Executive Summary

What is a Section 83(b) Election and How Can It Benefit You?

A Section 83(b) election allows recipients of restricted stock to pay taxes on the total fair market value at the time of granting rather than at vesting, potentially reducing tax liability by recognizing income early and benefiting from lower rates or future appreciation taxed as capital gains.

The intricacies of tax law provide numerous opportunities and pitfalls for taxpayers, particularly those receiving restricted stock or options as part of their compensation. Among these, the Section 83(b) election stands out as a powerful tool for managing tax liabilities. This guide delves into the mechanics, benefits, and considerations of making an 83(b) election, alongside broader tax strategies such as offsetting capital gains, understanding net loss deduction limits, navigating the wash-sale rule, and leveraging reinvestment strategies.

Searches for “IRS 83(b) election 30 days official” or “Treasury Regulation 1.83-2”: the 30-day clock and filing mechanics are set out in Treasury Regulation §1.83-2; you file with the IRS using the current Form 15620 (and send a copy to your employer). IRS Publication 525 summarizes how restricted property fits into income—use it alongside this guide, not instead of your grant terms. Typical RSUs (pure promise to deliver shares later) are not eligible for 83(b) the way restricted stock or early exercise of options often is—see our RSU tax guide.

FAQ — “30 days from grant or transfer?” The election clock runs from transfer of property (when you receive the stock subject to risk of forfeiture), not from a vague “offer” date—match the date on your grant notice. FAQ — “Official IRS form?” Use Form 15620 (or a statement that meets the regulation’s content rules); keep proof of timely mailing or approved delivery. Official filing playbook: How to File an Official Section 83(b) Election with the IRS. Draft + mailing execution aids: IRS 83(b) Election Form Generator & Mailing Checklist. Step-by-step filing: How to file an 83(b) within 30 days.

