Executive Summary

What happens to my stock options when I leave my job?

Vested stock options must be exercised within a post-termination window—typically 90 days—or they expire and become worthless. Unvested options are forfeited. RSUs that have already vested are yours to keep; unvested RSUs are forfeited. Check your plan documents for exact deadlines and any good-leaver provisions that may extend your exercise period.

Leaving a job is stressful enough without the added pressure of equity deadlines. Yet thousands of employees each year forfeit valuable options simply because they didn't know—or didn't act in time. The rules vary by company, but the stakes are high: a 90-day window can mean the difference between keeping $50,000+ in equity or losing it forever.1

The bottom line: Your vested options have an expiration date the moment you leave. Unvested equity is gone. Plan your exit with these deadlines in mind, and model the cash and tax impact before you give notice.2

Critical Warning: The 90-day post-termination exercise window is common but not universal. Some plans offer only 30 days or immediate expiration upon termination. Always verify your plan's exact terms before making career decisions.3

Stock Options: The Post-Termination Clock

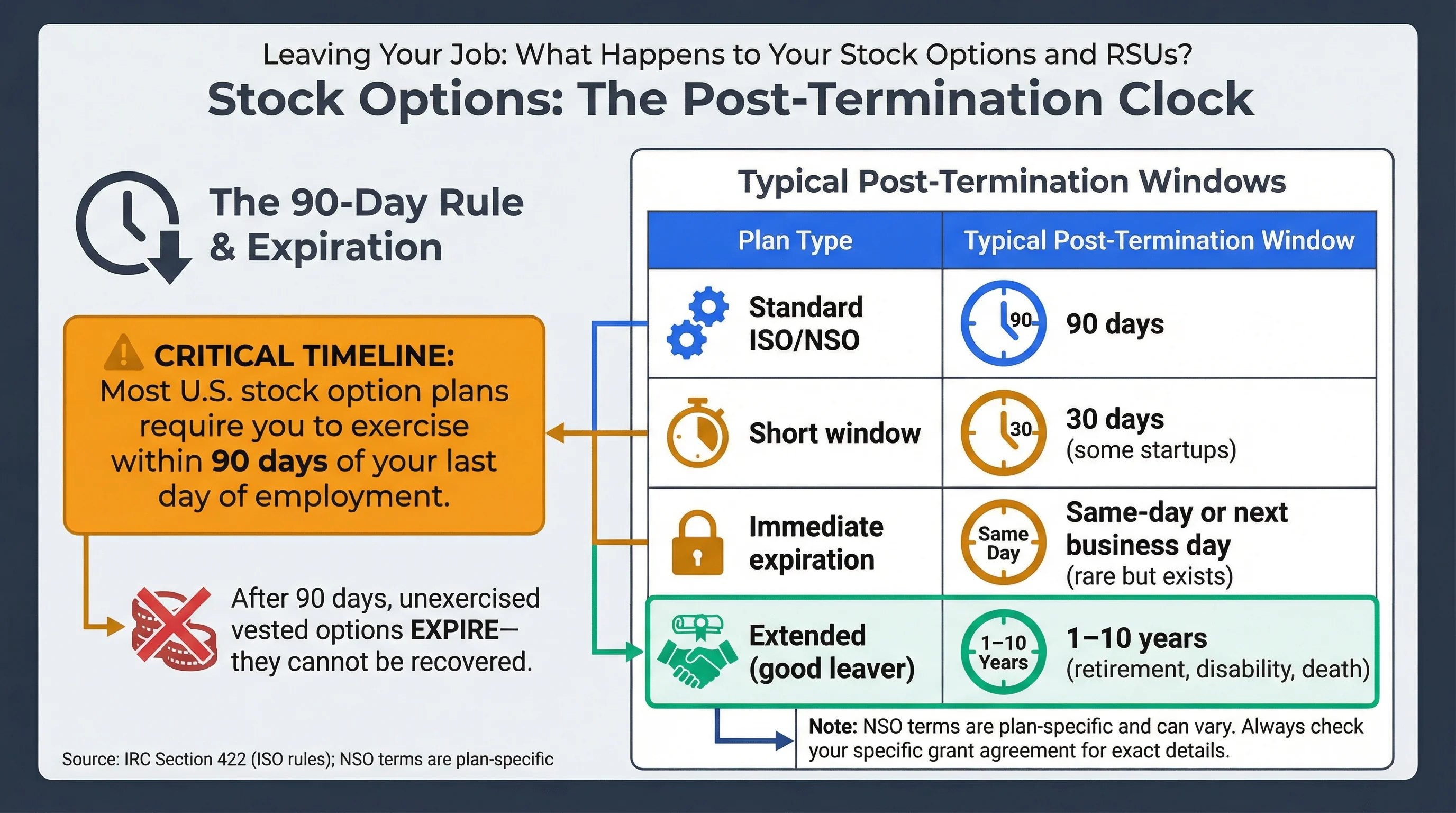

The 90-Day Rule (and Exceptions)

