Executive Summary

What is a parachute payment under §280G?

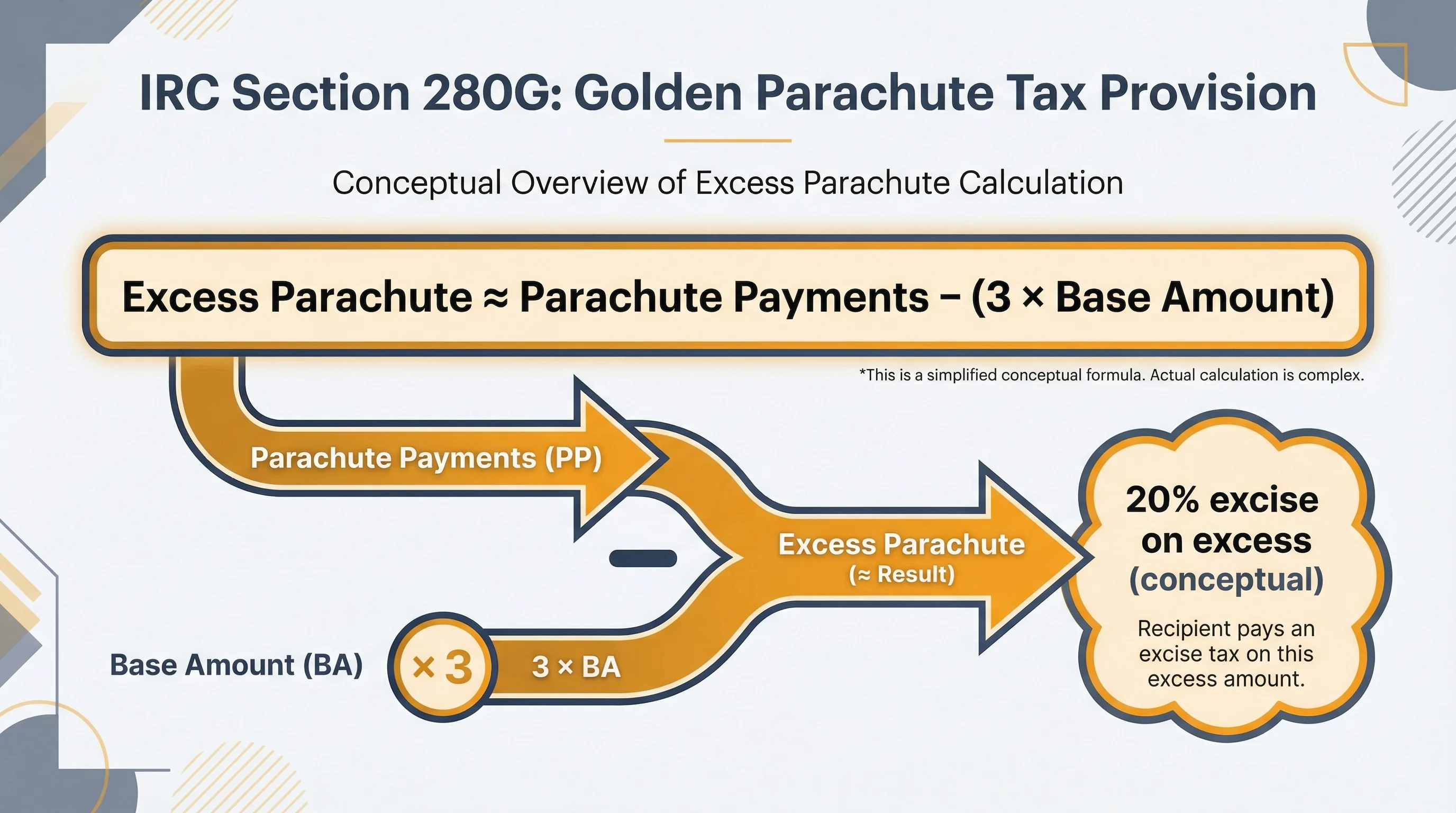

Very generally: compensation contingent on a change in ownership or control that exceeds 3 times the individual’s base amount (with statutory definitions). The rules distinguish parachute payments from ordinary compensation and can include equity acceleration, severance, and certain bonuses—subject to complex exclusions.

Who pays the 20% excise tax?

Typically the disqualified individual on the excess parachute amount, reported with federal tax filings—subject to specific mechanics and coordination with other taxes.

Can the excise tax be avoided?

