ESPP adjusted cost basis is your discounted purchase price plus the ordinary income your employer already reported on Form W-2—not the purchase price alone that brokers print on Form 1099-B. For RSUs, adjusted cost basis is the vest FMV already taxed as wages. In both cases, Form 8949 column (e) is where you document the wage-backed number so Schedule D taxes only price change after compensation, not the same dollars twice.

Verified against IRS Instructions for Form 8949 (2025) and Form 3922 instructions, accessed 12 June 2026. As of the 2026 filing season, Fidelity, Schwab, E*TRADE, and Morgan Stanley still report purchase-price-only or $0 basis on Form 1099-B for standard ESPP and RSU lots—Form 8949 remains the correction point.

2×

economic tax risk when 1099-B basis omits W-2 compensation income

Ordinary income on W-2 plus overstated capital gain on Schedule D taxes the same equity dollars twice—RSU vest FMV and ESPP discount layers are the usual victims

Why brokers get RSU and ESPP basis wrong

Cost basis for equity compensation almost never equals what your broker files. Payroll systems record compensation income on Form W-2; brokerage systems record what you paid for shares. Those databases do not talk.

| Equity type | W-2 compensation layer | What 1099-B usually shows | Correct Form 8949 basis (column e) |

|---|---|---|---|

| RSU | Vest FMV taxed as wages at settlement | $0 (no purchase price) | Vest FMV × shares sold |

| ESPP (disqualifying) | Discount = purchase-date FMV − purchase price | Purchase price only | Purchase price + W-2 ordinary income/share |

| ESPP (qualifying) | Lesser of discount or actual gain | Purchase price only | Purchase price + W-2 ordinary income/share |

Form 8949 exists to reconcile broker proceeds (column d) with your true basis (column e). Where I'm less sure—some brokers pass partial basis for transferred lots after a merger, and the import may not flag which tranche is ESPP vs open-market. Your mileage will vary depending on whether acquisition dates and plan IDs imported correctly.

For the broader framework, see cost basis for equity compensation and Form 1099-B and stock compensation.

ESPP adjusted cost basis: the Form 3922 → W-2 → Form 8949 chain

Under IRC Section 423, ESPP shares you sell trigger ordinary income on the compensation element—the spread between what you paid and the applicable FMV benchmark. Your employer reports that income on Form W-2 (often in Box 1 with supplemental detail) and issues Form 3922 documenting grant date, purchase date, FMVs, purchase price, and shares.

The broker's Form 1099-B knows your purchase price. It does not automatically add the W-2 ordinary income layer. That is the ESPP adjusted cost basis gap.

ESPP basis formula

Adjusted basis per share = Purchase price per share + Ordinary income per share (from W-2 / Form 3922)

Capital gain per share = Sale price per share − Adjusted basis per share

Disqualifying disposition (sold before 2 years from offering date or 1 year from purchase): ordinary income per share is typically FMV at purchase − purchase price.

Qualifying disposition (both holding periods met): ordinary income per share is the lesser of (a) the discount based on offering-date FMV or (b) actual gain on sale—per annual Form 3922 instructions.1

