Executive Summary

What are stock options and how do they work for employees?

Stock options give you the right to purchase company stock at a predetermined price (the strike price) after a vesting period. You typically vest over 4 years with a 1-year cliff—meaning 25% vests after year one, then monthly or quarterly thereafter. You don't own shares until you exercise (pay the strike price). Incentive Stock Options (ISOs) can offer capital gains treatment; Nonqualified Stock Options (NSOs) are taxed as ordinary income when exercised.

Receiving your first stock option grant can feel exciting—and confusing. Over 60% of tech employees receive some form of equity compensation, yet many don't understand the basics until they face a critical deadline.1 Whether you work at a startup or a public company, knowing the fundamentals helps you avoid costly mistakes and make informed decisions.

The bottom line: Stock options are a right to buy—not ownership. Vesting controls when you can exercise; tax type (ISO vs NSO) controls how you're taxed. Missing an exercise deadline can mean losing everything.2

Critical Warning: If you leave your job, you typically have 90 days (or less) to exercise vested options before they expire. Failing to exercise in time means your options become worthless. Plan ahead if you're considering a job change.3

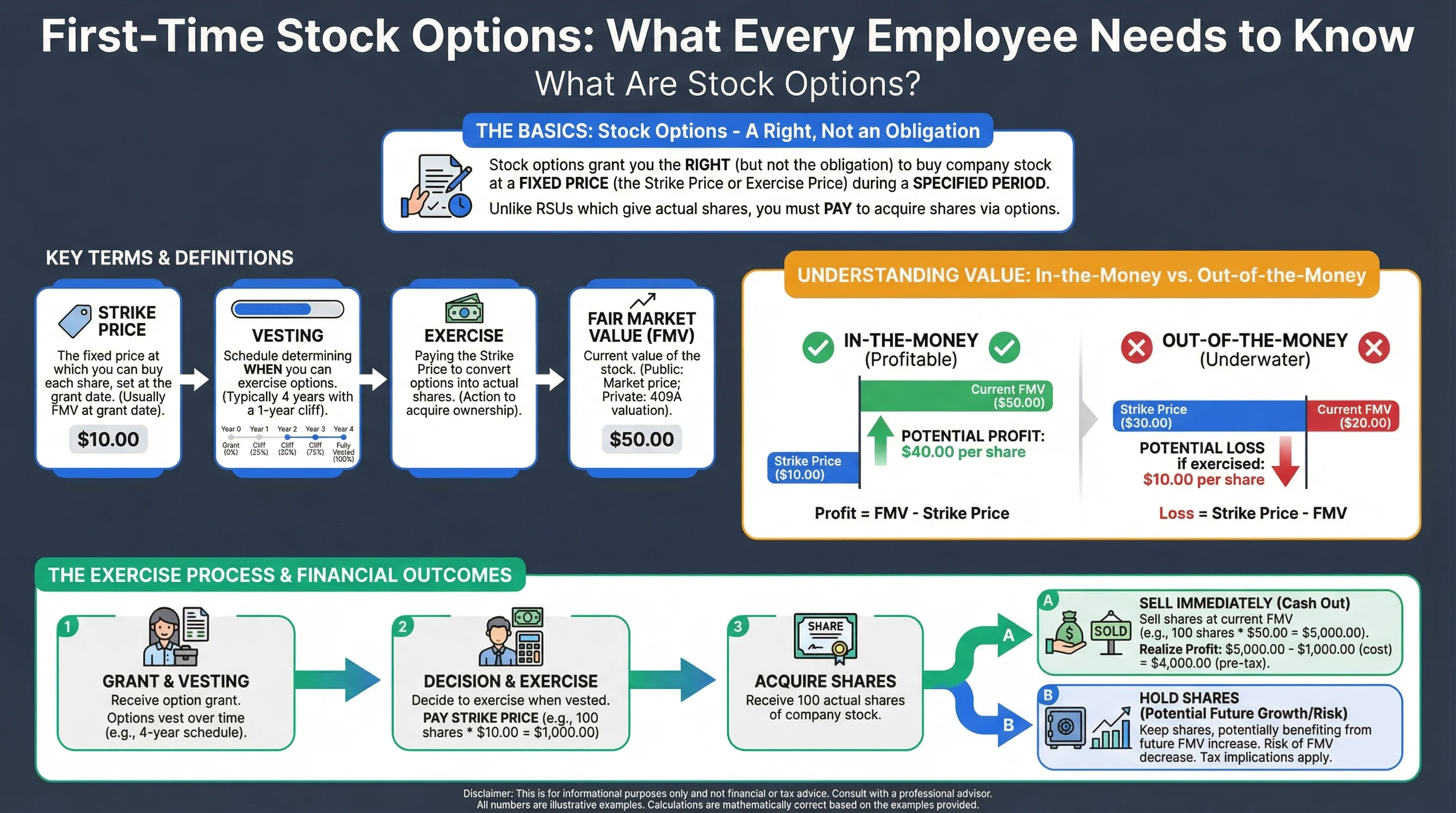

What Are Stock Options?

The Basics

Stock options are a form of equity compensation that gives you the right—but not the obligation—to buy company stock at a fixed price (the strike price or exercise price) during a specified period. Unlike RSUs, which grant actual shares at vesting, options require you to pay to acquire shares.

| Term | Definition |

|---|---|

| Strike Price | The price at which you can buy each share (set at grant, usually the FMV at that date) |

| Vesting | The schedule that determines when you can exercise (typically 4 years, 1-year cliff) |

| Exercise | Paying the strike price to convert options into actual shares |

| Fair Market Value (FMV) | The current value of the stock (public companies: market price; private: 409A valuation) |

| Intrinsic Value | (Current FMV − Strike Price) × Shares—the "in-the-money" value if you exercised today. See our how to calculate intrinsic value guide. |

Source: IRS Publication 525

Why Companies Grant Options

Companies use stock options to align employee incentives with company success. When the stock price rises, your options become more valuable. This creates motivation to help the company grow—and to stay long enough to vest.