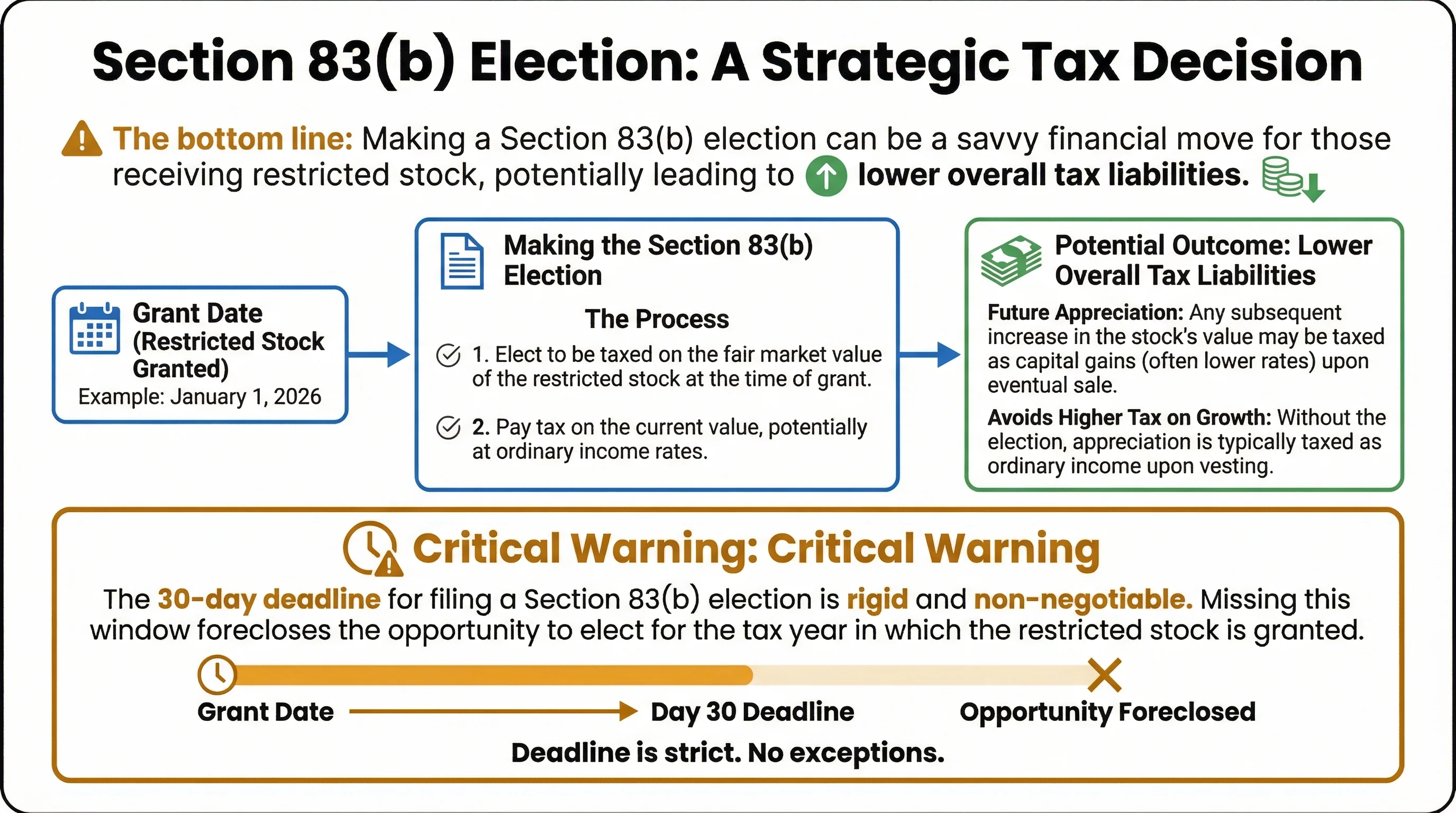

The bottom line: Making a Section 83(b) election can be a savvy financial move for those receiving restricted stock, potentially leading to lower overall tax liabilities. However, it requires careful consideration and timely action.

Critical Warning: The 30-day deadline for filing a Section 83(b) election is rigid and non-negotiable. Missing this window forecloses the opportunity to elect for the tax year in which the restricted stock is granted.

