Executive Summary

Are RSUs taxed twice under US federal tax law?

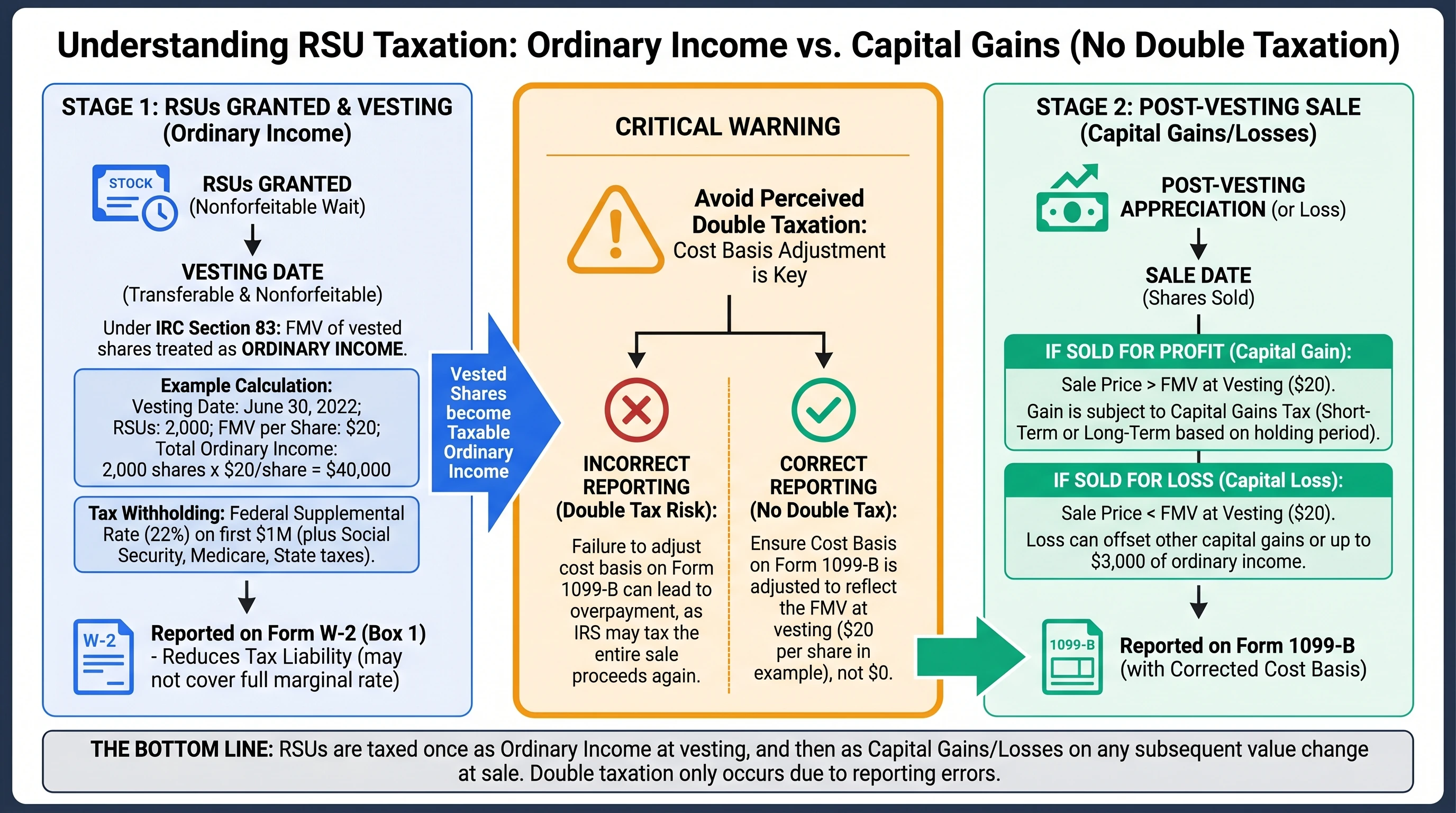

No, RSUs are not taxed twice. They are taxed as ordinary income at vesting and as capital gains on any post-vesting appreciation.

