Executive Summary

What is a 409A valuation—in plain English?

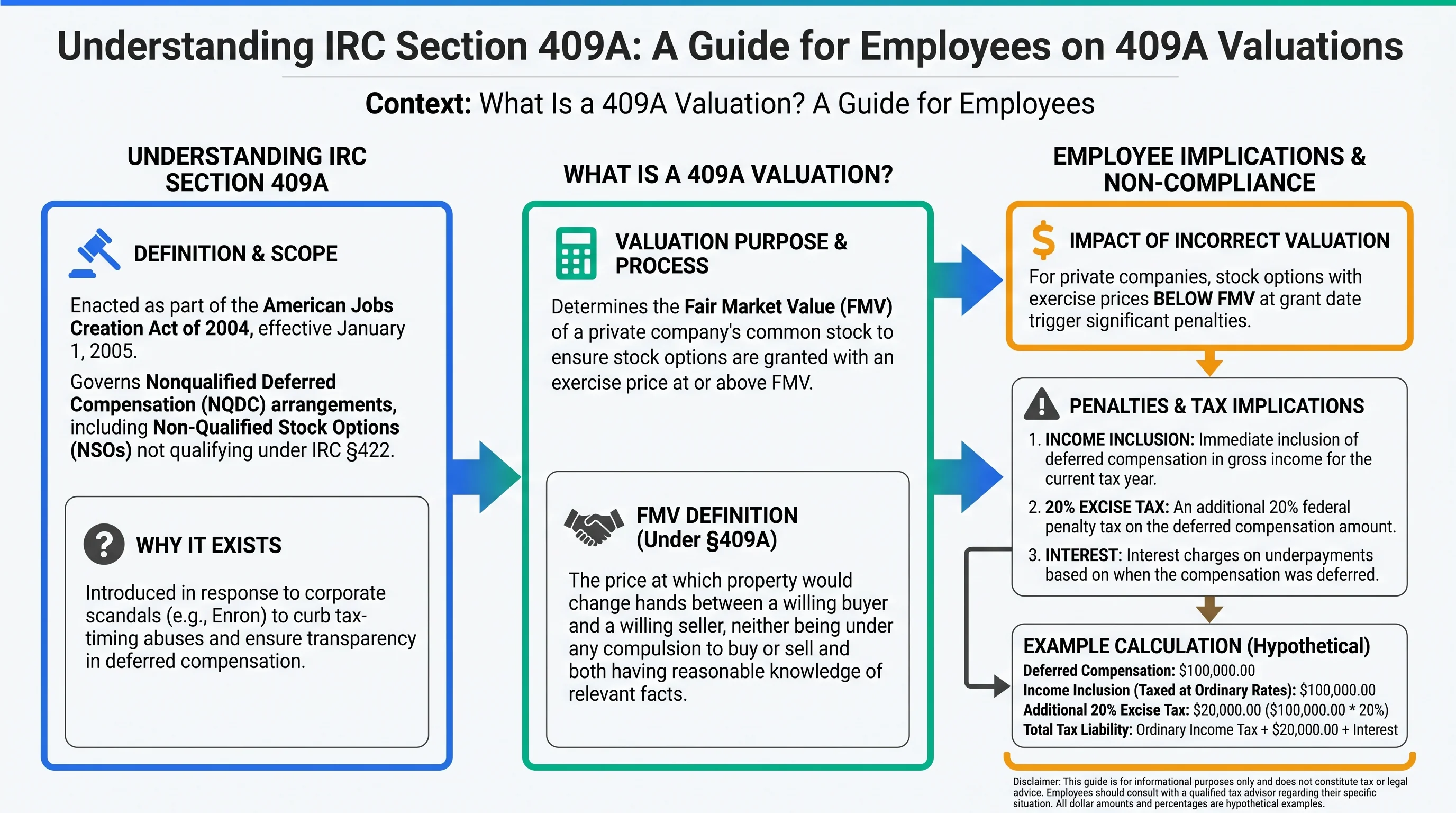

It is a formal process to estimate the fair market value (FMV) of a private company’s common stock on a specific date. Private companies use it so stock options and certain other equity awards can be priced at (or above) FMV, which helps avoid treating the award as discounted nonqualified deferred compensation under IRC Section 409A.