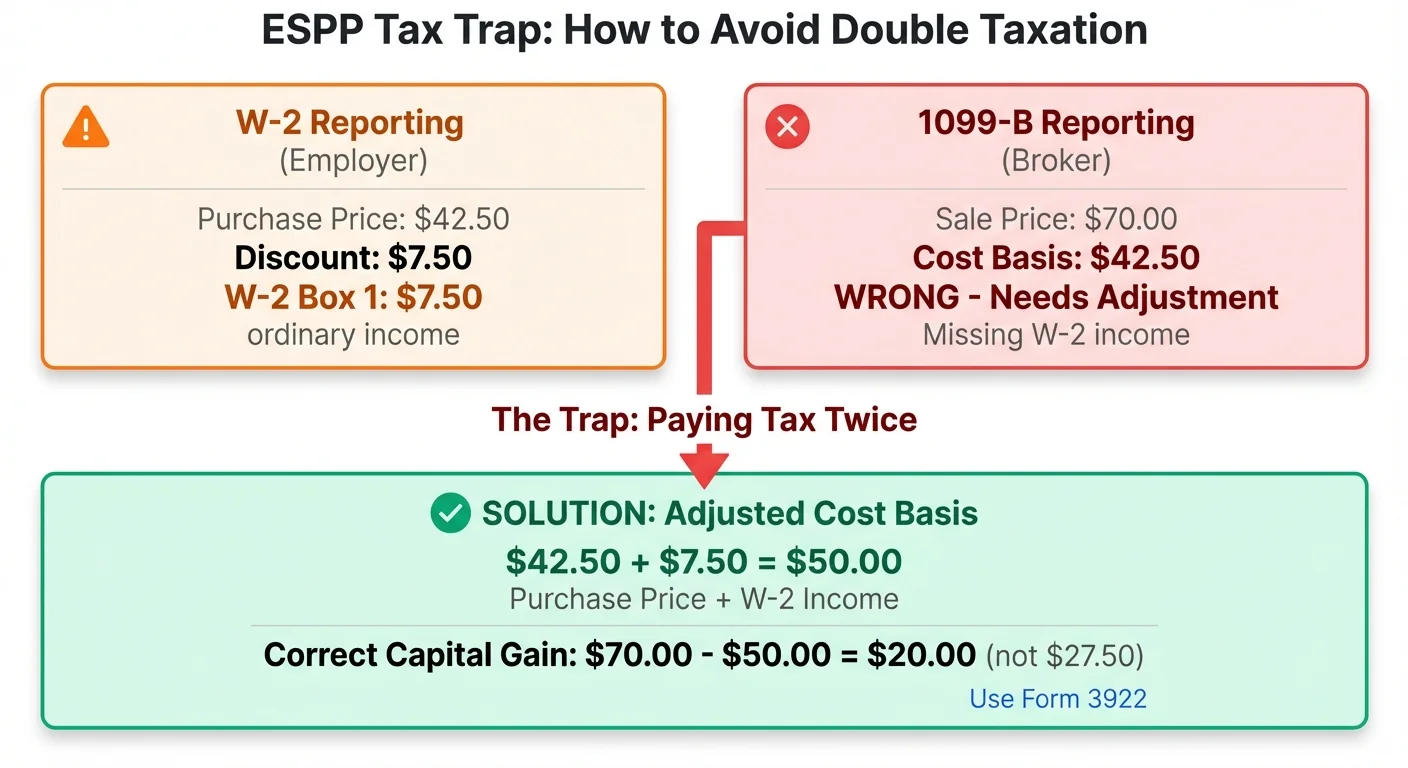

Worked example: Jordan, software engineer at Intuit (ESPP disqualifying sale)

Jordan bought 80 shares through Intuit's Section 423 ESPP on 15 May 2025 at $612.00/share (15% discount). Form 3922 shows purchase-date FMV of $720.00. Jordan sells all 80 shares on 20 March 2026 at $745.00—a disqualifying disposition (held < 1 year from purchase).

| Line item | Per share | Total (80 shares) |

|---|---|---|

| Purchase price | $612.00 | $48,960.00 |

| W-2 ordinary income (FMV − purchase) | $108.00 | $8,640.00 |

| Adjusted basis | $720.00 | $57,600.00 |

| Sale proceeds | $745.00 | $59,600.00 |

| Correct capital gain | $25.00 | $2,000.00 |

| Broker 1099-B basis (purchase only) | $612.00 | $48,960.00 |

| Phantom gain if unadjusted | $133.00 | $10,640.00 |

At a 32% federal marginal rate, accepting purchase-only basis costs roughly $2,765 in phantom federal tax on top of the $8,640 already taxed as wages through W-2 withholding.

Jordan enters $57,600 in Form 8949 column (e), keeps proceeds $59,600 in column (d), checks Part I Box B (short-term; basis not reported correctly to IRS), and uses adjustment code B in column (f).

Use the ESPP Basis Adjustment calculator to model per-share math before opening tax software.