Most U.S. stock option plans require you to exercise within 90 days of your last day of employment. After that, unexercised vested options expire—they cannot be recovered.4

| Plan Type | Typical Post-Termination Window |

|---|---|

| Standard ISO/NSO | 90 days |

| Short window | 30 days (some startups) |

| Immediate expiration | Same-day or next business day (rare but exists) |

| Extended (good leaver) | 1–10 years (retirement, disability, death) |

Source: IRC Section 422 — ISO rules; NSO terms are plan-specific

Figure 1: The 90-day post-termination exercise window — your options expire if not exercised in time.

Why 90 Days?

For ISOs, IRC Section 422 requires that options be exercised within 3 months of termination to retain ISO treatment. Many plans use this as the default for both ISOs and NSOs. The 90-day window gives you time to:

- Decide whether to exercise

- Arrange financing (exercise can require significant cash)

- Consult a tax advisor

Good Leaver vs Bad Leaver

Some plans distinguish between good leavers and bad leavers:

| Leaver Type | Typical Definition | Possible Benefits |

|---|---|---|

| Good leaver | Retirement (e.g., 55+), disability, death, layoff, mutual agreement | Extended exercise (e.g., 1–10 years); sometimes accelerated vesting |

| Bad leaver | Resignation, termination for cause | Standard 90-day window; no acceleration |

Related Guides: For M&A scenarios (company acquisition), see our Stock Options in M&A guide.