Restricted Stock Units (RSUs) are a popular form of equity compensation, especially in the tech industry. Understanding their taxation is crucial to avoid overpayment and ensure compliance with IRS regulations. RSUs are taxed at two distinct economic points: at vesting and at sale. At vesting, the fair market value (FMV) of the shares is treated as ordinary income and reported on Form W-2. When these shares are sold, any gain over the FMV at vesting is subject to capital gains tax. Those are different dollars, not the same income taxed twice.

If you want the full RSU framework first, start with our comprehensive RSU tax guide. If your question is specifically about basis and brokerage forms, pair this page with cost basis and double taxation on your tax return and Form 1099-B for stock compensation.

The bottom line: RSUs are not subject to double taxation if the cost basis is correctly reported and adjusted on tax forms.1

Critical Warning: Failure to adjust the cost basis on Form 1099-B can result in overpayment of taxes due to perceived double taxation.2

Ordinary Income Taxation at Vesting

Understanding IRC Section 83

Under IRC Section 83, RSUs are not considered substantially vested until they become transferable and nonforfeitable. At this point, the FMV of the vested shares is taxed as ordinary wage income, similar to a bonus. This income is reported in Box 1 of Form W-2 and is subject to federal income tax, Social Security, Medicare, and state taxes.

Example Calculation:

- Vesting Date: June 30, 2022

- Number of RSUs: 2,000

- FMV per Share: $20

- Total Ordinary Income: 2,000 shares × $20/share = $40,000

The employer withholds taxes at a 22% federal supplemental rate on the first $1 million, with a higher rate of 37% for amounts above this threshold. State taxes can add an additional 5-13%.

Tax Withholding and Reporting

Employers typically withhold a flat 22% for federal taxes on RSU vesting, which is considered supplemental wage withholding. This withholding is reflected on your W-2 and reduces your tax liability but may not cover the full amount if your marginal tax rate exceeds 22%.

Table: Federal Tax Withholding Rates

| Income Bracket | Federal Tax Rate |

|---|---|

| ≤ $1M | 22% |

| > $1M | 37% |

Important Note: If your marginal tax rate is higher than the withholding rate, you may owe additional taxes when filing your return.

Planning for Tax Payments

To avoid underpayment penalties, consider making estimated tax payments if your withholding is insufficient. This is particularly important for high-income earners whose marginal tax rate exceeds the supplemental withholding rate.

Example Calculation:

- Marginal Tax Rate: 37%

- Federal Withholding: 22% of $40,000 = $8,800

- Additional Tax Owed: 37% of $40,000 - $8,800 = $5,000

Table: Estimated Tax Payment Schedule

| Quarter | Due Date | Payment Amount |

|---|---|---|

| Q1 | April 15 | $1,250 |

| Q2 | June 15 | $1,250 |

| Q3 | September 15 | $1,250 |

| Q4 | January 15 | $1,250 |

Visual overview of how equity compensation layers ordinary income, basis, and later capital gains—educational only, not individualized tax advice.

Why It Feels Like Double Tax (Even When It Is Not)

Most “I was taxed twice on my RSUs” stories are really one of three things:

-

Withholding vs. true tax liability. Employers often use the flat 22% federal withholding rate on supplemental wages (for the portion that qualifies under the usual rules), but many tech employees have marginal federal rates of 32%–37%. You still owe the difference when you file. That is one tax liability settled in two cash flows (payroll withholding + April balance), not two taxes on the same income. For a deeper dive, see why 22% withholding may not be enough and our first-year RSU survival guide.

-

W-2 ordinary income + a 1099-B sale in the same year. It is easy to feel taxed twice when you see wage income on your W-2 and a broker sale on Form 1099-B. Legally, the wage piece is the same compensation component that should raise your basis. If you skip that adjustment, tax software may compute a gain on dollars you already paid ordinary income tax on—which is double taxation, but it is a reporting error, not a rule that RSUs are taxed twice by default.

-

Payroll taxes + income taxes. RSU vesting is generally wages. You may see federal income tax withholding, Social Security, Medicare (and state taxes), all on the same vest event. That is multiple taxes, but not the same tax twice.