Section 83(b) Election: A Strategic Tax Decision

Definition and Core Mechanics

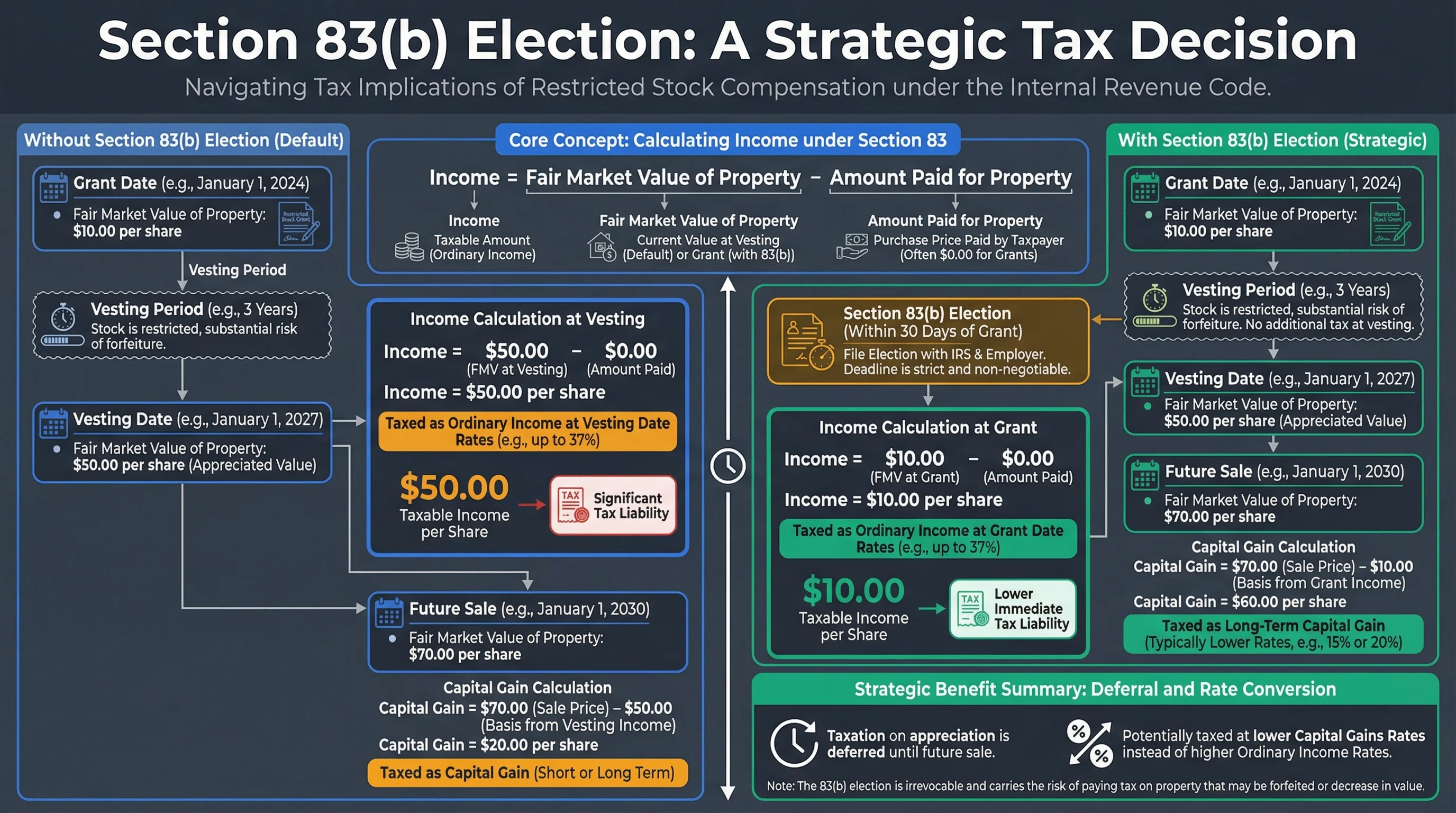

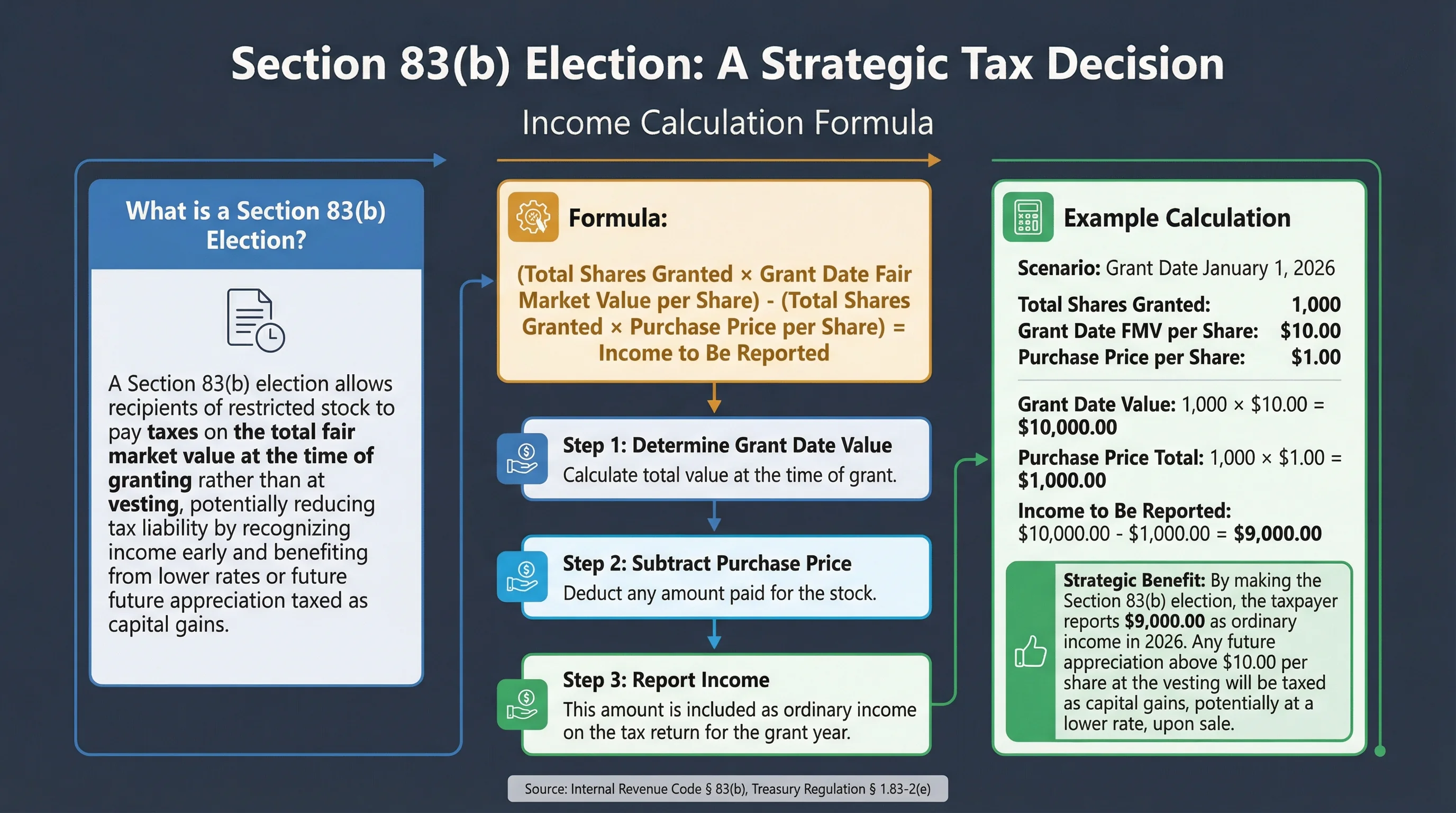

A Section 83(b) election is a tax strategy under the Internal Revenue Code § 83(b) that allows individuals receiving restricted stock or options as part of their compensation to accelerate their income recognition. Instead of paying taxes upon vesting, taxpayers can choose to include the fair market value of the property at the time of transfer in their gross income, potentially reducing their future tax liability.

Income Calculation Formula:

Gross Income = Fair Market Value of Property − Amount Paid for Property

Filing Requirements and Deadlines

The election must be filed within 30 days following the transfer of property, using either the IRS Form 15620 or a compliant statement. The deadline is strict, with no extensions available.

| Requirement | Specification |

|---|---|

| Deadline | 30 calendar days from property transfer (Board approval date) |

| Form | IRS Form 15620 (revised April 2025) |

| Signature | Original required; electronic signatures now permitted (June 2025 update) |

| Filing Location | IRS Service Center, Austin TX (for non-residents) |

| Delivery Method | Certified mail or IRS-designated private delivery (FedEx, DHL, UPS) |

| Copies Required | (1) IRS, (2) Employer, (3) Personal records |

Source: Treasury Regulation § 1.83-2(e)

Post-Filing Obligations and Revocation Restrictions

After filing, copies of the election must be provided to the employer and the IRS. Importantly, once made, the election cannot be revoked without IRS consent.

Strategic Considerations

Filing an 83(b) election can be advantageous if the stock's value is expected to rise significantly, as future appreciation is taxed as capital gains. However, if the stock's value decreases, taxpayers cannot reclaim taxes paid on the higher initial value.

Figure 1: Section 83(b) Election timeline — file within 30 days of grant to lock in low tax basis and qualify for long-term capital gains treatment on future appreciation.