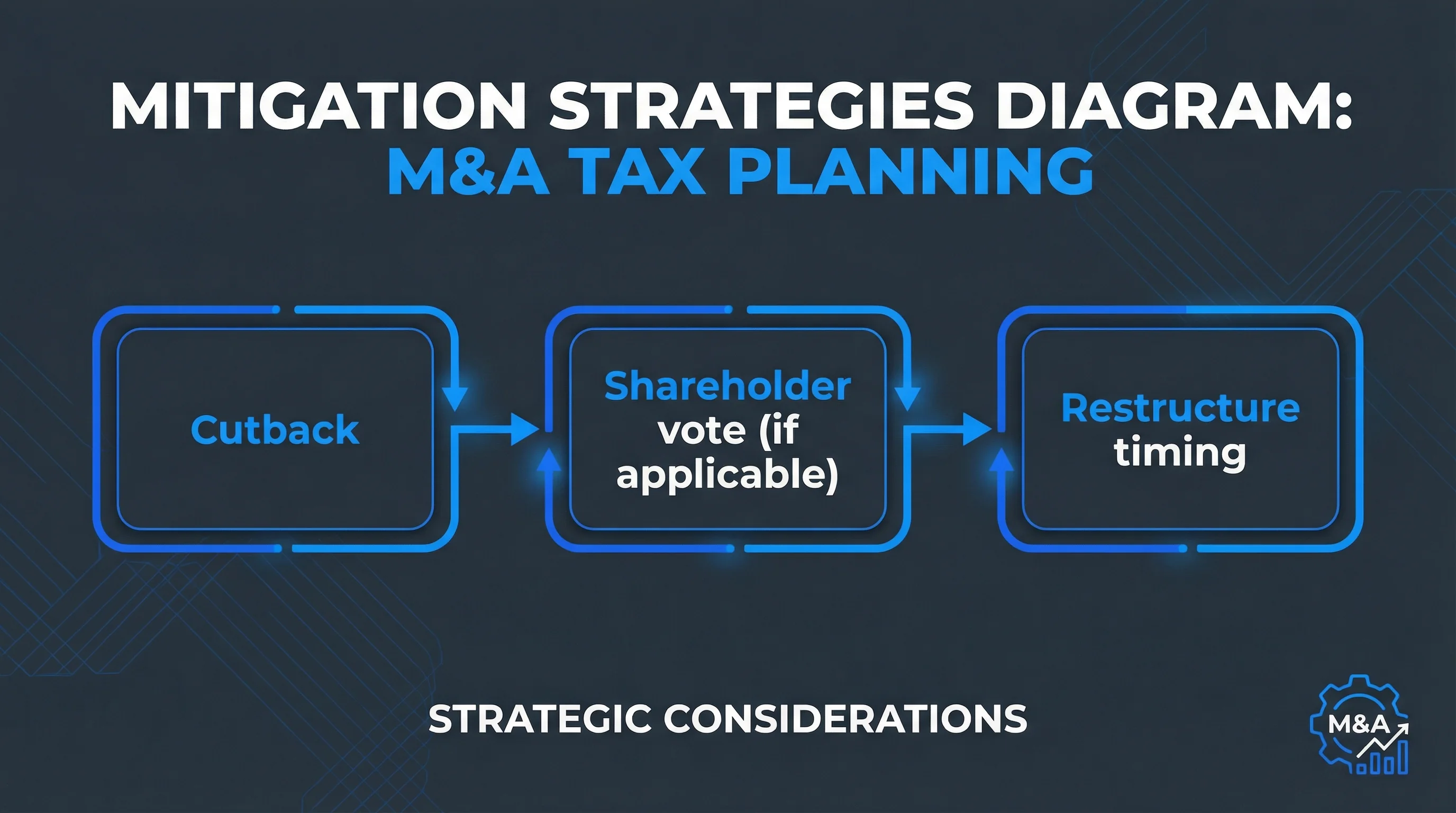

Sometimes through cutbacks (reducing payments below thresholds), shareholder approval where permitted, or restructuring compensation timing and characterization. There is no one-size-fits-all strategy—legal and tax advisors model scenarios in diligence.

Golden parachute rules exist because Congress wanted to limit tax-favored windfalls in corporate takeovers. For employees, the issue is not just headline severance—it is whether accelerated vesting, lump sums, and transaction bonuses stack into parachute treatment.

Pair with our M&A equity guide and the 280G calculator.

Figure 1: Core mechanical idea—statutory definitions and exclusions still apply.

Core Concepts (Mechanics-Level, Not Advice)

| Term | Plain-language hook |

|---|---|

| Disqualified individual | Officers, shareholders, and highly-compensated roles meeting statutory tests |

| Base amount | Generally average annual compensation over a 5-year lookback (details matter) |

| Parachute payment | Payments contingent on change in ownership/control, with exclusions |

| Excess | Amount above 3× base (if threshold tests are met) |

Why This Shows Up in Tech M&A

- Single-trigger acceleration can create large ordinary income events—see vesting acceleration.

- Retention bonuses may be layered on top of equity acceleration.

- Buyers model 280G exposure early because deductibility and employee excise affect net cost.