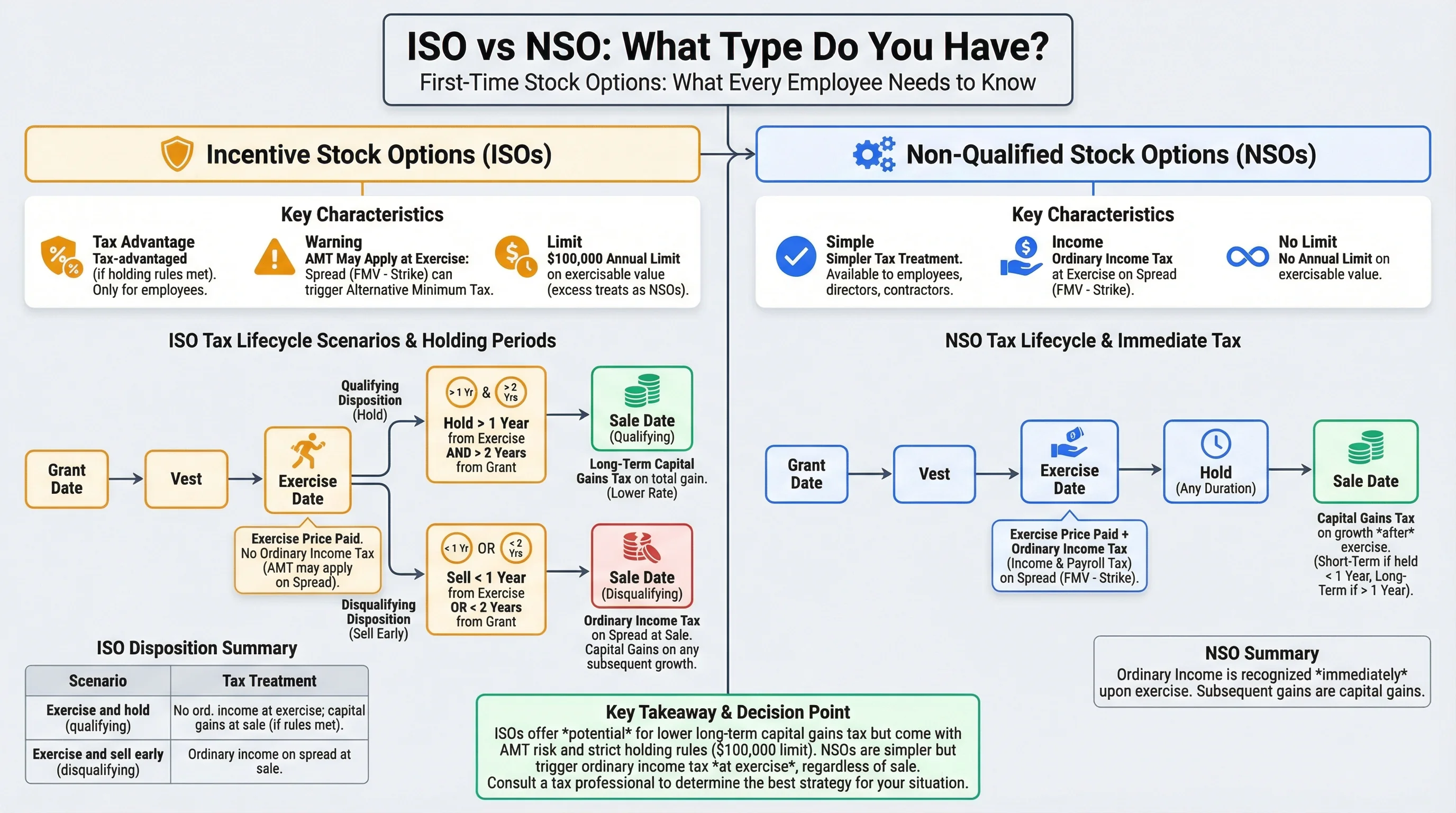

ISO vs NSO: What Type Do You Have?

Incentive Stock Options (ISOs)

ISOs are a tax-advantaged type of option available only to employees. Key characteristics:4

- No ordinary income tax at exercise (if you hold the shares)

- Potential long-term capital gains if you meet holding period rules: 2 years from grant + 1 year from exercise

- AMT may apply at exercise—the spread (FMV − strike) can trigger Alternative Minimum Tax

- $100,000 annual limit on exercisable value (excess treated as NSOs)

| Scenario | Tax Treatment |

|---|---|

| Exercise and hold (qualifying disposition) | No ordinary income at exercise; capital gains at sale |

| Exercise and sell within 1 year | Disqualifying disposition—ordinary income on spread |

| Exercise and sell within 2 years of grant | Disqualifying disposition—ordinary income on spread |

Source: IRC Section 422

Nonqualified Stock Options (NSOs)

NSOs (also called nonstatutory stock options) are more common and simpler from a tax perspective:

- Ordinary income at exercise on the spread (FMV − strike price)

- Withholding typically required (22% federal supplemental rate)

- No special holding period for favorable treatment—but holding >1 year after exercise gives long-term capital gains on future appreciation

- No $100K limit—companies can grant unlimited NSOs

Related Guides: For detailed ISO vs NSO comparison, see our ISO vs NSO guide. For AMT planning with ISOs, see our AMT planning guide.

Figure 1: ISO vs NSO — key tax differences and holding period requirements for favorable treatment.