Tax Impact Quantification: The Strategic Benefit

The financial benefit of filing an 83(b) election scales with company appreciation. Using the widely-cited Cooley LLP methodology:

Scenario Comparison: 100,000 Shares at $0.01 Grant Price

| Metric | With 83(b) Election | Without 83(b) Election | Difference |

|---|---|---|---|

| Grant Date FMV | $1,000 | $1,000 | — |

| Tax at Grant (37%) | $370 | $0 | +$370 |

| Vesting Date FMV | $100,000 | $100,000 | — |

| Tax at Vesting (37%) | $0 | $37,000 | -$37,000 |

| Exit Value ($5/share) | $500,000 | $500,000 | — |

| Capital Gain | $499,000 | $400,000 | — |

| Capital Gains Tax (20%) | $99,800 | $80,000 | +$19,800 |

| Total Tax Paid | $100,170 | $117,000 | -$16,830 |

| Net Proceeds | $399,830 | $383,000 | +$16,830 |

Key Insight: The savings of $16,830 represents a company that only grew from $0.01 to $5.00 per share. For high-growth startups reaching $50+ per share, the savings exceed $150,000 per 100,000 share grant.

Source: Cooley GO – Silicon Valley's leading startup law firm

The Mathematical Principle

83(b) Advantage = (FMV at Vest - FMV at Grant) × (Ordinary Rate - Cap Gains Rate)

For tech employees in the 37% federal bracket (plus California's 13.3%), the spread between ordinary income and long-term capital gains treatment can exceed 30 percentage points.

Figure 2: Section 83(b) Election income calculation formula and strategic benefits — demonstrates how to calculate taxable income and the potential tax savings from making the election.

Offset Capital Gains and Loss Deduction Limits

Capital Gains Tax Strategies

Taxpayers can use capital losses to offset capital gains, reducing their taxable income. The IRS allows a $3,000 annual deduction against ordinary income if capital losses exceed gains, with the ability to carry forward unused losses indefinitely.

Wash-Sale Rule

The wash-sale rule prevents taxpayers from claiming a tax deduction for a security sold at a loss if a substantially identical security is purchased within 30 days before or after the sale. This rule aims to discourage selling securities at a loss simply to claim a tax benefit.

| Rule Component | Specification |

|---|---|

| Time Window | 30 days before or after sale |

| Substantially Identical | Same security or option on same security |

| Effect | Loss disallowed, added to basis of replacement security |

| Exception | Different security types (e.g., stock vs. ETF) |

Source: IRS Publication 550 – Investment Income and Expenses

Reinvestment Strategies

Investing in Qualified Opportunity Funds (QOFs) or utilizing like-kind exchanges under §1031 can defer capital gains taxes. These strategies allow for the reinvestment of gains into new properties or distressed areas, potentially deferring taxes and benefiting from basis step-ups.

Tech Stock Volatility and Tax Planning

Tax-Loss Harvesting

Active tax-loss harvesting can mitigate the impact of tech stock volatility on taxable income. By selling securities at a loss and immediately repurchasing similar assets, investors can realize losses for tax purposes while maintaining their market position.

Equity Compensation Tax Planning

For those with equity compensation in tech stocks, understanding the tax implications of Restricted Stock Units (RSUs) and Incentive Stock Options (ISOs) is crucial. Proper planning can minimize the tax burden associated with vesting and exercise.

Related Guides: For comparing stock option types, see our ISO vs NSO guide. For expats managing equity compensation, check our Section 83(b) guide for expats. For comprehensive RSU taxation, see our RSU tax guide. For AMT planning with stock options, see our AMT planning guide.

Figure 3: Section 83(b) Election tax implications comparison — side-by-side comparison of tax treatment with and without the election, showing the potential tax savings.

2026 Tax Law Changes and Implications

Federal Income Tax Brackets and Standard Deductions

The IRS adjusts tax brackets and standard deductions annually for inflation. For 2026, these adjustments reflect changes under the One Big Beautiful Bill Act, affecting taxpayers' strategies for income recognition and deductions.

Automated Tools and Platforms

The IRS's adoption of AI and machine learning for audit selection and compliance checks underscores the importance of accurate income reporting and reconciliation, especially with the introduction of Form 1099-DA for digital asset transactions.

