Executive Summary

What is W-2 Box 14 for equity compensation?

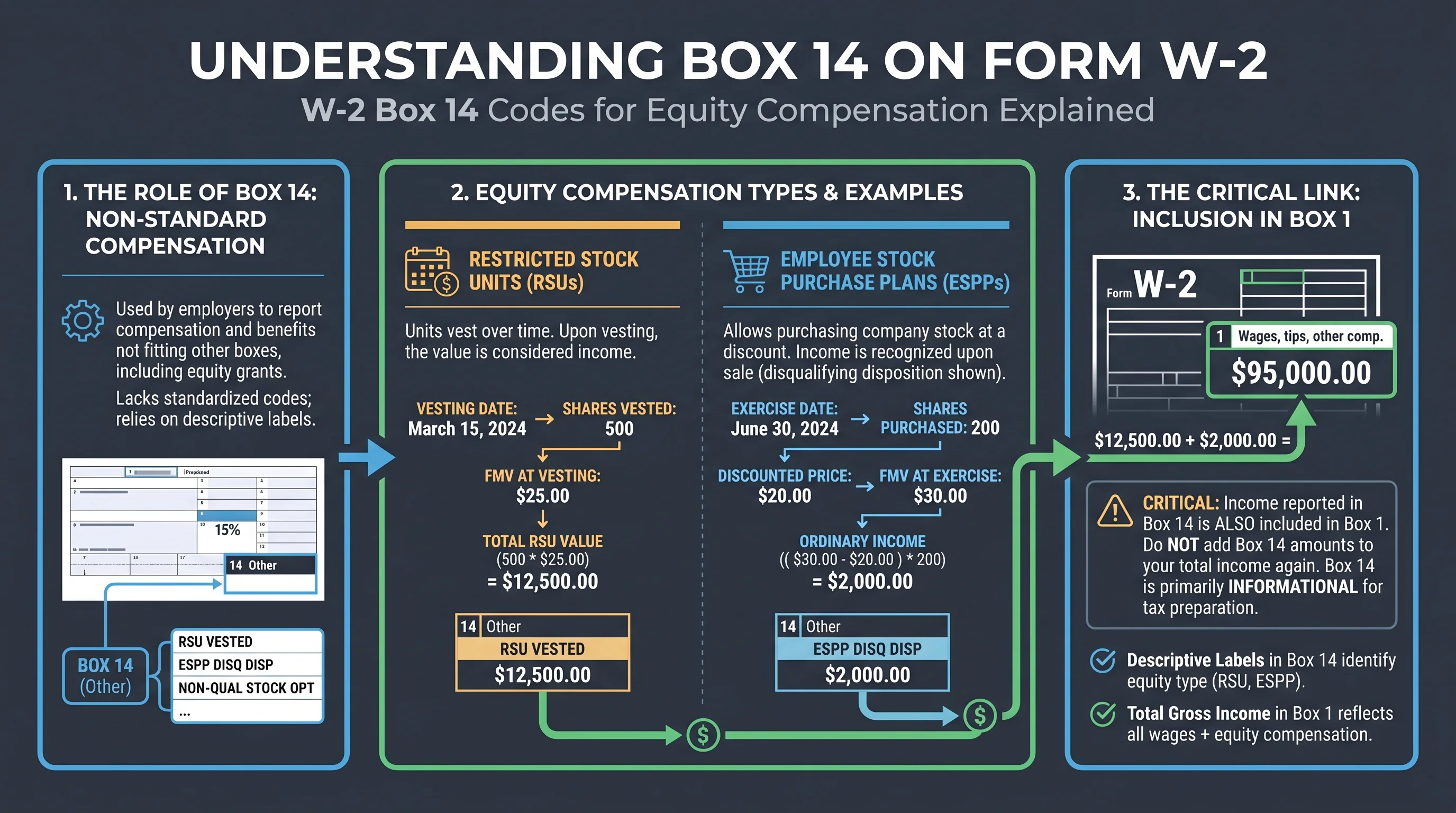

Box 14 is optional information your employer chooses to print—state disability contributions, union dues, educational assistance, or shorthand notes about equity. For many tech employees, equity wage income is already included in Box 1 wages; Box 14 may simply label a portion (for example “RSU”) for payroll or state purposes. Always read Box 14 together with Box 1, Box 12, state Boxes 15–20, and your brokerage tax forms.

The bottom line: Treat Box 14 as footnotes to payroll, not as a second wage total. Your tax return’s wage line generally follows Box 1, not Box 14 labels summed again.1

Critical warning: If you add Box 14 “RSU” amounts to Box 1 without checking whether they are already included in Box 1, you can double-report income. When in doubt, compare December pay stubs to the annual W-2.