Table: “Double tax” story vs. what is actually happening

| What you experienced | What is usually going on | What to verify |

|---|---|---|

| Big vest, then a tax bill at filing | Withholding was below your marginal rate | Safe harbor / estimated taxes; W-4 adjustments |

| 1099-B shows gain on RSU sale | Basis not adjusted to vest FMV | Form 8949; employer vest confirmation |

| Sold immediately after vest | Small ST gain/loss vs. vest FMV | Trade confirmations; per-lot basis |

Sell-to-Cover and Net Share Settlement: A Second Layer That Is Not a Second Ordinary Tax

Many plans “net settle” RSUs: the company withholds shares, sells a portion for taxes, and deposits net shares in your brokerage account. That tax sale is still a disposition for tax purposes. In practice:

- You recognize ordinary income on the gross RSU value at vest (what the plan reports for payroll), not only on the net shares you keep.

- The shares sold to cover withholding can produce a small capital gain or loss versus the per-share FMV at vest—often tiny if the sale is the same day, but not always zero if prices move intraday or across time zones.

Illustrative example (simplified):

- Gross RSUs vesting: 1,000 shares; FMV $50 → $50,000 wage income.

- Company sells 300 shares for withholding (round numbers) and delivers 700 shares to you.

- Your income and basis for the 700 long shares generally reflect the $50 per-share FMV included in wages (subject to your plan’s reporting and lot tracking).

- The 300 sold-for-tax shares may show a small gain/loss on Form 1099-B relative to the vest FMV.

This is not “taxing the same RSU dollars twice at ordinary rates.” It is wage taxation on the award plus separate gain/loss mechanics on shares actually sold.

Capital Gains Taxation at Sale

Establishing Cost Basis

The FMV at vesting becomes the cost basis for your RSUs. When you sell the shares, the gain or loss is calculated based on the difference between the sale price and this cost basis. This ensures that you are only taxed on the appreciation after vesting.

Example Calculation:

- Vesting FMV: $20/share

- Sale Price: $25/share

- Number of Shares Sold: 2,000

- Capital Gain: (2,000 shares × $25) - (2,000 shares × $20) = $10,000

Short-Term vs. Long-Term Capital Gains

The tax rate on your capital gains depends on how long you hold the shares after they vest:

- Short-Term Capital Gains: Held for less than 1 year, taxed at ordinary income rates.

- Long-Term Capital Gains: Held for more than 1 year, taxed at preferential rates of 0%, 15%, or 20%.

Table: Capital Gains Tax Rates

| Holding Period | Tax Rate |

|---|---|

| < 1 year | Ordinary rates |

| > 1 year | 0%, 15%, or 20% |

Critical Warning: Selling RSUs immediately after vesting can result in higher taxes due to short-term capital gains rates.

Adjusting Cost Basis on Form 1099-B

Brokers often report a $0 cost basis on Form 1099-B, which can lead to double taxation if not corrected. You must adjust the basis on Form 8949 to reflect the FMV at vesting.

Example Correction:

- Reported Basis on 1099-B: $0

- Correct Basis: $20/share

- Adjustment Needed: $20/share × 2,000 shares = $40,000

Table: Form 8949 Adjustment Codes

| Code | Description |

|---|---|

| B | Basis not reported to IRS |

| C | Corrected basis |

Supplemental Wage Withholding

Federal Withholding Rules

Supplemental wages, including RSU vesting value, are subject to federal income tax withholding at a default flat rate of 22% if paid separately from regular wages and totaling $1 million or less annually. Amounts over $1 million require 37% withholding on the excess.

Example Calculation:

- Vesting Income: $1,200,000

- Federal Withholding: 22% on $1,000,000 + 37% on $200,000

- Total Withholding: $220,000 + $74,000 = $294,000

Planning for Underwithholding

If your marginal tax rate exceeds the withholding rate, consider increasing your W-4 withholding or making quarterly estimated tax payments to avoid penalties.

Table: Withholding Adjustment Options

| Option | Description |

|---|---|

| Increase W-4 | Adjust withholding on regular wages |

| Estimated Payments | Make quarterly tax payments |

Important Note: The IRS requires that you pay at least 90% of your tax liability by the end of the year to avoid underpayment penalties.

Cost Basis Establishment at Vest

Importance of Correct Cost Basis

Establishing the correct cost basis at vesting is crucial to avoid double taxation. The FMV at vesting is used as the cost basis for future sales, ensuring that only post-vesting appreciation is taxed as capital gains.

Example Calculation:

- Vesting FMV: $50/share

- Number of Shares: 100

- Cost Basis: 100 shares × $50/share = $5,000

Adjustments for Corporate Actions

The cost basis may need to be adjusted for stock splits, dividends, and other corporate actions. Ensure that these adjustments are accurately reflected on your tax forms.