When to File an 83(b) Election

Optimal Scenarios

| Scenario | Recommendation | Rationale |

|---|---|---|

| Early-stage startup with low grant value | ✅ File | Lock in low basis, future appreciation taxed as capital gains |

| High-growth potential company | ✅ File | Significant appreciation expected, maximize capital gains treatment |

| Certain you'll hold until sale | ✅ File | Benefit from long-term capital gains rates |

| High grant-date valuation | ⚠️ Consider carefully | May not want to accelerate tax recognition |

| Significant forfeiture risk | ❌ May not file | Risk paying tax on shares you never receive |

| Company likely to fail | ❌ Do not file | Tax paid at grant is non-recoverable |

Source: DWT Startup Law Blog

Frequently Asked Questions

Q1: Can I file an 83(b) election after the 30-day deadline?

No. The 30-day deadline is absolute and non-extensible per Treasury Regulation §1.83-2. There are no IRS remedies, no reasonable cause exceptions, and no penalty abatement options. If you miss the deadline, the election is permanently unavailable for that grant.

Source: 26 CFR § 1.83-2

Q2: What happens if the stock value decreases after I file?

If you file an 83(b) election and the stock value decreases, you cannot reclaim the taxes you paid on the higher initial value. The election is irrevocable, so you've essentially "locked in" the higher tax basis. This is why the election is most beneficial when you expect significant appreciation.

Source: IRS Publication 525

Q3: Do I need to file an 83(b) election for every grant?

Yes. Each grant of restricted stock requires its own 83(b) election. You must file a separate election for each grant within 30 days of that specific grant date.

Source: Treasury Regulation § 1.83-2(e)

Q4: Can I file an 83(b) election for stock options?

No. Section 83(b) elections apply only to restricted stock (property subject to substantial risk of forfeiture). Stock options are not eligible for 83(b) elections. However, ISOs and NSOs have their own tax treatment rules. Private company employees may have a different option: Section 83(i) qualified equity grants allow tax deferral on options and RSUs.

Source: IRS Publication 525

Q5: What information do I need to file an 83(b) election?

You'll need:

- Grant date

- Number of shares

- Fair market value per share at grant date

- Amount paid for the stock (if any)

- Your Social Security Number or TIN

- Employer's name and address

Source: IRS Form 15620 Instructions

Q6: How do I calculate the fair market value at grant?

For private companies, the fair market value is typically determined by a 409A valuation performed by an independent appraiser. For public companies, use the closing stock price on the grant date. Your employer should provide this information.

Source: IRS Revenue Procedure 2005-51

Q7: What if I'm not a US citizen or resident?

Non-US persons can file an 83(b) election, but the process may be more complex. You may need to use "Applied For" or "N/A" in the TIN field if you don't have a Social Security Number. See our Section 83(b) guide for expats for detailed information.

Source: Baker Tax Law

Q8: Can I revoke an 83(b) election?

No. Once filed, an 83(b) election is irrevocable without IRS consent, which is rarely granted. This is why careful consideration is essential before filing.

Source: Treasury Regulation § 1.83-2(e)

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| Internal Revenue Code § 83(b) | Statute | https://www.law.cornell.edu/uscode/text/26/83 |

| Treasury Regulation § 1.83-2(e) | Regulation | https://www.law.cornell.edu/cfr/text/26/1.83-2 |

| IRS Form 15620 | Form | https://www.irs.gov/pub/irs-pdf/f15620.pdf |

| IRS Publication 525 | Publication | https://www.irs.gov/pub/irs-pdf/p550.pdf |

| IRS Newsroom: 2026 Inflation Adjustments | Announcement | https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill |

| IRS Strategic Operating Plan FY 2023-2031 | Strategic Plan | https://www.irs.gov/strategicplan |

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Tax laws vary by jurisdiction and change frequently. Always consult a qualified tax professional (CPA, tax attorney, enrolled agent) before making decisions based on this information. The authors accept no liability for actions taken based on this content.

Last Updated: January 26, 2026

Research Team: VestingStrategy Editorial Team