Figure 1: Box 1 is the wage spine; Box 14 is often explanatory—not additive.

How Box 14 fits on the W-2

Official role (IRS framing)

Form W-2 is structured so Boxes 1–11 carry amounts the IRS and SSA use most directly. Box 12 carries coded items (including several equity-related codes). Box 14 is described in IRS instructions as space for employers to report other information—union dues, state disability insurance, after-tax retirement contributions, and similar items—using short descriptions chosen by the employer.

Because Box 14 is flexible, two employers can use different abbreviations for conceptually similar equity information.

Boxes 3–6: Social Security and Medicare vs. Box 14

Equity wages almost always flow through Medicare wages (Box 5) because the Additional Medicare Tax threshold logic keys off Medicare wages, not Box 14. Social Security wages (Box 3) may be capped at the annual wage base, while Box 1 can keep climbing with large RSU vests.

| Box | Common meaning | Equity pitfall |

|---|---|---|

| Box 1 | Federal taxable wages | Your starting point for ordinary income |

| Box 3 | Social Security wages | May stop increasing after the SS wage base |

| Box 5 | Medicare wages | Often tracks unlimited Medicare exposure |

| Box 6 | Medicare tax withheld | Compare to Additional Medicare rules at higher wages |

Box 14 does not replace this spine. If you try to infer FICA from Box 14 memos alone, you will usually guess wrong.

Equity items that usually do not belong in Box 14

Some equity tax events are defined elsewhere:

| Item | Typical W-2 location | Why Box 14 is the wrong focus |

|---|---|---|

| NSO exercise ordinary income | Box 1 + Box 12 Code V | Code V is the standardized equity wage tag |

| ISO disqualifying disposition | Box 1 + Box 12 Code V (often) | Character depends on facts; still wage-style for many payrolls |

