Executive Summary

What happens to my stock options when my company is acquired?

In M&A transactions, your stock options are typically assumed by the acquirer, substituted with new options (per IRC Section 424), or cashed out. ISOs can preserve qualified status if the Ratio Test and Spread Test are met. Cash-outs trigger ordinary income for NSOs and cause ISOs to lose qualified status. The tax treatment depends on the deal structure—Type B reorganizations (100% stock) offer the best tax deferral.

When your company undergoes a merger or acquisition, your stock options face one of three fates: assumption, substitution, or cash-out. The tax consequences vary dramatically depending on whether you hold Incentive Stock Options (ISOs) or Nonqualified Stock Options (NSOs), and how the transaction is structured under IRC Section 368 reorganizations.

The bottom line: IRC Section 424 provides a critical exception allowing ISOs to preserve qualified status during M&A if specific tests are met. Cash-outs trigger immediate ordinary income taxation and cause ISOs to lose their favorable treatment. Understanding these rules can save tens of thousands in taxes.1

Critical Warning: If your ISO options are cashed out in an M&A transaction, they lose qualified status and are treated as NSOs, triggering ordinary income tax (up to 37%) plus FICA taxes (7.65%) on the spread. This can result in $45,000+ in taxes on a $100,000 cash-out that could have been deferred as capital gains.2