If you work at a private company and receive stock options, you have probably noticed that your strike price (exercise price) changes over time and often jumps after a funding round. That pattern is not random: it is usually downstream of a 409A valuation (sometimes called an “IRC 409A valuation” or “common stock FMV study”).

This guide is written for employees, not appraisers. It explains what the valuation is trying to accomplish, why it exists, what “safe harbors” mean in practice, and what questions are worth asking when your strike price, company stage, or equity package changes. For a shorter definition-first article, see What Is a 409A Valuation? (Simple Explanation). For more technical depth on FMV methods and regulatory citations, pair this with Section 409A Valuation: Fair Market Value and 409A valuation for employees—what it means for your options.

The bottom line: A 409A valuation is how many private companies support defensible common stock FMV so option grants are not “cheap stock” grants that trigger Section 409A tax penalties.1

Critical Warning: If you are considering early exercise, promissory notes, extension of exercise windows, or any nonstandard equity arrangement, do not guess. Those features can interact with Section 83 and Section 409A in ways that are not obvious from a brokerage screen. Get professional advice.2

Figure 1: Conceptual map—your grant agreement and employer administration still control the actual legal terms.

Why 409A Exists (and Why Employees Should Care)

The policy story (short)

Congress enacted IRC Section 409A in 2004 (generally effective in 2005) to limit tax-timing games with nonqualified deferred compensation. The rules are broad, and they interact with equity because certain stock rights can be treated as deferred compensation if the pricing and deferral features do not comply.3

Employees care because the penalty regime is employee-facing in many failure modes: taxation can be accelerated, and the statute includes a 20% additional tax on amounts includible under the violation rules, plus interest concepts that can make the problem worse over time.4

What the valuation is not

A 409A valuation is not a guarantee that your equity will be worth money later. It is also not the same thing as the preferred share price from a venture round. Preferred stock often carries liquidation preferences, dividend rights, and other economics that can make preferred price an unreliable shortcut for common stock FMV.

When Things Break: Why “Cheap Stock” Is a Big Deal

This section is not here to scare you—it is here to explain why HR, finance, and counsel act conservative about grant pricing.

When Section 409A applies to a nonqualified deferred compensation arrangement that fails the rules, the statute’s penalty framework can include immediate income inclusion for amounts that are deferred and not compliant, a 20% additional tax, and interest charges tied to late payment concepts under the statute’s formula.4 In plain terms: the IRS has made discounted deferred compensation expensive to get wrong.

A stylized example (not tax advice)

Suppose (hypothetically) an employee has $200,000 of vested deferred amounts that are discovered to be noncompliant in a given year, and that amount becomes includible under the Section 409A rules. The 20% additional tax alone is $40,000 on top of normal income taxes that may also apply to the inclusion. Interest concepts under the statute can stack on top depending on timing and facts. Real cases vary widely; the point is that the penalties are structural, not “maybe a small penalty.”

Why companies prefer safe harbors

Safe harbors matter because they change the burden of proof posture in an audit context: if you qualify, the regulations provide a presumption of reasonableness for FMV that the IRS can only rebut with certain kinds of evidence.5 That is why startups pay for independent appraisals even when everyone “knows” the company is valuable—credibility and process matter as much as the final number.

What employees should not do

- Do not assume you can “fix” a broken grant with a verbal side agreement.

- Do not assume a low strike is always “free money”—it can be tax friction later if the arrangement is noncompliant.

- Do not treat investor SAFEs or convertible notes as a substitute for common FMV; they are different instruments with different economics (see SAFE notes for early employees for context on early-stage capitalization).

FMV, Strike Price, and the Employee Experience

Definitions that actually matter on the grant letter

For private company options, employers typically set the exercise price based on common stock FMV on the grant date (subject to plan rules and corporate approvals). If you are granted nonqualified stock options (NSOs), the tax rules are different from incentive stock options (ISOs)—but 409A is still part of the reason companies maintain a disciplined valuation process. Use ISO vs NSO as a companion if you are deciding whether ISO treatment is even available for your grant.