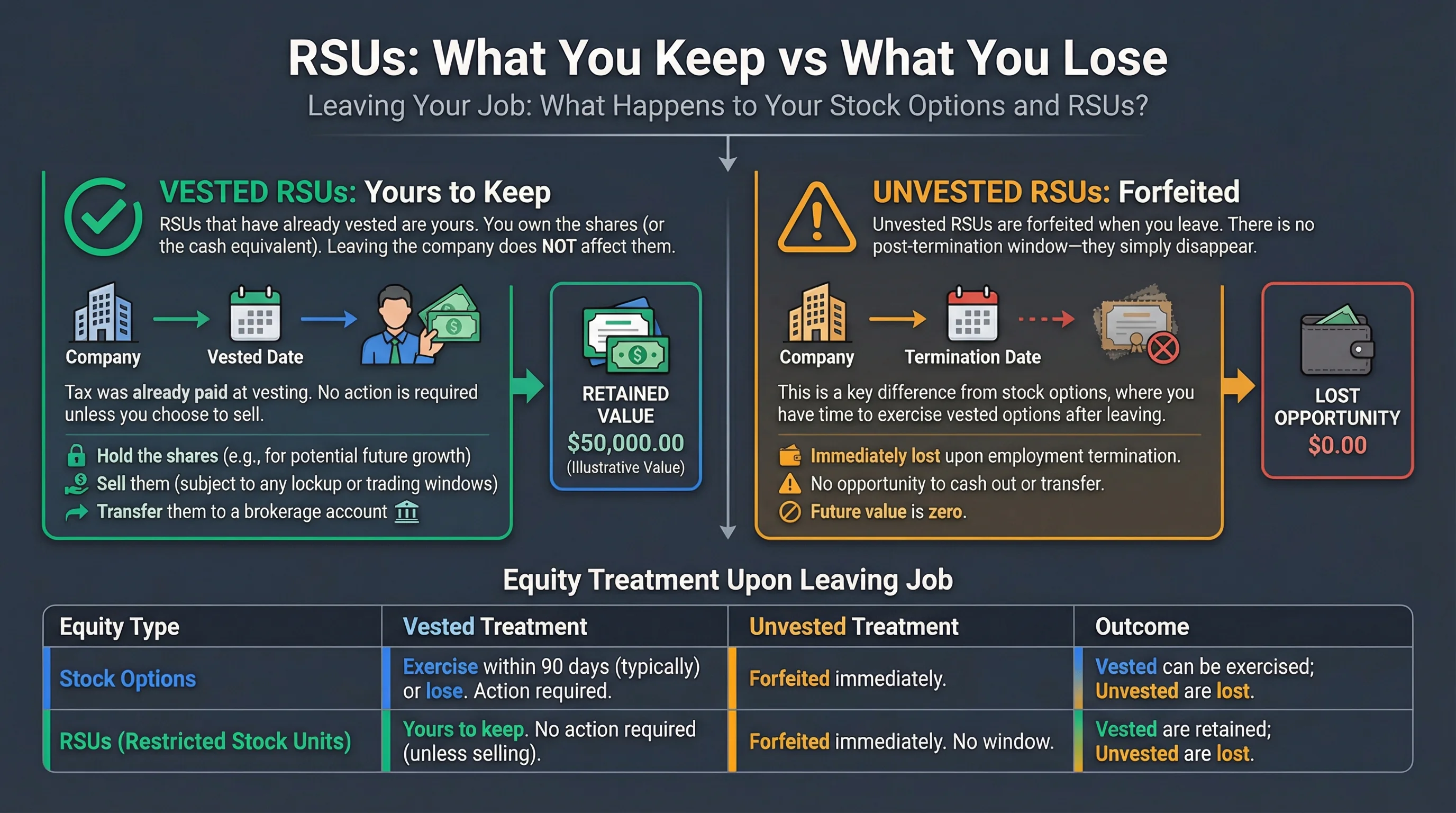

RSUs: What You Keep vs What You Lose

Vested RSUs: Yours to Keep

RSUs that have already vested are yours. You own the shares (or the cash equivalent, depending on plan). Leaving the company does not affect them. You can:

- Hold the shares

- Sell them (subject to any lockup or trading windows)

- Transfer them to a brokerage

No action is required unless you choose to sell. Tax was already paid at vesting.

Unvested RSUs: Forfeited

Unvested RSUs are forfeited when you leave. There is no post-termination window—they simply disappear. This is a key difference from stock options, where you have time to exercise vested options after leaving.

| Equity Type | Vested | Unvested |

|---|---|---|

| Stock Options | Exercise within 90 days (typically) or lose | Forfeited immediately |

| RSUs | Keep shares; no deadline | Forfeited immediately |

Source: Treasury Regulation §1.83-1

Accelerated Vesting: When Unvested RSUs May Vest

In some situations, unvested RSUs may vest early:

| Trigger | Typical Outcome |

|---|---|

| Change of control (M&A) | Single-trigger: vest on deal close; Double-trigger: vest only if you're terminated after deal |

| Death | Some plans accelerate all unvested RSUs to estate |

| Disability | May accelerate per plan |

| Retirement | Some plans offer pro-rata or full acceleration for retirees |

Check your plan's change of control and good leaver provisions.

Figure 2: What you keep vs what you lose — options vs RSUs when leaving.