Introduction to Stock Options in M&A

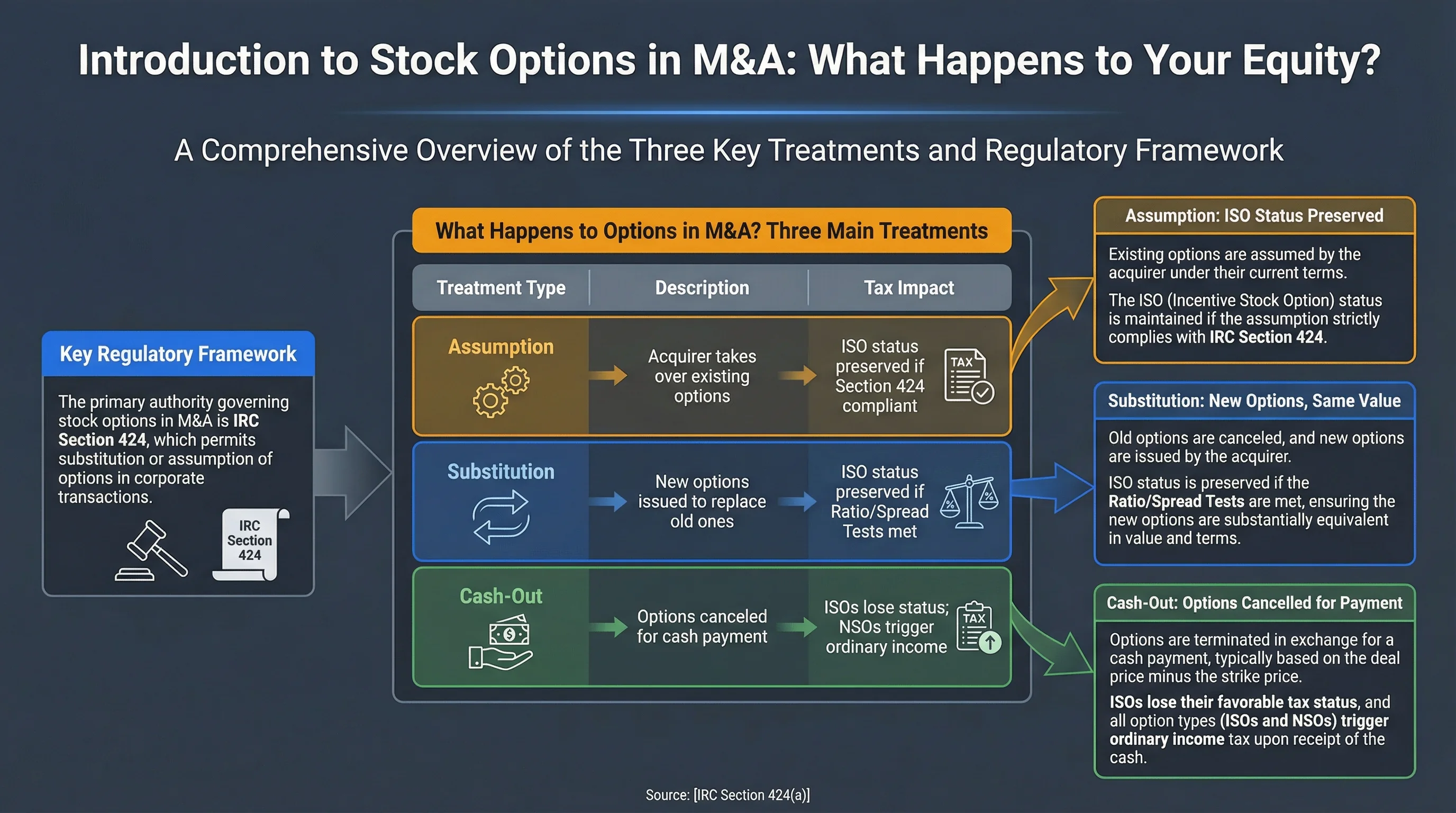

What Happens to Options in M&A?

When a company is acquired, stock options are typically handled in one of three ways:

| Treatment Type | Description | Tax Impact |

|---|---|---|

| Assumption | Acquirer takes over existing options | ISO status preserved if Section 424 compliant |

| Substitution | New options issued to replace old ones | ISO status preserved if Ratio/Spread Tests met |

| Cash-Out | Options canceled for cash payment | ISOs lose status; NSOs trigger ordinary income |

Source: IRC Section 424(a)

Key Regulatory Framework

The primary authority governing stock options in M&A is IRC Section 424, which permits substitution or assumption of options in corporate transactions without triggering "modification" that would disqualify ISOs. The regulations define a "corporate transaction" broadly to include:3

- Mergers and consolidations

- Stock acquisitions

- Spinoffs, split-ups, and split-offs

- Reorganizations (Type A, B, C under Section 368)

- Partial or complete liquidations

- Stock splits and stock dividends (proportional adjustments)