A simple numeric example (illustrative)

Assume a 409A report supports common stock FMV = $2.00 on the grant date. If you receive an option with a $2.00 strike, you are not getting an instant accounting “bargain” at grant in the way tax counsel worries about for discounted options. If instead the company granted you a $0.50 strike while FMV is $2.00, that mismatch is the kind of fact pattern that can create 409A issues for a nonqualified arrangement (depending on plan structure and compliance).

| Term | Typical employee-facing meaning |

|---|---|

| FMV | The company’s supported value per share of common stock on a valuation date |

| Strike / exercise price | What you pay per share when you exercise (unless a cashless/net exercise program applies) |

| Preferred price | Often reflects different security economics—not automatically your strike price |

How this connects to offer negotiation

Employees sometimes compare offers using share counts alone. A healthier first pass is to compare strike, vesting, post-termination exercise windows, and company stage together. If you are new to equity, start with first-time stock options and how to read your equity grant.

Figure 2: Preferred valuation and common FMV can diverge—this is normal in venture-backed capital structures.

Safe Harbors (What “Presumption of Reasonableness” Means)

The tax regulations under Section 409A include detailed rules for establishing FMV for purposes of stock rights granted by private companies. In practice, companies often aim to fit within a safe harbor because a qualifying valuation can provide a presumption of reasonableness that the IRS can only rebut with certain types of evidence.5

Common safe-harbor buckets (high level)

| Safe harbor theme | Plain-language idea |

|---|---|

| Independent appraisal | A qualified appraiser values common stock using standard methods and documentation. |

| Board valuation | A defined process exists for a contemporaneous board determination within regulatory constraints. |

| Illiquid stock presumptions | Narrower rules can apply for qualifying “illiquid stock” of a start-up corporation within limits. |

Employees rarely “choose” a safe harbor personally—but you can ask whether the company’s process is documented, dated, and refreshed when events change the business.