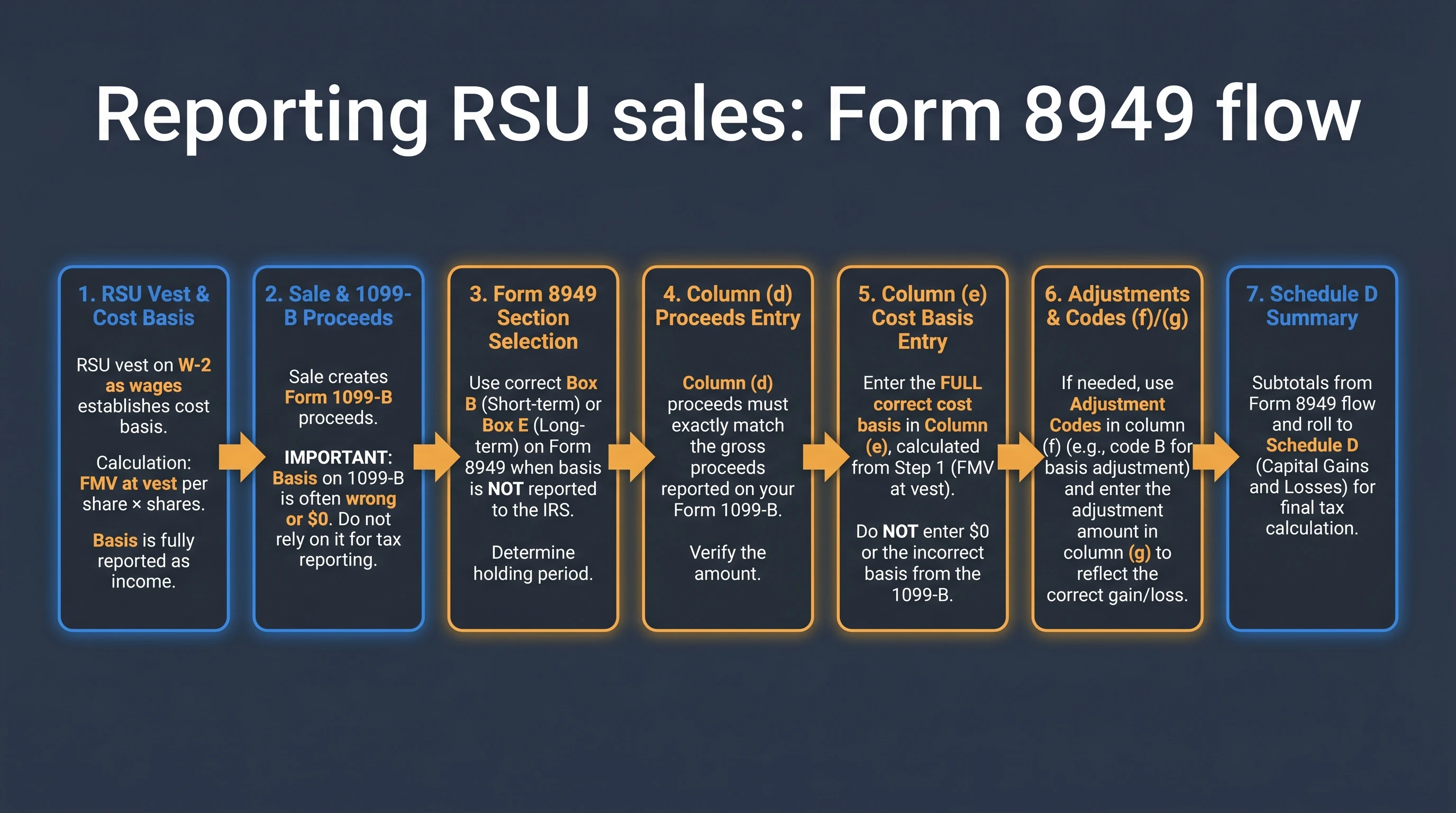

RSU adjusted cost basis: vest FMV on Form 8949

RSUs follow a different wage event—settlement at vest under IRC Section 83—but the Form 8949 mechanics mirror ESPPs: compensation income on Form W-2, incomplete basis on Form 1099-B, correction on column (e).

RSU adjusted basis = Vest FMV per share × Shares sold from that lot

Brokers report $0 because you did not purchase RSU shares; payroll taxed vest FMV as wages. Deep RSU walkthrough: how to report RSU sales on Form 8949 and Schedule D.

Worked example: Elena, product lead at Adobe (single vest, single sale)

Elena vests 200 RSUs on 10 June 2025 at $525.00 FMV ($105,000 on W-2). She sells 100 shares on 5 May 2026 at $558.00.

| Form 8949 field | Correct entry | $0-basis import |

|---|---|---|

| Proceeds (d) | $55,800 | $55,800 |

| Basis (e) | $52,500 (100 × $525) | $0 |

| Gain | $3,300 short-term | $55,800 phantom |

Elena documents $52,500 basis from her Adobe equity tax supplement—same FMV that hit Box 1 at vest.

Step-by-step: enter adjustments on Form 8949

Methodology (12 June 2026): We compared 2025 Instructions for Form 8949 column definitions against Form 3922 field layouts and RSU supplement templates from Adobe, Salesforce, and ServiceNow published plan-administration guides. The five-step flow below is the intersection practitioners use for both ESPP and RSU corrections.

