often ends; equity often worthless; strict timelines |

Why this matters: In Chapter 11, you might see new equity, RSU replacement, or key employee retention packages approved by the court. In Chapter 7, there is often no continuing employer to administer a stock plan.

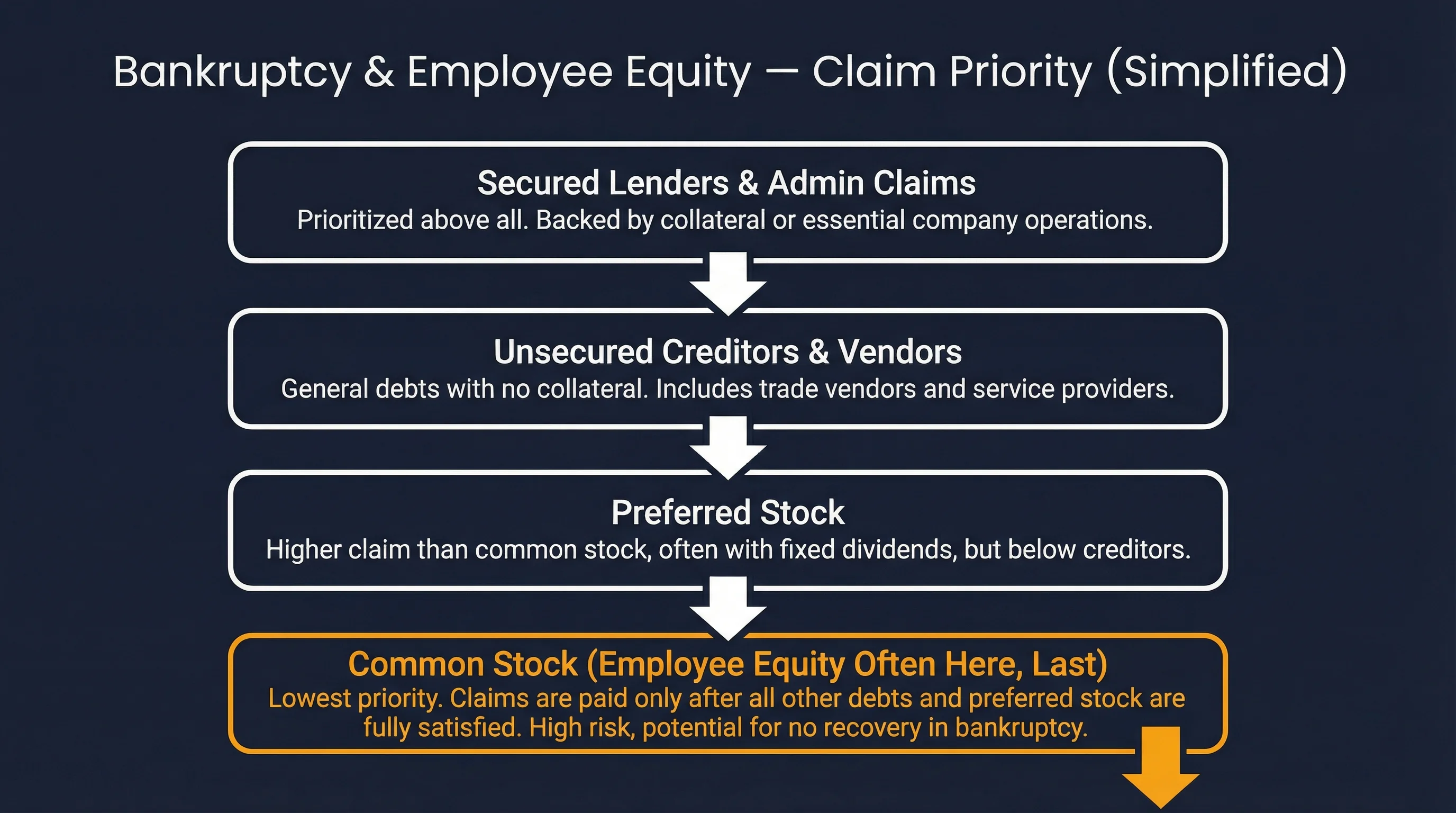

Figure 1: Claim priority is not tax advice—illustrates why common equity can be last in line.

How Claims and Capital Structure Interact (Simplified)

| Priority (very simplified) | Examples |

|---|---|

| Higher | Secured lenders, administrative expenses |

| Middle | Unsecured creditors, vendors, some bondholders |

| Lower | Preferred equity |

| Often last | Common stock (typical startup employee equity) |

If you only hold options, you are not a shareholder until you exercise. If the share price is zero or the plan is gone, exercise may be pointless even if the window is technically open.

Figure 2: Chapter 11 vs Chapter 7—different paths for operations and equity administration.

Stock Options in Bankruptcy

Vested options

- Cash to exercise: You may need to pay strike price and consider tax consequences—see our ISO vs NSO guide.

- ISO 90-day rule: If employment ends due to liquidation, your post-termination exercise window may be short—confirm plan terms immediately. See leaving your job.

Unvested options

- Often forfeited upon termination or plan termination unless a court-approved program says otherwise.

Net exercise / cashless

- If available pre-bankruptcy, mechanics may freeze—our net exercise calculator helps with economics, not legal availability.

RSUs in Bankruptcy

RSUs are promises to issue shares (or cash) on vesting. In distress:

- Unvested RSUs may be cancelled or replaced.

- Vested but unsettled RSUs may be caught in administration—confirm whether shares were actually delivered.

Pair with RSU tax guide for tax timing (vesting as wages when settled).