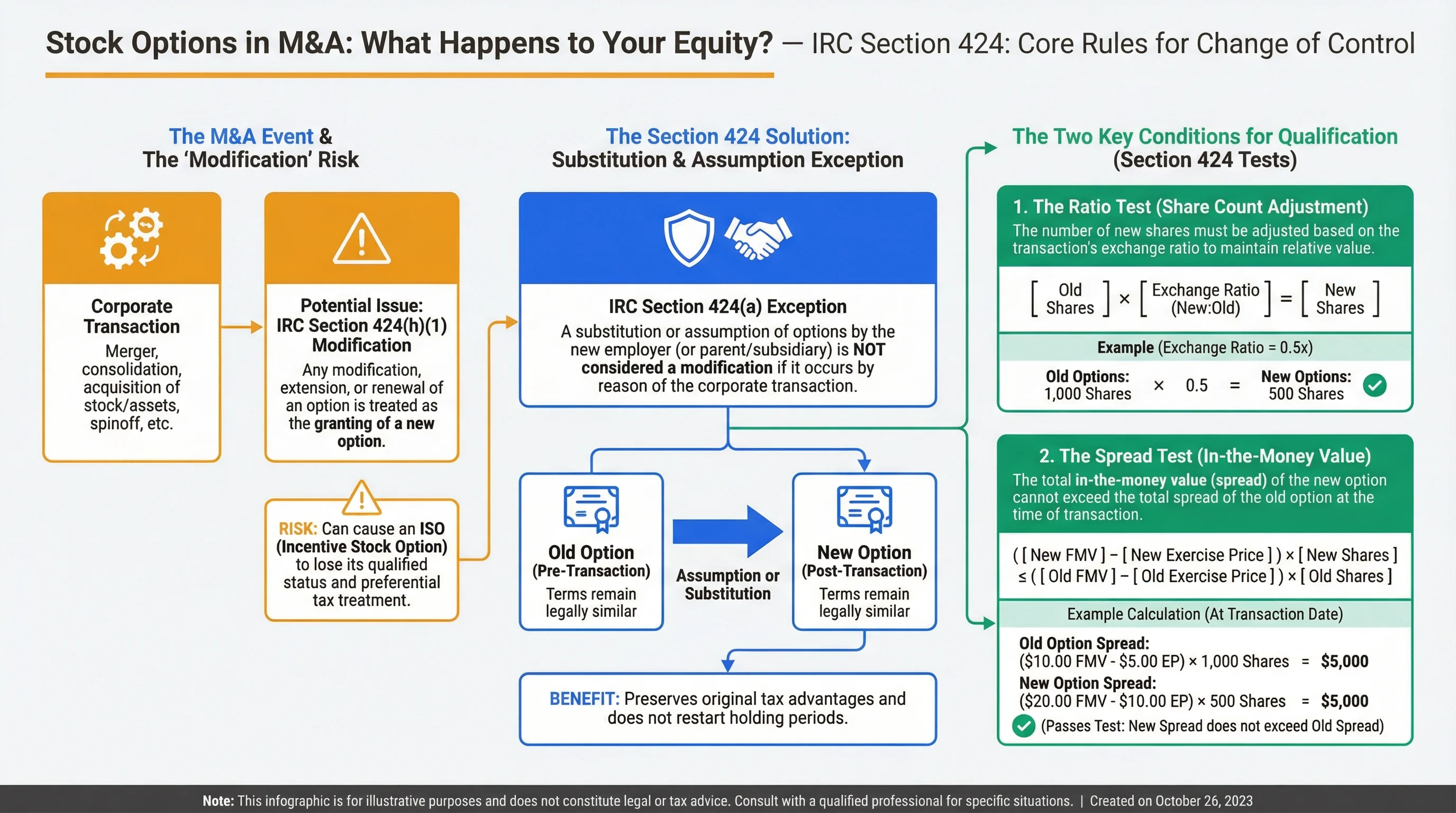

IRC Section 424: Core Rules for Change of Control

Substitution and Assumption Defined

Under IRC Section 424(a), a substitution of a new option for an old option, or an assumption of an old option by an employer corporation (or parent/subsidiary), can occur "by reason of a corporate merger, consolidation, acquisition of property or stock, spinoff, split-up or split-off, reorganization or partial or complete liquidation" without being considered a modification.4

This exception is critical because, under IRC Section 424(h)(1), any modification, extension, or renewal of an option is treated as the granting of a new option, which could cause an ISO to lose its qualified status.5

The Ratio Test and Spread Test

For a substitution or assumption to qualify under Section 424, two conditions must be satisfied:6

1. The Ratio Test:

New Option Price / New FMV ≤ Old Option Price / Old FMV

2. The Spread Test: The spread (difference between option price and FMV) cannot be more favorable to the optionee after substitution than before.

Example Calculation:

| Metric | Pre-M&A | Post-M&A | Test Result |

|---|---|---|---|

| Option Price | $50/share | $75/share | — |

| FMV | $100/share | $150/share | — |

| Price/FMV Ratio | 50% | 50% | ✅ Pass |

| Spread per Share | $50 | $75 | ✅ Pass (proportional) |

In this example, both tests pass because the ratio remains constant (50% discount) and the spread increases proportionally with the stock value.

Source: Treasury Regulation §1.424-1

Figure 1: IRC Section 424 overview — how stock options are treated in M&A transactions and the tests required to preserve ISO qualified status.