Table: Cost Basis Adjustments

| Action | Adjustment Needed |

|---|---|

| Stock Split | Adjust basis per share |

| Dividend Reinvestment | Add to cost basis |

Critical Warning: Failure to adjust for corporate actions can result in incorrect tax calculations and potential penalties.

Form 1099-B Reporting and Cost Basis Errors

Common Reporting Errors

Brokers often report incorrect cost basis on Form 1099-B, leading to potential double taxation. It's essential to verify and adjust the basis to match the FMV at vesting.

Example Correction:

- Incorrect Basis on 1099-B: $0

- Correct Basis: $5,000

- Adjustment Needed: Report on Form 8949 with Code B

Avoiding Double Taxation

To prevent double taxation, ensure that the cost basis reported on Form 8949 matches the FMV at vesting. This adjustment is crucial for accurate tax reporting.

Table: Form 8949 Reporting Codes

| Code | Description |

|---|---|

| A | Basis reported to IRS |

| B | Basis not reported to IRS |

| C | Corrected basis |

Important Note: Always retain documentation of the FMV at vesting and any adjustments made to the cost basis.

Frequently Asked Questions

What is the tax treatment of RSUs at vesting?

Answer: At vesting, RSUs are taxed as ordinary income based on their fair market value. This amount is reported on your W-2 and is subject to federal, state, and payroll taxes.

Source: IRS Publication 525

How do I calculate the cost basis for RSUs?

Answer: The cost basis for RSUs is the fair market value at the time of vesting. This amount is used to calculate capital gains or losses when the shares are sold.

Source: Morgan Stanley

What happens if my broker reports a $0 cost basis on Form 1099-B?

Answer: If your broker reports a $0 cost basis, you must adjust it on Form 8949 to reflect the FMV at vesting. This prevents double taxation on the sale of RSU shares.

Source: Schwab

Are RSUs subject to FICA taxes?

Answer: Yes, RSUs are subject to Social Security and Medicare taxes at vesting, up to the applicable wage base limits.

Source: IRS Publication 15

How can I avoid underpayment penalties on RSU income?

Answer: To avoid underpayment penalties, consider increasing your withholding or making estimated tax payments if your marginal tax rate exceeds the withholding rate.

Source: TurboTax

What are the long-term capital gains tax rates for RSUs?

Answer: Long-term capital gains on RSUs held for more than one year are taxed at preferential rates of 0%, 15%, or 20%, depending on your income level.

Source: IRS Publication 550

How do RSUs differ from stock options in terms of taxation?

Answer: RSUs are taxed at vesting as ordinary income, while stock options are taxed when exercised. The difference in FMV between the exercise price and the market price at exercise is taxed as ordinary income for non-qualified stock options (NSOs), while incentive stock options (ISOs) may have different tax implications.

Source: Fidelity

Can I defer taxes on RSUs?

Answer: Generally, taxes on RSUs cannot be deferred as they are taxed at vesting. However, some companies offer deferred compensation plans that allow employees to defer income until a later date, subject to specific rules and limitations.

Source: Investopedia

What are the implications of RSUs for non-resident aliens?

Answer: Non-resident aliens may be subject to different tax rules on RSUs, including potential withholding requirements and tax treaties that affect how RSUs are taxed. It's crucial to consult a tax advisor familiar with international tax law.

Source: IRS International Taxpayers

How do corporate actions affect RSU taxation?

Answer: Corporate actions such as mergers, acquisitions, or stock splits can affect the taxation of RSUs. These actions may alter the vesting schedule or the number of shares received, impacting the cost basis and potential capital gains.

Source: Charles Schwab

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRS Publication 525 | Guide | IRS |

| Morgan Stanley | Article | Morgan Stanley |

| Schwab | Guide | Schwab |

| IRS Publication 15 | Guide | IRS |

| TurboTax | Article | TurboTax |

| IRS Publication 550 | Guide | IRS |

| Fidelity | Article | Fidelity |

| Investopedia | Article | Investopedia |

| IRS International Taxpayers | Guide | IRS |

| Charles Schwab | Article | Charles Schwab |

Disclaimer: This guide is for general education only and is not individualized tax, legal, or investment advice. Tax rules change, and your facts (employer plan design, residency, treaty status, payroll reporting) may differ. Consult a qualified tax professional before making decisions.