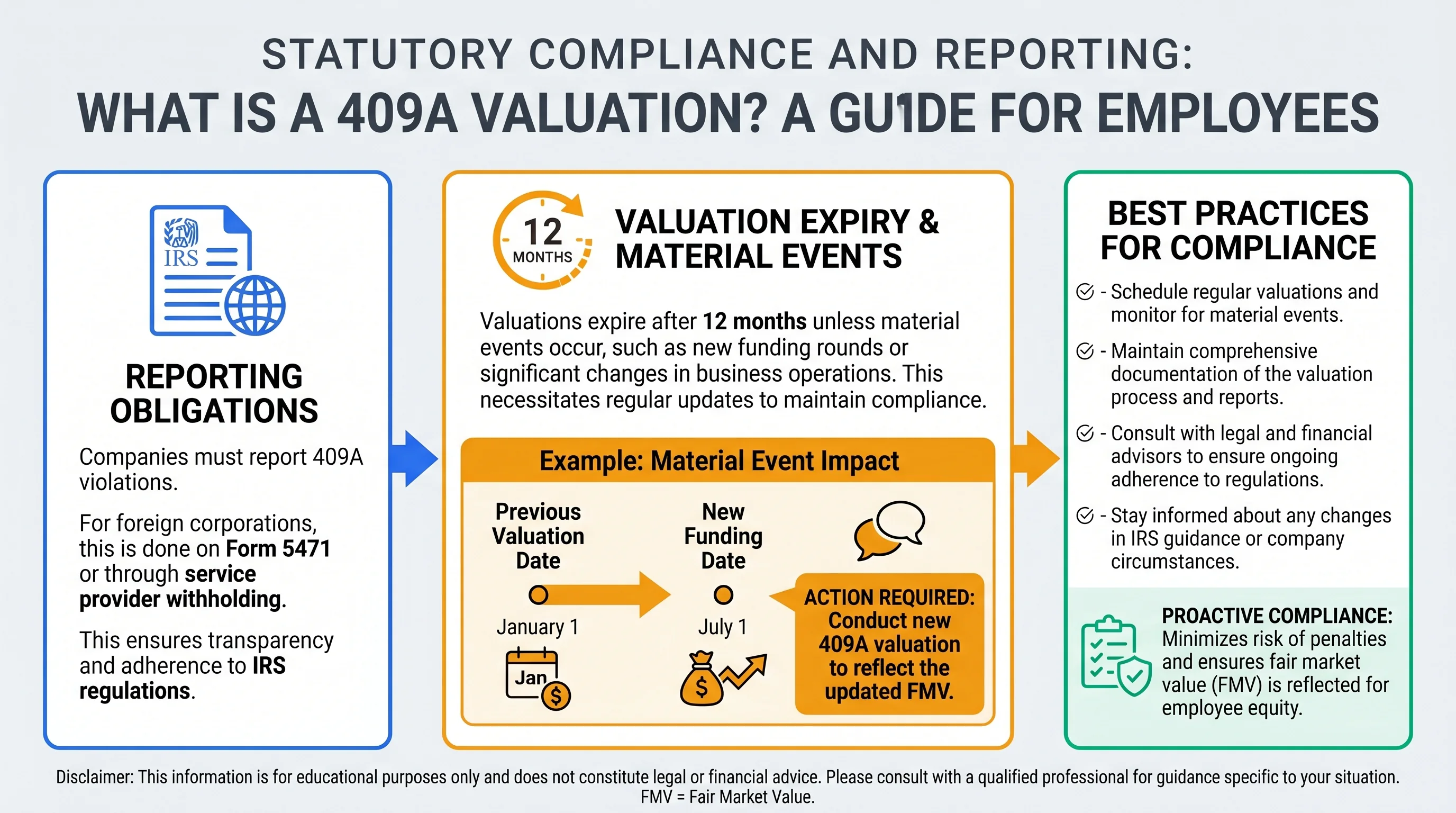

Material events: when companies refresh FMV

Most employees first notice 409A when FMV jumps after fundraising. A new round often implies new enterprise value, new capital structure, and sometimes a new risk profile—so a stale valuation may not be credible.

If you want the employee-facing angle on valuation resets after a down round, read down round 409A reset.

Figure 3: Think “calendar refresh + event-driven refresh,” not “one valuation forever.”