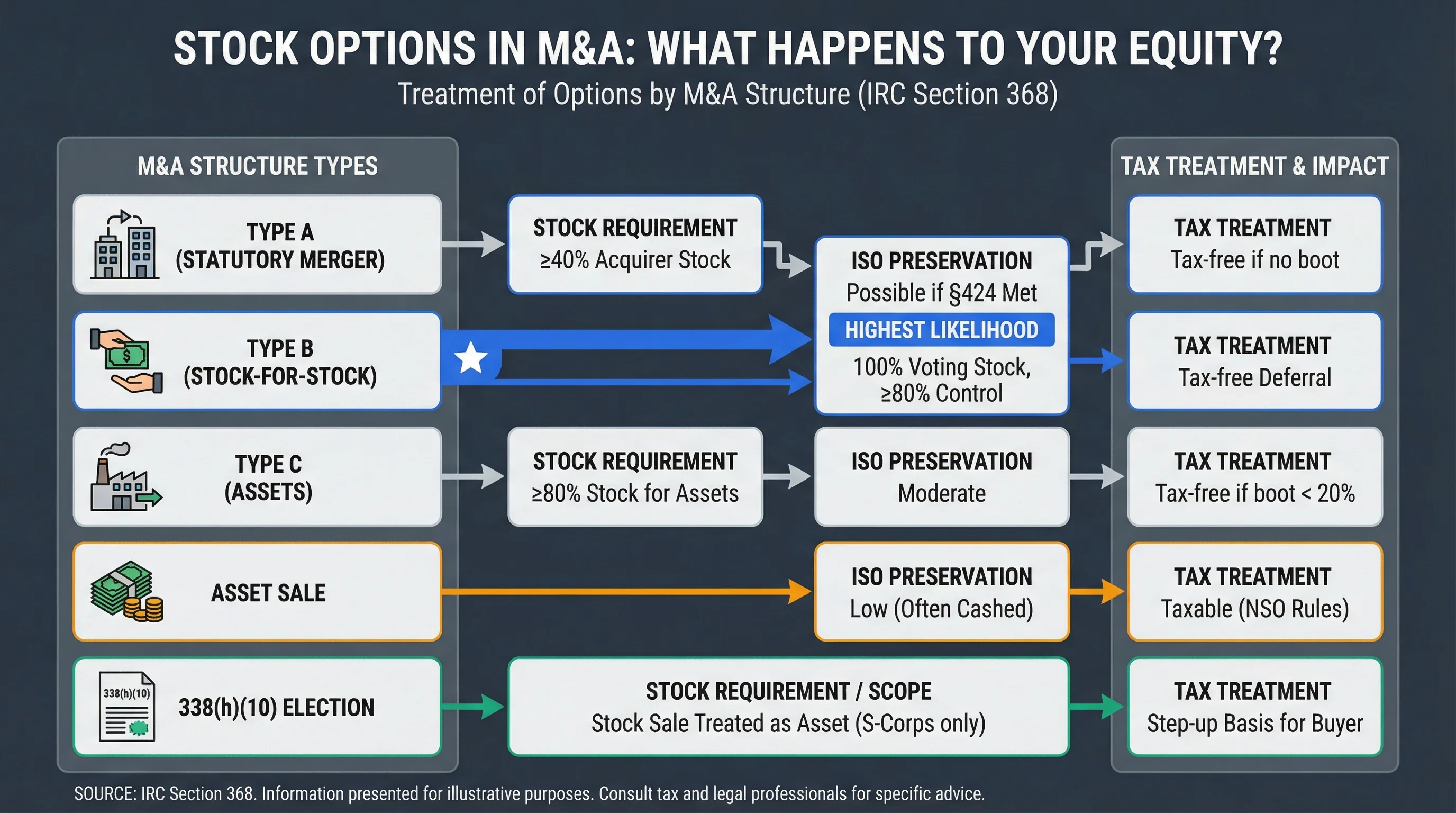

Treatment of Options by M&A Structure

Tax Treatment by Reorganization Type (IRC Section 368)

The tax treatment of options in M&A depends heavily on the transaction structure:

| Structure | Stock Requirement | ISO Preservation | Tax Treatment |

|---|---|---|---|

| Type A (Statutory Merger) | ≥40% acquirer stock | Possible if §424 met | Tax-free if no boot |

| Type B (Stock-for-Stock) | 100% voting stock, ≥80% control | Highest likelihood | Tax-free deferral |

| Type C (Assets) | ≥80% stock for assets | Moderate | Tax-free if boot < 20% |

| Asset Sale | N/A | Low (often cashed) | Taxable (NSO rules) |

| 338(h)(10) Election | Stock sale treated as asset | S-Corps only | Step-up basis for buyer |

Source: IRC Section 368

Figure 2: M&A transaction types and option treatment — comparison of reorganization structures and their impact on ISO preservation and tax treatment.

Cash-Out Treatment

When options are cashed out (canceled in exchange for cash), the tax consequences are immediate:

For NSOs:

- Ordinary income on the spread (up to 37% federal)

- FICA taxes (1.45% + 0.9% Medicare surtax)

- FUTA taxes

- Immediate withholding required

For ISOs:

- Lose qualified status (treated as NSOs)

- Same tax treatment as NSOs above

- No AMT benefit

- No capital gains deferral

Example: $100,000 ISO cash-out (spread value)

- As ISO (if preserved): Deferred to capital gains (~15-23% when sold)

- As NSO (cash-out): $37,000 ordinary tax + $7,650 FICA = $44,650 total

The difference: $20,000+ in additional taxes from cash-out vs. preserving ISO status.