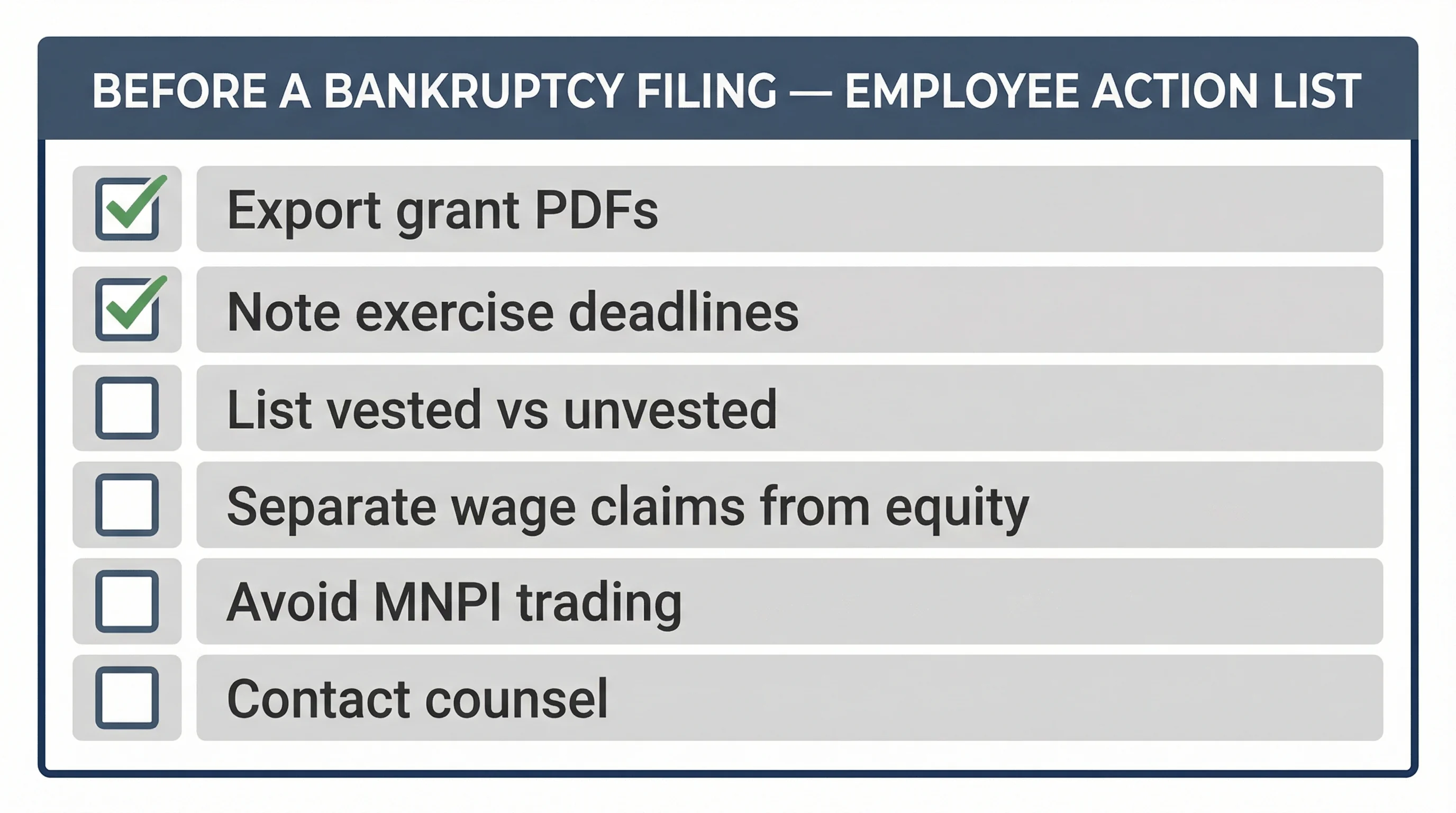

Figure 3: Documentation and deadlines matter more when plans are in flux.

If You Already Own Shares

Common stockholders may receive only residual value after all senior claims. In many startup wipeouts, residual is zero.

Also consider trading restrictions, lockups, and insider rules—bankruptcy does not automatically make restricted stock freely salable.

Tax and Accounting (Overview)

Bankruptcy itself does not create a magical tax event for unexercised options. Worthless stock and capital losses have specific rules—consult a CPA if you paid for shares or have basis.

Checklist: Before and After a Filing

- Export grant confirmations and plan documents

- Identify vesting and exercise deadlines

- List shares owned vs unvested awards

- Note any WARN notices, severance, or employee claims separately from equity

- Avoid insider trading if you have MNPI—coordinate with counsel

FAQ

Is unpaid salary the same as equity in bankruptcy?

Often no—wage claims can have different treatment than securities. Verify with counsel.

Can a buyer save my equity?

Sometimes—in M&A or 363 sales, new equity grants appear. See M&A equity guide.

Does bankruptcy erase my tax on past RSU vests?

No—prior wage income remains taxable; bankruptcy generally does not “undo” settled tax years.

Disclaimer

This article is educational and not legal, tax, or investment advice. Bankruptcy outcomes depend on the plan, jurisdiction, and court. Consult employment and securities counsel for deadlines affecting your rights.

Primary sources

| Source | URL |

|---|---|

| U.S. Courts — Bankruptcy Basics | https://www.uscourts.gov/services-forms/bankruptcy/bankruptcy-basics |

| SEC — Corporate Bankruptcy | https://www.investor.gov/introduction-investing/investing-basics/glossary/corporate-bankruptcy |