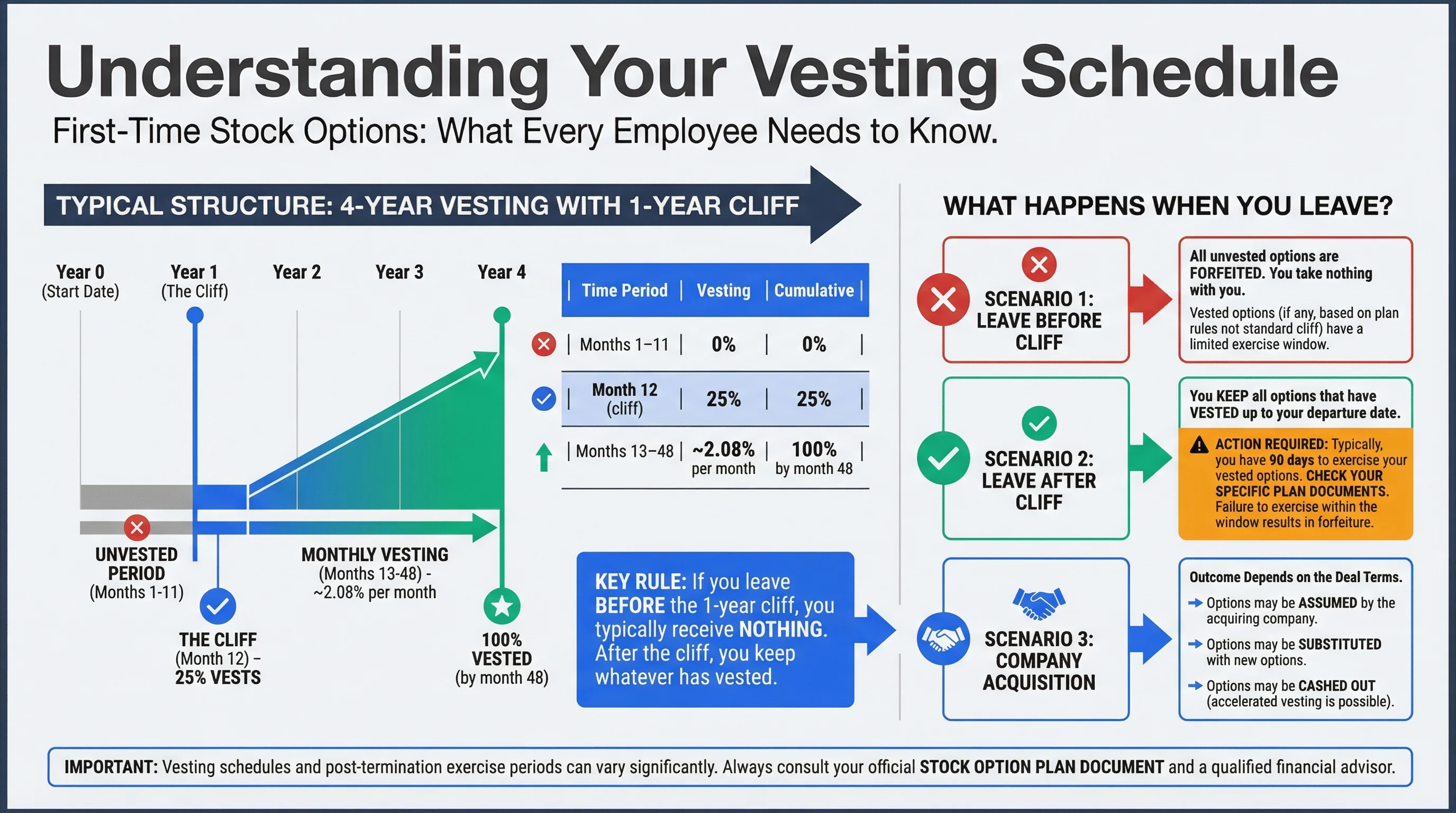

Understanding Your Vesting Schedule

Typical Structure: 4-Year Cliff

The most common vesting structure is 4 years with a 1-year cliff:

| Time Period | Vesting | Cumulative |

|---|---|---|

| Months 1–11 | 0% | 0% |

| Month 12 (cliff) | 25% | 25% |

| Months 13–48 | ~2.08% per month | 100% by month 48 |

If you leave before the 1-year cliff, you typically receive nothing. After the cliff, you keep whatever has vested.