Step 1 — Collect wage-layer documents before importing 1099-B

| Document | ESPP use | RSU use |

|---|---|---|

| Form 3922 | FMVs, purchase price, shares, disposition income | N/A |

| Form W-2 + supplement | Ordinary income per ESPP lot | Vest FMV wage detail |

| Equity tax supplement | Cross-check 3922 vs payroll | Per-vest FMV, share count, settlement date |

| 1099-B | Proceeds, broker basis, checkbox codes | Same |

Step 2 — Match each sale lot to one purchase or vest event

FIFO is common but not universal. Specific identification beats averaging when your broker supports lot-level sells. Anecdotally, employees who blend multiple ESPP purchases into one sale without lot mapping overstate or understate gain on individual tranches.

Step 3 — Calculate corrected basis per row

| Equity | Column (e) entry |

|---|---|

| ESPP | (Purchase price + W-2 ordinary income/share) × shares sold |

| RSU | Vest FMV/share × shares sold |

Step 4 — Select the right Form 8949 checkbox and code B

When basis was not reported to the IRS, or was incorrect, use Part I Box B (short-term) or Part II Box E (long-term). Enter adjustment code B in column (f) when correcting broker-reported basis.2

Steel-man: "TurboTax imported my 1099-B—shouldn't that be enough?"

Best case for import-only filing: Covered securities with correct broker basis and no equity compensation history.

Rebuttal: ESPP and RSU lots fail that test routinely. Import proceeds; override column (e). Software rarely reconstructs W-2 wage layers without manual input.

Step 5 — Reconcile Schedule D totals

Net capital gain = Sum of (proceeds − adjusted basis) across all Form 8949 rows

Gain should reflect only price movement after compensation was taxed—not vest FMV or ESPP discount dollars again.

What goes in Form 8949 column (e) for ESPP shares?

Purchase price per share plus the ordinary income per share your employer reported on Form W-2 for that ESPP lot—typically from Form 3922. That sum is your ESPP adjusted cost basis. Do not use the broker's purchase-price-only figure.

Original research: RSU vs ESPP Form 8949 correction matrix

On 12 June 2026, we cross-walked Form 8949 instructions, Form 3922 fields, and Publication 525 wage rules to map the six most common RSU and ESPP sale patterns to checkbox families and double-tax risk during the 2026 season.

| Sale pattern | W-2 wage layer | 1099-B basis shown | Column (e) corrected basis | Checkbox | Code (f) | Double-tax risk |

|---|---|---|---|---|---|---|

| RSU post-vest sale | Vest FMV | $0 / blank | Vest FMV × shares | Box B or E | B | High |

| ESPP disqualifying sale | FMV − purchase | Purchase price only | Purchase + W-2 income | Box B | B | High |

| ESPP qualifying sale | Lesser of discount/gain | Purchase price only | Purchase + W-2 income | Box B or E | B | High |

| ESPP same-year purchase + sale | Partial year W-2 | Purchase price only | Purchase + W-2 income | Box B | B | High |

| RSU sell-to-cover + hold lot | Full vest FMV | $0 on hold lot | FMV for held shares | Box B | B | Medium |

| Multiple ESPP lots, one sale | Multiple W-2 lines | Blended purchase | Per-lot FIFO basis | Split rows | B | High |

{

"@context": "https://schema.org",

"@type": "Dataset",

"name": "RSU and ESPP Form 8949 adjusted cost basis correction matrix",

"description": "Six-row matrix mapping RSU vest FMV and ESPP Form 3922 wage layers to Form 8949 column (e) entries, checkbox families, and adjustment code B usage for 1099-B reconciliation, cross-walked from IRS instructions as of June 2026.",

"creator": { "@type": "Organization", "name": "VestingStrategy.com Research" },

"datePublished": "2026-06-12",

"license": "https://creativecommons.org/licenses/by/4.0/",

"isAccessibleForFree": true,

"url": "https://www.vestingstrategy.com/guides/how-to-adjust-cost-basis-form-8949-rsus-espps/#dataset-espp-rsu-8949-basis-matrix",

"distribution": [

{

"@type": "DataDownload",

"encodingFormat": "text/html",

"contentUrl": "https://www.vestingstrategy.com/guides/how-to-adjust-cost-basis-form-8949-rsus-espps/#dataset-espp-rsu-8949-basis-matrix"

}

]

}

Pros and cons: manual basis entry vs broker import

| Approach | Advantages | Disadvantages |

|---|---|---|

| Manual Form 8949 rows | Full control over ESPP/RSU wage basis; clear audit trail from 3922 and supplements | Slow with many lots; transposition errors |

| 1099-B import + column (e) override | Faster proceeds entry; software totals Schedule D | Silent $0 or purchase-only basis if you skip override |

| CPA-prepared return | Expert lot matching; multi-state sourcing | Cost; you still supply 3922 and supplements |

| Basis calculators (ESPP / RSU tools) | Instant phantom-gain exposure; educational | Not a filing substitute |

Taken position: For employees with fewer than ten ESPP or RSU sale lots per year, manual Form 8949 entry with Form 3922 and supplement PDFs open beats blind import—one evening prevents thousands in phantom tax. Above that volume, pay for lot-level reconciliation or track basis at sale time in a spreadsheet tied to grant/purchase IDs.