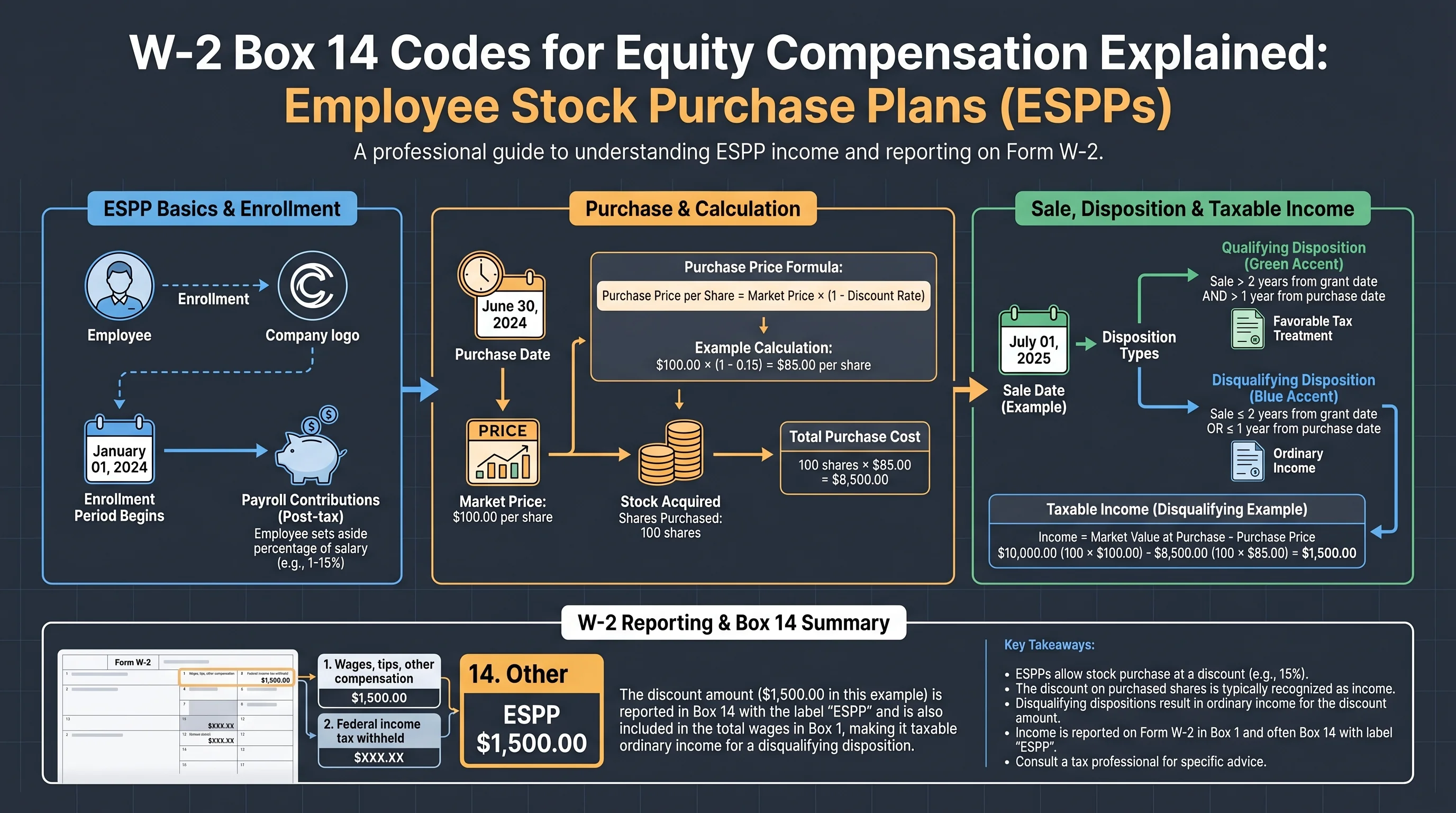

| ESPP disqualifying disposition | Box 1 + Box 12 Code V | Discount/spread may be wages |

| RSU vest (same-day settlement) | Box 1 wages | May appear again in Box 14 as a memo |

For the full reporting map, read Equity compensation reporting: Forms 3921, 3922, and W-2.

Figure 2: Box 12 Code V is the standardized wage marker for many option/ESPP spreads.

Common Box 14 labels tech employees see

The following labels are examples only—verify against your employer’s payroll guide.

| Label (examples) | What it might mean | What to do |

|---|---|---|

| RSU | Memo of RSU ordinary income included in wages | Confirm the same dollars in Box 1 / last paycheck |

| ESPP | Employer shorthand for ESPP-related wage items | Check Box 12 and your purchase confirmation |

| STOCK / EQ | Generic equity wage bucket | Read supporting footnotes on the W-2 PDF |

| NQ / NQSO | Nonqualified option wage component (informal) | Cross-check Code V and exercise statements |

| ISO | Sometimes informational (ISOs may not add to Box 1 at exercise) | ISO regular tax vs AMT is not “Box 14 solves it”—see ISO vs NSO |

| State programs (e.g., SDI, FLI) | State insurance/withholding | Usually not equity, but appears in Box 14 |

If your employer uses opaque tokens (e.g., internal project codes), ask HR payroll for the W-2 legend—that is faster than guessing.