What Happens When You Leave?

| Situation | Outcome |

|---|---|

| Leave before cliff | All unvested options forfeited; vested options have limited exercise window |

| Leave after cliff | Keep vested options; typically 90 days to exercise (check your plan) |

| Company acquisition | Depends on deal—options may be assumed, substituted, or cashed out |

Source: Stock Options in M&A guide

Figure 2: Typical 4-year vesting schedule — 1-year cliff, then monthly vesting.

Key Questions First-Time Recipients Ask

"What Are My Options Worth?"

Intrinsic value (if in-the-money) = (Current FMV − Strike Price) × Vested Shares

Example: 1,000 vested options, strike $10, current FMV $50:

Intrinsic Value = ($50 − $10) × 1,000 = $40,000

But real value depends on liquidity. If the company is private, you may not be able to sell. Use our Stock Options Value Calculator to model scenarios.

"Should I Exercise Now or Wait?"

For NSOs: Exercising creates an immediate tax bill (ordinary income on the spread). Only exercise if you have a reason—e.g., approaching a liquidity event, or you want to start the capital gains holding period.

For ISOs: Early exercise can reduce AMT exposure if the spread is small. But you need cash to pay the strike price, and you risk losing it if the company fails. See our Early Exercise Break-Even Calculator for analysis.

"I'm Leaving—What Are My Deadlines?"

Critical: Check your plan documents. Common rules:

- 90 days post-termination to exercise (most common)

- 10 years from grant date maximum (options expire if not exercised)

- Some plans offer extended exercise for good leavers (e.g., retirement, disability)

Use our Post-Employment Equity Timeline to map your deadlines.

Tax Basics: What to Expect

NSO Exercise

When you exercise NSOs:

- Ordinary income = (FMV at exercise − Strike) × Shares

- Reported on W-2 (or 1099 for former employees)

- Employer typically withholds 22% federal (may be insufficient for high earners)

- State tax applies in most states

ISO Exercise (Qualifying Disposition)

If you hold ISO shares and meet the holding period:

- No ordinary income at exercise

- Capital gains at sale (0%, 15%, or 20% federal + 3.8% NIIT if applicable)

- AMT may apply at exercise—calculate with our ISO AMT Impact Calculator

ISO Exercise (Disqualifying Disposition)

If you sell before meeting the holding period:

- Ordinary income on the spread (same as NSO)

- No capital gains preference

Figure 3: Tax flow for NSO vs ISO — when and how each is taxed.

Action Checklist for New Option Recipients

Frequently Asked Questions

What is the difference between stock options and RSUs?

Answer: Stock options give you the right to buy shares at a fixed price; you must pay to exercise. RSUs grant actual shares at vesting—no payment required. RSUs are taxed as ordinary income at vesting; options are taxed at exercise (NSO) or at sale (ISO, if qualifying).

Source: RSU vs Stock Options Tax Comparison

Can I lose my stock options?

Answer: Yes. Unvested options are forfeited if you leave before they vest. Vested options expire if you don't exercise within the post-termination window (often 90 days). If the company fails, options can become worthless.

What happens if my company goes public?

Answer: Your options may become more liquid—you can often sell on the open market after exercise. Lockup periods (typically 180 days post-IPO) may restrict when insiders can sell. See our IPO Lockup Periods guide.

Do I owe tax when I receive the grant?

Answer: No. Granting options is not a taxable event. Tax occurs at exercise (NSO) or at sale (ISO, if qualifying disposition).

How do I know my options' fair market value if the company is private?

Answer: Private companies obtain a 409A valuation (typically annually or after material events) to set FMV. Your company or equity administrator (e.g., Carta) can provide this. See our Section 409A Valuation guide.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRS Publication 525 | Reference | https://www.irs.gov/publications/p525 |

| IRS Publication 550 | Reference | https://www.irs.gov/publications/p550 |

| IRC Section 422 | Reference | https://www.law.cornell.edu/uscode/text/26/422 |

| Carta Equity 101 | Educational | https://carta.com/blog/equity-101 |

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Tax laws vary by jurisdiction and change frequently. Always consult a qualified tax professional (CPA, tax attorney, enrolled agent) before making decisions based on this information. The authors accept no liability for actions taken based on this content.