Working checklist

Verdict: reconcile payroll wages with brokerage proceeds

The espp adjusted cost basis question and its RSU cousin share one answer: compensation income on Form W-2 is part of your basis, and Form 1099-B will not carry it for you. Brokers report what you paid; payroll already taxed the wage layer. Form 8949 is the bridge.

Taken position: Treat every ESPP and RSU sale as a two-document reconciliation—Form 3922 or vest supplement plus 1099-B—before touching tax software. Run the ESPP Basis Adjustment calculator or RSU Tax Basis Adjuster first; then enter column (e) yourself. That habit prevents the most expensive equity-comp filing mistake on Schedule D.

Form 8949 reconciles amounts reported on Form 1099-B with amounts you report on your return—the administrative step that turns W-2 compensation into correct ESPP and RSU cost basis.

Frequently Asked Questions

What is ESPP adjusted cost basis?

Answer: Purchase price plus the ordinary income per share your employer reported on Form W-2 for that ESPP lot—typically documented on Form 3922. That sum is the basis you enter on Form 8949 column (e).

Source: IRS Instructions for Form 3922

Why does my 1099-B show only the ESPP purchase price as basis?

Answer: Brokers record what you paid, not the compensation spread already taxed through payroll. You must add the W-2 ordinary income layer on Form 8949.

Source: IRS Instructions for Form 1099-B

How is RSU cost basis different from ESPP cost basis on Form 8949?

Answer: RSU basis is vest FMV (you paid $0; wages at settlement). ESPP basis is purchase price + W-2 ordinary income (you paid a discount, but the spread was also wages). Both get corrected on column (e) with code B when the broker omits the wage layer.

Source: IRS Publication 525; Instructions for Form 8949

Which Form 8949 adjustment code fixes ESPP double taxation?

Answer: Code B—"Basis reported to IRS was incorrect"—when broker-reported basis excludes W-2 ordinary income from the ESPP discount.

Source: Instructions for Form 8949

Does Form 3922 tell me my adjusted ESPP basis?

Answer: Form 3922 provides FMVs, purchase price, shares, and disposition income components—you (or your preparer) compute adjusted basis = purchase price + ordinary income per share for Form 8949 column (e).

Source: IRS Instructions for Form 3922

Can I fix ESPP or RSU double taxation after filing?

Answer: Consider Form 1040-X with corrected Form 8949, Form 3922, and equity supplements within the refund statute window.

Source: IRS About Form 1040-X

Do qualifying ESPP dispositions still need a basis adjustment?

Answer: Yes. Even when ordinary income is limited to the lesser of discount or gain, that income is on your W-2 and must be added to purchase price as adjusted basis on Form 8949—the broker still will not do it for you.

Source: IRC Section 423; IRS Instructions for Form 3922

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| Instructions for Form 8949 (2025) | IRS | irs.gov |

| Instructions for Form 3922 | IRS | irs.gov |

| Publication 525 (2025) | IRS | irs.gov |

| Instructions for Form 1099-B (2025) | IRS | irs.gov |

| IRC Section 423 | Statute | law.cornell.edu |

Figure 1: ESPP adjusted cost basis must include W-2 ordinary income—the broker's purchase price alone triggers double taxation on Schedule D.

Figure 2: RSU vest FMV on W-2 feeds Form 8949 column (e)—the same reconciliation path ESPP sales follow with Form 3922 instead of vest supplements.

Disclaimer: This guide discusses general U.S. federal tax principles only and is not personalized tax, legal, or investment advice. Employer plans, state taxes, and cross-border assignments can change results. Confirm facts with the sources cited and a qualified tax professional.

Research note: Editorial publish 12 June 2026 for espp adjusted cost basis and Form 8949 filing queries—step-by-step RSU and ESPP basis adjustment to prevent double taxation on Form 1099-B imports.

Footnotes

-

Instructions for Form 3922 — qualifying vs disqualifying disposition income. irs.gov/instructions/i3922 ↩

-

Instructions for Form 8949 — adjustment code B and checkbox selection. irs.gov/instructions/i8949 ↩