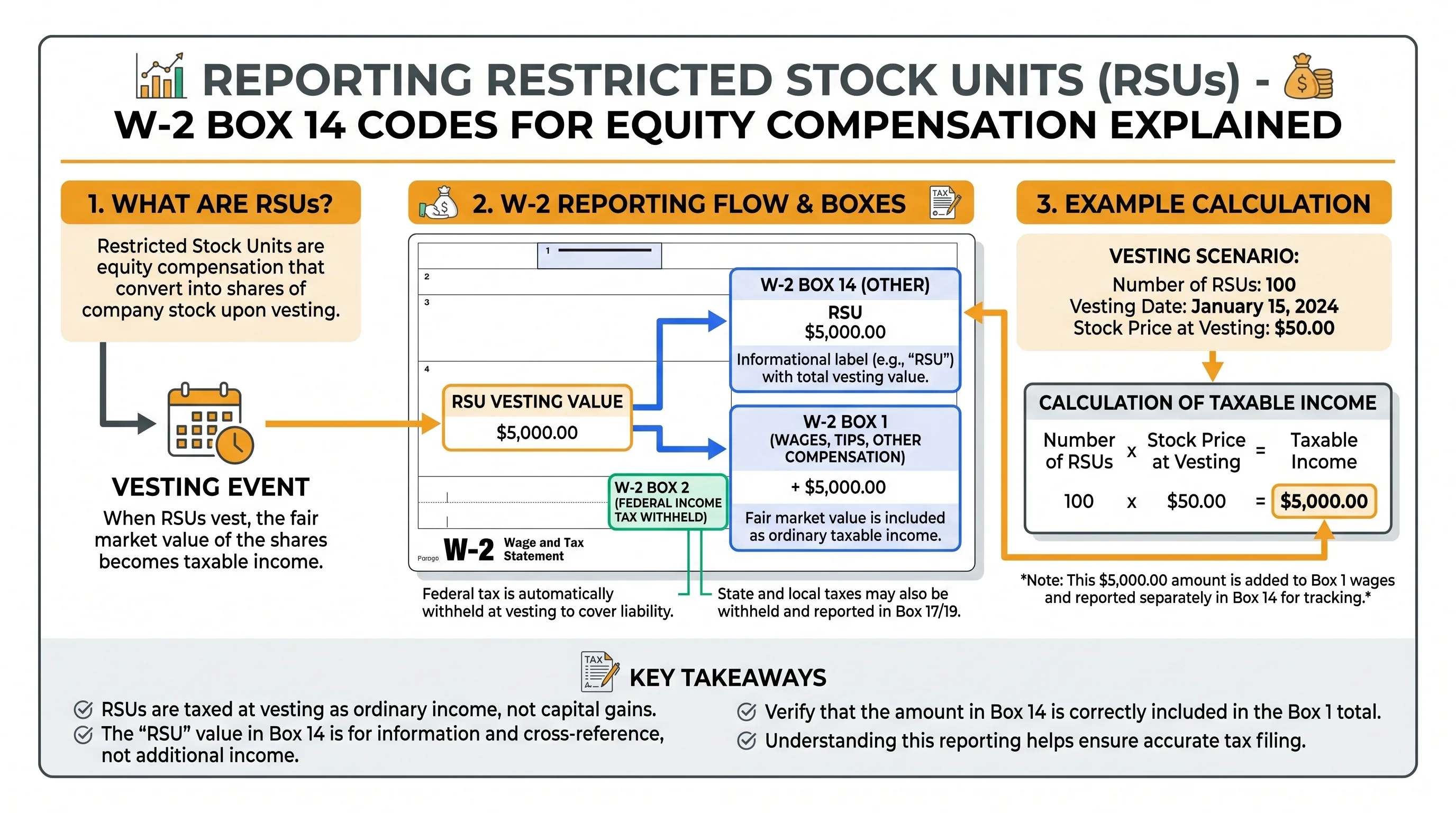

RSUs: Box 14 vs sell-to-cover

When RSUs vest, many employers withhold shares and report wages for the full vest FMV (before share withholding). Your net share deposit is smaller, but taxable wages can still reflect the gross spread.

Reconciliation habit:

- Find vest FMV × shares on your equity portal.

- Match to Box 1 wage jump on the vest date pay cycle.

- Use Box 14 only if it helps split components (some payrolls separate bonus vs RSU).

Deep dive: RSU sell-to-cover withholding explained.

Box 12 codes you must read alongside Box 14

Code V — exercise / ESPP wage spreads

Box 12 Code V is one of the most important equity codes because it ties payroll ordinary income to later stock sales.

Code Z — Section 409A failures

If amounts are treated as Section 409A includible under federal rules, employers may use Code Z (and additional reporting). This is not “ordinary RSU vesting”—it is a compliance failure category with different planning stakes.

Code W — HSA (not equity, but common neighbor)

Employees sometimes confuse Code W (employer HSA) with equity lines because both appear in Box 12. Keep HSA and equity workflows separate.

Figure 3: Payroll wages set basis; brokerage 1099-B tests your math at sale.

Worked example: avoid double-counting

Scenario: Box 1 shows $400,000 wages. Box 14 shows RSU $120,000.

Wrong move: Enter $520,000 wages because “Box 14 adds RSU.”

Right move: Confirm whether the $120,000 is already inside the $400,000 Box 1 total (almost always yes for standard payroll). Box 14 is then a memo, not an extra stack of wages.

Scenario 2 — broker sale: You sell vested shares the next year. Your 1099-B shows proceeds and may show cost basis that already reflects prior wage inclusion. Compare to Form 1099-B after stock compensation.

State and local hints in Box 14

Some employers push state-specific programs into Box 14:

- California SDI

- New Jersey UI/SDI family leave variants

- Local occupational taxes in certain cities

These lines can affect state return worksheets even when they do not change federal AGI. If you live in a high-tax state, pair this guide with state nexus and remote work.

W-4 and withholding: Box 14 does not replace planning

Box 14 does not tell you your marginal rate. If equity spikes your wages, adjust Form W-4 or make estimated payments:

Statutory vs non-statutory: why Box 14 will not answer ISO questions

Incentive stock options (ISOs) can produce no regular wage inclusion at exercise if you hold shares and meet ISO statutory tests—but you may still have AMT adjustments. That complexity rarely belongs in Box 14. Instead, watch Form 3921 (exercise information) and your holding period records.