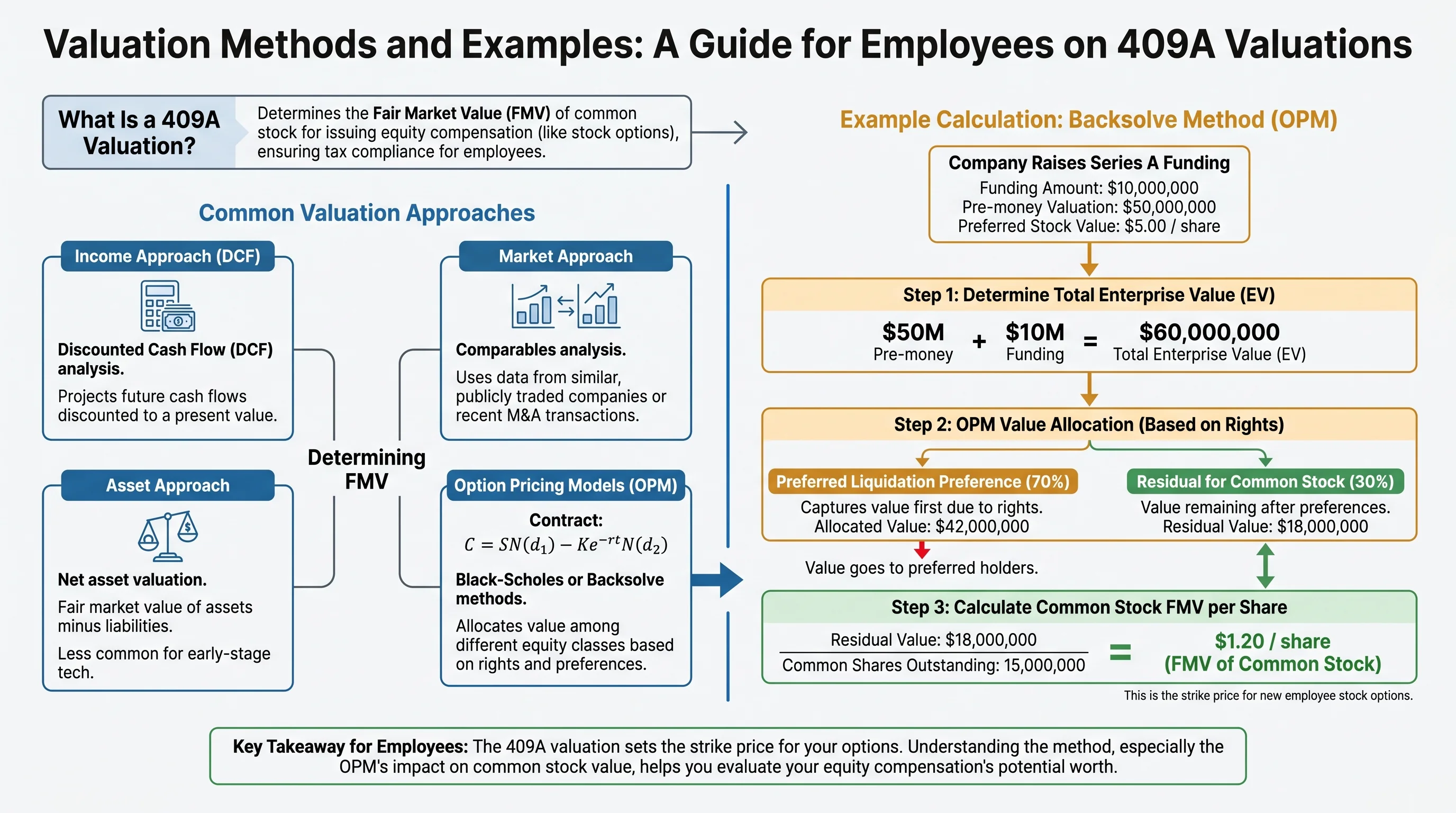

Valuation Methods Employees Hear About (Without Becoming Appraisers)

Appraisers combine facts and judgment. Common method families include:

- Market approaches (comparable companies and transactions—when data exists)

- Income approaches (cash-flow-driven value—when forecasting is credible)

- Back-solve / option-model approaches (infer common value implied by a recent preferred financing)

Many tech employees hear OPM backsolve referenced after a priced round. The intuition is: once you know something credible about enterprise value and capital structure, you can allocate value across classes—and apply discounts like DLOM (discount for lack of marketability) where appropriate.

| Method family | When it shows up |

|---|---|

| Back-solve / OPM | After a financing defines preferred pricing |

| DCF / income | When management forecasts support it |

| Market comps | When comparable public companies exist |

ISO vs NSO: Why 409A Shows Up in Both Conversations

ISOs have their own statutory requirements under IRC Section 422 (including pricing and holding period rules). NSOs are generally more flexible for companies but do not offer ISO’s potential tax benefits.

Even when ISO treatment is available, companies still care about 409A compliance across the equity program because many plans include NSOs, RSUs, or hybrid structures. If you are modeling exercise decisions, pair this article with early exercise strategies only as a conceptual overview—execution depends on your grant and 83(b) timing rules.

Practical Employee Checklist (Questions Worth Asking)

These are not “gotcha” questions—they are normal diligence questions for anyone whose compensation is increasingly equity-weighted:

- What is the current 409A FMV used for new grants, and when was it approved?

- Did a financing or acquisition term sheet arrive since that date?

- For each grant: ISO or NSO, strike, vesting, and post-termination exercise window?

- If you are exercising early: was 83(b) required, and was it filed in time? (See how to file an 83(b).)

- If you are joining near a round: will you be granted pre-round or post-round pricing?

Illustrative Scenarios (How Employees Actually Experience 409A)

Scenario A: You join a Series B company

You receive an option with a strike of $4.75. Six months later, after a new financing closes, new hires receive $7.10. That change often reflects a refreshed common FMV supported by a new valuation report—not “the company randomly decided to be mean.”