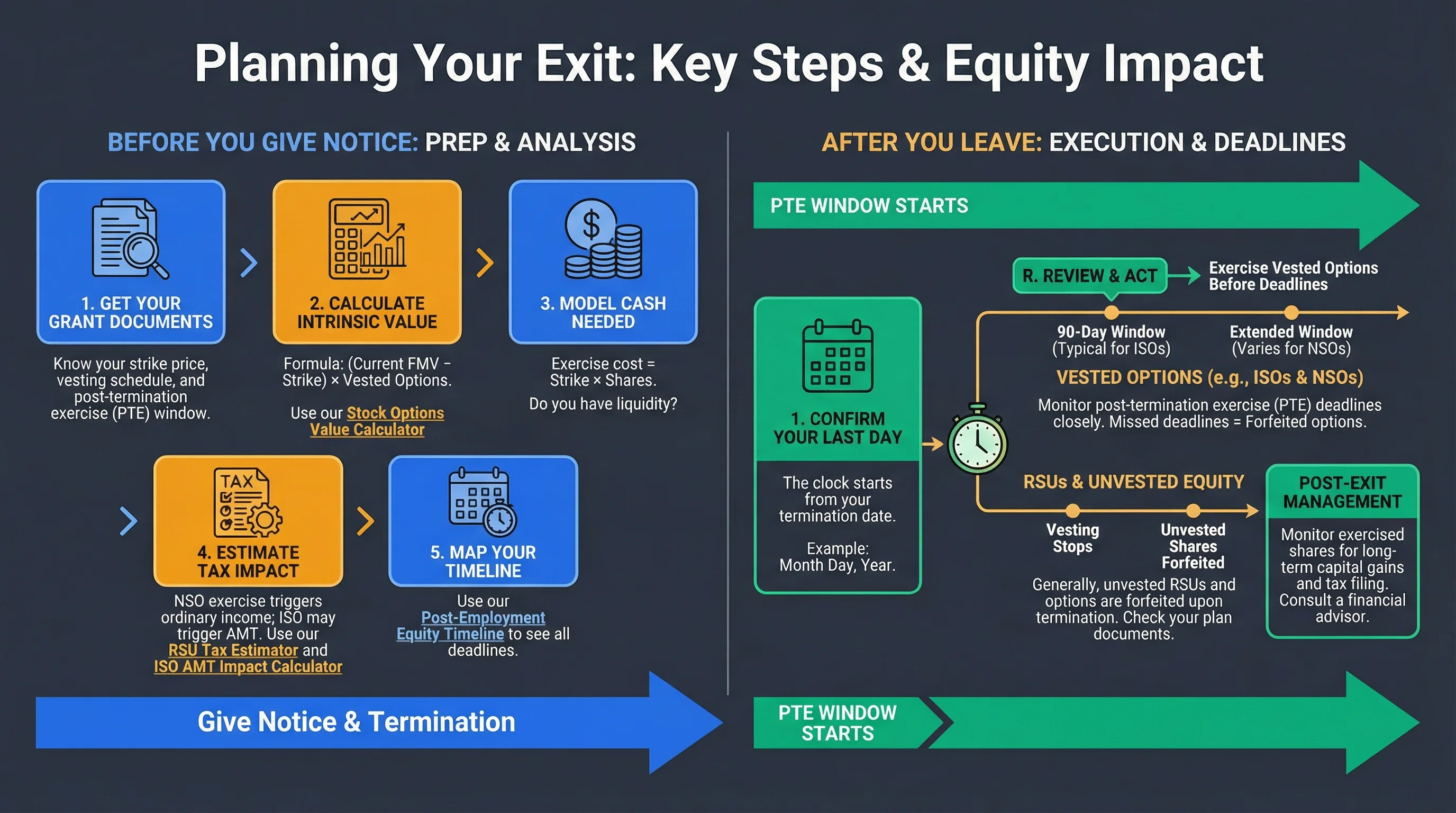

Planning Your Exit: Key Steps

Before You Give Notice

- Get your grant documents—Know your strike price, vesting schedule, and post-termination exercise window

- Calculate intrinsic value—(Current FMV − Strike) × Vested options. Use our Stock Options Value Calculator

- Model cash needed—Exercise cost = Strike × Shares. Do you have liquidity?

- Estimate tax impact—NSO exercise triggers ordinary income; ISO may trigger AMT. Use our RSU Tax Estimator and ISO AMT Impact Calculator

- Map your timeline—Use our Post-Employment Equity Timeline to see all deadlines

After You Leave

- Confirm your last day—The clock starts from your termination date

- Request exercise instructions—Contact your equity administrator (Carta, E*TRADE, etc.)

- Decide: exercise or let expire—Consider: cash available, tax impact, company outlook, liquidity

- Execute before deadline—Allow time for processing (brokerage transfers can take days)

Tax Implications of Post-Termination Exercise

NSO Exercise After Leaving

When you exercise NSOs as a former employee:

- Ordinary income on the spread (FMV − strike) at exercise

- Typically reported on Form 1099-NEC or 1099-MISC (not W-2)

- No withholding—you may need to make estimated tax payments

- State tax may apply based on your residence and the company's location

ISO Exercise After Leaving

If you exercise ISOs within the 90-day window:

- No ordinary income at exercise (if you hold the shares)

- AMT may apply—the spread is an AMT preference item

- Qualifying disposition requires holding 2 years from grant + 1 year from exercise

- Use our Holding Period Tracker to monitor dates

Figure 3: Post-employment timeline — plan your exit with deadlines in mind.

Frequently Asked Questions

Can I negotiate an extended exercise window when leaving?

Answer: Sometimes. Employers may agree to extend the window as part of a separation agreement, especially for good leavers or key employees. This is negotiable—ask before you sign anything.

What if I can't afford to exercise my options?

Answer: Options require cash to exercise (strike price × shares). If you can't afford it, you may need to: (1) exercise only a portion, (2) use a cashless exercise if your plan allows (sell enough shares to cover the cost), (3) consider pre-IPO exercise financing from specialized lenders, or (4) let them expire. Some companies offer financing; check with your equity administrator.

Do I lose my RSUs if I leave the day before a vesting date?

Answer: Yes. RSUs vest based on your employment status on the vesting date. If you're no longer employed, you typically forfeit that tranche. Plan your departure date carefully if a vesting date is imminent.

What happens to my options if my company is acquired while I'm employed?

Answer: Depends on the deal. Options may be assumed, substituted for acquirer stock, or cashed out. See our Stock Options in M&A guide.

Can I exercise options after 90 days if my plan says 90 days?

Answer: No. The plan document controls. Missing the deadline means your options expire. There is no IRS extension for personal circumstances.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRC Section 422 | Reference | https://www.law.cornell.edu/uscode/text/26/422 |

| IRS Publication 525 | Reference | https://www.irs.gov/publications/p525 |

| Treasury Regulation §1.83-1 | Reference | https://www.law.cornell.edu/cfr/text/26/1.83-1 |

| Carta Post-Termination Equity | Educational | https://carta.com/blog/post-termination-equity |

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Tax laws vary by jurisdiction and change frequently. Always consult a qualified tax professional (CPA, tax attorney, enrolled agent) before making decisions based on this information. The authors accept no liability for actions taken based on this content.