Tax Consequences for ISOs vs. NSOs

ISOs in M&A

ISOs receive favorable tax treatment under IRC Section 422. For a complete comparison of ISO vs NSO tax treatment, see our ISO vs NSO guide:

| Event | Regular Tax | AMT | Employment Tax |

|---|---|---|---|

| Grant | None | None | None |

| Exercise | None (if holding periods met) | AMT on spread | None |

| Qualified Disposition | Long-term capital gains | No AMT adjustment | None |

| Disqualifying Disposition | Ordinary income on spread | May reverse AMT | None |

Key Considerations:

- No tax at exercise if holding periods met (2 years from grant, 1 year from exercise)

- AMT applies to spread at exercise (28% rate)

- Post-M&A sale: Form 1099-B, Schedule D for long-term capital gains (0-20% + 3.8% NIIT)

- Net exercise or cash-out = NSO treatment, full payroll taxes

Source: IRS Publication 525

NSOs in M&A

NSOs are taxed as ordinary income at exercise:

| Event | Tax Treatment |

|---|---|

| Exercise | Ordinary income on spread (up to 37%) + FICA (1.45% + 0.9%) + FUTA |

| Cash-Out | Compensation income, immediate withholding |

| Sale | Capital gains only on appreciation after exercise |

Strategies:

- Cashless exercise post-M&A to minimize upfront tax

- Coordinate with high-income years to optimize tax brackets

- Consider timing of exercises relative to deal closing

Figure 3: ISO vs NSO tax treatment in M&A — comparison of tax consequences at exercise, sale, and cash-out scenarios.

Accelerated Vesting: Single-Trigger vs. Double-Trigger

For a simpler explanation of how double-trigger works and why it matters, see our double-trigger acceleration guide.

Single-Trigger Vesting

Options vest automatically upon a change of control, regardless of continued employment.

Tax Impact: If acceleration occurs as part of a Section 424-compliant assumption or substitution, it does not trigger modification treatment.

Double-Trigger Vesting

Options vest only if both conditions are met:

- Change of control occurs

- Employment is terminated (typically without cause or for good reason)

Tax Impact: Same as single-trigger—no modification if Section 424 compliant.

Key Point: Accelerated vesting itself doesn't trigger adverse tax consequences if the underlying transaction qualifies under Section 424. The tax treatment depends on whether you exercise, hold, or sell the shares after vesting. For more on restricted stock and vesting strategies, see our Section 83(b) election guide.

Reporting and Compliance

Required IRS Forms

| Form | Purpose | When Required |

|---|---|---|

| Form 3921 | ISO exercise reporting | Within 30 days of exercise |

| Form 3922 | ESPP exercise reporting | Within 30 days of exercise |

| Form 1099-B | Sales proceeds reporting | When shares are sold |

| Schedule D / Form 8949 | Capital gains reporting | Annual tax return |

| W-2 | NSO income reporting | Annual (employer reports) |

Source: IRS Form 3921 Instructions

Withholding Requirements

- NSO cash-outs: Mandatory withholding (22% federal + state)

- ISO exercises: No withholding required

- State taxes: Most states follow federal treatment (PA has exceptions)

Documentation Best Practices

- Document Section 424 compliance (Ratio Test, Spread Test calculations)

- Maintain valuation reports for FMV determinations

- Keep records of transaction structure and timing

- Preserve option agreements and amendment documents

Planning Strategies and Pitfalls

Strategies to Preserve ISO Status

-

Ensure Substitution Meets Tests

- Verify Ratio Test and Spread Test calculations

- Document compliance in transaction documents

- Work with tax advisor to confirm Section 424 qualification

-

Favor Stock-for-Stock Deals

- Type B reorganizations offer best ISO preservation

- Avoid cash consideration (boot) that could disqualify

- Negotiate for stock consideration when possible

-

Avoid Net Exercise

- Net exercise (using shares to pay exercise price) causes ISO to lose status

- Use cash to exercise if preserving ISO status is priority

Common Pitfalls

| Pitfall | Consequence | Solution |

|---|---|---|

| Boot exceeds limits | Disqualifies tax-free treatment | Negotiate stock consideration |

| Non-pro-rata payouts | May trigger modification | Ensure proportional treatment |

| Service-tied earnouts | Loses QSBS exclusion | Structure as stock consideration |

| Cash-out of ISOs | Loses qualified status | Negotiate substitution instead |

QSBS Considerations

Qualified Small Business Stock (QSBS) under IRC Section 1202 offers up to 100% exclusion on gains, but:

- ✅ Preserved in stock purchases and reverse triangular mergers

- ❌ Lost with cash consideration or service-tied earnouts

- ⚠️ Timing matters: Must meet 5-year holding period

Source: IRC Section 1202

Frequently Asked Questions

Does cash-out always trigger taxes?

Answer: Yes, for NSOs cash-out triggers ordinary income tax immediately. For ISOs, cash-out causes loss of qualified status and triggers the same ordinary income treatment. The only way to defer taxes is through assumption or substitution that preserves ISO status.

Source: IRC Section 424(h)(1)

Can I exercise my options before the M&A closes?

Answer: Yes, you can exercise pre-M&A to start the capital gains holding period clock. However, this creates liquidity risk if the deal falls through or if you can't sell immediately due to lockup periods. Consider your cash flow and risk tolerance.

What if the acquirer's stock tanks after the deal?

Answer: If you received acquirer stock in substitution and the value declines, you can realize capital losses when you sell. For options that were underwater (exercise price > FMV), they're typically canceled for no consideration in cash-outs.

How does AMT affect ISO exercises in M&A?

Answer: AMT applies to the bargain element (spread) when you exercise ISOs, regardless of M&A context. If you exercise ISOs before a cash-out, you'll pay AMT on paper gains. Consider a disqualifying disposition (exercise and sell same year) to avoid AMT, though this triggers ordinary income tax instead. For comprehensive AMT planning strategies, see our AMT planning guide.

Source: IRS Form 6251 Instructions

Are there special rules for S-Corporations?

Answer: Yes. S-Corporations can use a 338(h)(10) election to treat a stock sale as an asset sale, providing step-up basis for the buyer. This affects how options are treated—consult a tax advisor for S-Corp specific planning.

What happens to underwater options?

Answer: Underwater options (where exercise price exceeds FMV) are typically canceled for no consideration in cash-outs. In substitutions, they may be adjusted proportionally, but the economic value remains zero or negative.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRC Section 424 | Statute | https://www.law.cornell.edu/uscode/text/26/424 |

| Treasury Regulation §1.424-1 | Regulation | https://www.law.cornell.edu/cfr/text/26/1.424-1 |

| IRC Section 368 | Statute | https://www.law.cornell.edu/uscode/text/26/368 |

| IRS Publication 525 | Guidance | https://www.irs.gov/publications/p525 |

| IRS Form 3921 | Form | https://www.irs.gov/pub/irs-pdf/f3921.pdf |

| IRC Section 1202 (QSBS) | Statute | https://www.law.cornell.edu/uscode/text/26/1202 |

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Tax laws vary by jurisdiction and change frequently. Always consult a qualified tax professional (CPA, tax attorney, enrolled agent) before making decisions based on this information. The authors accept no liability for actions taken based on this content.

Footnotes

-

IRC Section 424 provides the framework for preserving ISO qualified status during corporate transactions. Treasury Regulation §1.424-1 provides detailed guidance on the Ratio Test and Spread Test requirements. ↩

-

Cash-out of ISOs triggers modification treatment under IRC Section 424(h)(1), causing loss of qualified status and immediate ordinary income taxation. ↩

-

Treasury Regulation §1.424-1 defines "corporate transaction" broadly to include various types of reorganizations and corporate changes. ↩

-

IRC Section 424(a) permits substitution or assumption "by reason of" qualifying corporate transactions without triggering modification. ↩

-

IRC Section 424(h)(1) provides that modifications, extensions, or renewals are treated as new option grants, which could disqualify ISOs. ↩

-

Treasury Regulation §1.424-1 requires both the Ratio Test and Spread Test to be satisfied for substitution to qualify under Section 424. ↩