Scenario B: You want to early-exercise unvested shares

Some plans allow early exercise of NSOs or ISOs into restricted stock. The interaction of Section 83, Section 422 holding periods, and 409A compliance is a three-way coordination problem. This is one of the highest-leverage moments to pay for advice—mistakes can be irreversible if an 83(b) deadline is missed.

Scenario C: You are comparing two offers with very different strikes

Offer 1 gives more shares but a higher strike; Offer 2 gives fewer shares but a lower strike. Without FMV and liquidity context, you cannot rank the packages. Ask for grant date FMV, fully diluted share count (understanding it is imperfect), and exercise window on termination.

| Decision input | Why it matters |

|---|---|

| FMV trend | Rising FMV can mean less “bargain” at grant but also signals enterprise progress |

| Exercise window | Short windows force cash decisions at job changes |

| ISO vs NSO mix | Changes tax modeling and AMT exposure |

Frequently Asked Questions

Does a 409A valuation tell me what my shares will be worth at an IPO?

Answer: No. It estimates common stock FMV for a specific date under a compliance and appraisal framework. Public market pricing later can be higher or lower.

Source: IRC Section 409A

Why did my strike price increase after a funding round?

Answer: Because post-money capital structure and enterprise value often imply a higher common FMV than before, and companies typically refresh 409A studies after material events.

Source: Treas. Reg. §1.409A-1(b)(5)(iv)

Is the 409A price the same as the preferred price investors paid?

Answer: Usually not. Preferred stock and common stock are different economic interests; employee options are typically tied to common FMV.

Source: Treas. Reg. §1.409A-1(b)(5)

What happens if a company grants options below FMV?

Answer: Depending on facts, nonqualified discounted options can create Section 409A inclusion and penalty exposure. This is why companies invest in valuations and process.

Source: IRC Section 409A(a)(1)(B)

Do I need my own appraiser?

Answer: Typically no—the company obtains the valuation. Employees hire professionals for exercise planning, AMT, or cross-border issues.

Source: IRS — Nonqualified deferred compensation (409A)

How often should 409A be updated?

Answer: Many companies treat valuations as valid for up to 12 months absent intervening events, but material changes can require an earlier refresh. Your company’s counsel and appraiser document the cadence.

Source: Treas. Reg. §1.409A-1(b)(5)(iv)(F)

Does Section 409A apply to RSUs?

Answer: RSUs are usually structured to be taxed as wages when settled; the core 409A valuation conversation is often most visible for stock options and certain deferred equity features. Still, companies may coordinate RSU and option programs under one equity compliance policy.

Source: IRS Publication 525 (taxable income overview)

What should I do if my employer will not share FMV context?

Answer: Ask for grant date FMV support for your specific award (sometimes summarized in an offer or grant acknowledgment). If you are exercising, brokers and payroll teams may provide pieces—but you may still need a CPA for modeling.

Source: IRS Form 3921 instructions (ISO information returns)

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRC §409A | Statute | law.cornell.edu |

| Treas. Reg. §1.409A-1 | Regulation | law.cornell.edu |

| IRS — 409A overview | IRS | irs.gov |

| IRS Publication 525 | IRS | irs.gov |

Disclaimer: This guide discusses legal tax education and planning concepts only. Tax evasion is illegal. This content is not tax, legal, or investment advice. Consult a qualified professional before exercising options, filing elections, or making decisions based on FMV.

Footnotes

-

IRC Section 409A and related Treasury Regulations establish deferred compensation rules and valuation documentation expectations for stock rights granted by private corporations. ↩

-

Early exercise and restricted stock can involve Section 83 inclusion timing and 83(b) elections; these rules are separate from—but often coordinated with—409A planning. ↩

-

See the statutory text at 26 U.S.C. §409A. ↩

-

Penalty and inclusion mechanics appear at 26 U.S.C. §409A(a)(1)(B); confirm current rates and reporting with a professional. ↩ ↩2

-

Safe harbor frameworks for private company stock valuations are outlined in Treas. Reg. §1.409A-1(b)(5)(iv). ↩ ↩2