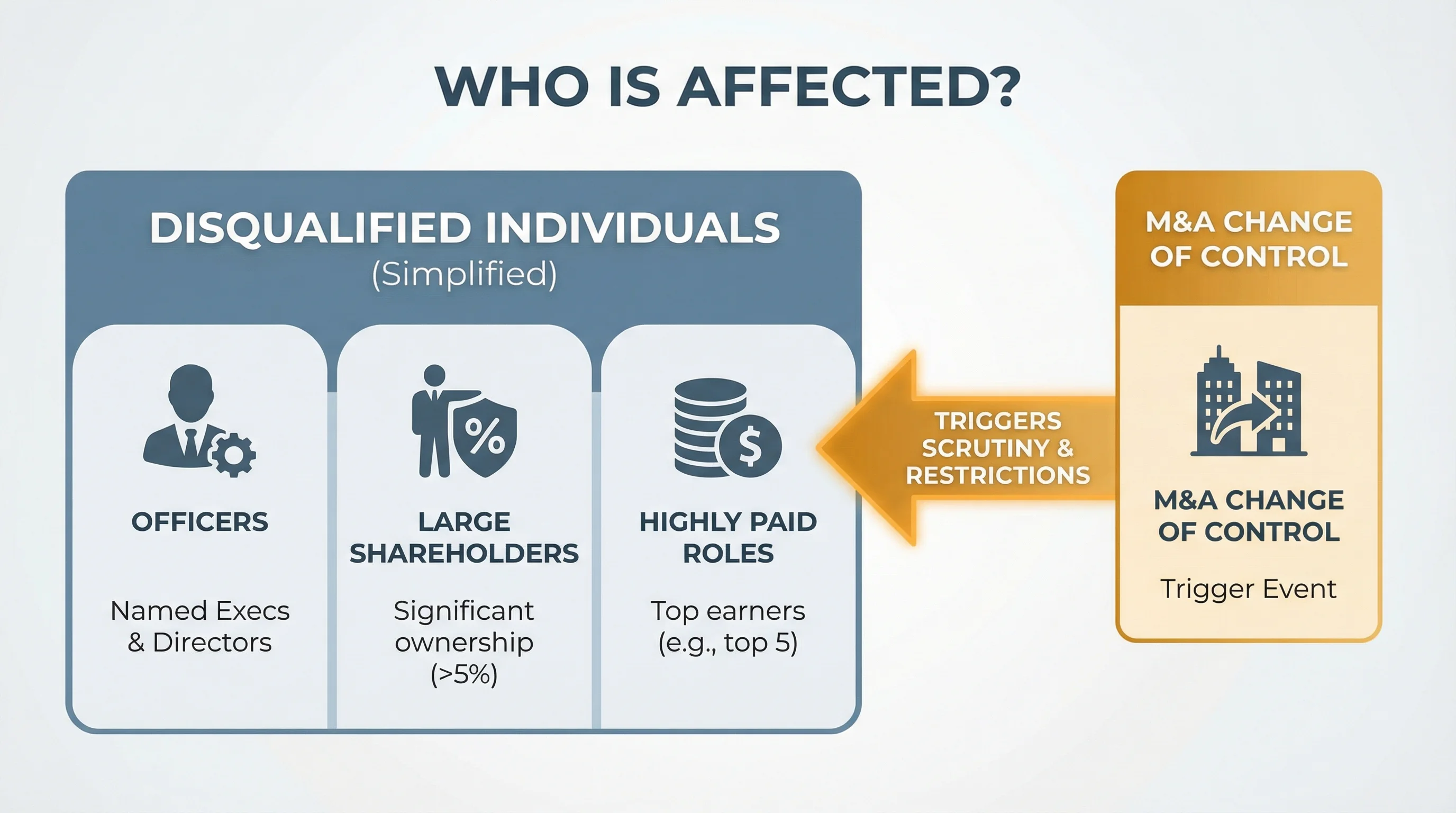

Figure 2: Who gets modeled in diligence depends on facts and tests—not job title alone.

Mitigation Playbook (Overview)

| Strategy | Idea |

|---|---|

| Cutback | Reduce payments to stay below excess thresholds |

| Shareholder vote | Certain private company procedures may help—counsel required |

| Recharacterize / defer | May be possible in some structures—highly constrained |

| Insurance / gross-up | Sometimes negotiated for executives—taxable to employee |

Figure 3: Common planning themes—confirm what your transaction permits.

Coordination With Other Rules

- 409A still matters for deferred comp—see 409A guide.

- ISO/NSO treatment on assumption/substitution—ISO vs NSO.

Checklist

- Identify all contingent payments in the CIC definition

- Model base amount with payroll history

- Compare to 3× threshold and estimate excise

- Review equity acceleration as part of parachute math

Disclaimer

Educational only. §280G is complex and fact-specific. Consult M&A tax counsel before signing.

Primary sources

| Source | URL |

|---|---|

| IRC §280G | https://www.law.cornell.edu/uscode/text/26/280G |

| IRC §4999 | https://www.law.cornell.edu/uscode/text/26/4999 |