Nonqualified stock options (NSOs) usually create ordinary wages at exercise equal to the spread, commonly mirrored in Box 12 Code V. Box 14 might say “NSO” or “OPTION,” but the coded wage amount is what ties to your basis.

If you exercised ISOs and are trying to predict AMT, start at AMT planning for stock options—not Box 14.

When Box 14 seems to “fight” your broker 1099-B

Brokers sometimes report cost basis that already reflects prior wage inclusion from the employer (RSU net settlement is a classic). Other times, basis is incomplete and you must adjust on Form 8949.

Red flags:

- Proceeds on 1099-B without a plausible cost basis for shares you acquired from vesting

- Duplicate wage income: you claim the RSU wage and treat the full sale as zero basis

- Wash sale markers on RSU-related sales (less common than option trading, but possible with frequent purchases)

Walk the reconciliation slowly: payroll wage sets your starting basis for shares you received as compensation; broker reports the exit. Our cost basis and equity compensation guide is the conceptual bridge.

Corrected W-2 (Form W-2c) and payroll reversals

M&A integrations, payroll vendor bugs, and late 409A adjustments occasionally force a Form W-2c. If you receive a correction:

- Compare Box 1 deltas first—did wages move materially?

- Re-check Box 12 codes; Code V corrections change basis logic for later sales.

- Update state returns if Boxes 15–17 shifted.

- If you already filed, consider amended returns under IRS and state rules.

Box 14 on a corrected W-2 can change labels even when Box 1 is unchanged—those edits still matter for state worksheets even if federal AGI is flat.

International employees: US W-2 Box 14 while non-US payroll runs “shadow” equity

Some multinationals pay home-country salary but run a US shadow payroll for equity tied to US services. Box 14 may include memo lines that exist only for US compliance while your payslip currency differs.

If that sounds like your situation, read Equity compensation for international employees and verify treaty residency with a cross-border CPA—Box 14 is still US payroll dialect, not a treaty answer.

Seasonal checklist (tie-out in January)

Use this during tax season alongside Tax season reporting for stock compensation:

| Step | Action |

|---|---|

| 1 | Export full-year pay stubs (all employers) |

| 2 | Match Box 1 to YTD “Medicare wages” / “Federal taxable wages” |

| 3 | List every Box 12 code and amount |

| 4 | Read Box 14 as memo, not automatic additions |

| 5 | Import 1099-B only after you understand basis |

Frequently Asked Questions

Is Box 14 income always taxable?

Answer: Not as a separate rule. Box 14 items may be informational, already included in Box 1, or relate to state programs. Read the label and confirm with pay stubs.

Source: IRS — Instructions for Forms W-2 and W-3

Why does my employer print “RSU” in Box 14 if it is already in Box 1?

Answer: Payroll systems often segment compensation for state reporting, GL accounting, or employee communication. The duplication is usually descriptive, not an extra IRS wage line.

Source: IRS — Instructions for Forms W-2 and W-3

Do I enter Box 14 on my Form 1040?

Answer: You generally start from Box 1 wages on your W-2 inputs. Some Box 14 items flow to state forms or worksheets. Follow your software’s interview carefully.

Source: IRS Publication 17

What is the difference between Box 12 Code V and Box 14 “NQSO”?

Answer: Code V is a standardized Box 12 code for the spread on option exercises and certain ESPP dispositions. Box 14 “NQSO” may be an employer nickname for communication. Trust coded Box 12 first, then reconcile.

Source: IRS — Instructions for Forms W-2 and W-3

Can Box 14 help me figure cost basis when I sell shares?

Answer: Sometimes it points to wage amounts, but basis lives in trade history and 1099-B adjustments. Use wage inclusion to reduce double tax risk, not as a substitute for broker downloads.

Source: IRS — Instructions for Form 8949

I have two W-2s after a merger—Box 14 differs. What now?

Answer: Treat each W-2 as a separate payroll system. Merge totals only after you confirm which lines are memo vs additive. M&A payroll cutovers are a common source of duplicate RSU confusion—see Spin-offs and carve-outs.

Source: Internal guide

Where can I learn more about ISO vs NSO W-2 patterns?

Answer: Start with ISO vs NSO and ISO qualifying vs disqualifying disposition.

Source: Internal guides

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRS — Forms W-2 and W-3 instructions | Federal | irs.gov/instructions/iw2w3 |

| IRS — Publication 525 | Federal | irs.gov/publications/p525 |

| IRS — Topic 427 | Federal | irs.gov/taxtopics/tc427 |

| IRS — Publication 17 | Federal | irs.gov/publications/p17 |

| IRS — Form 8949 instructions | Federal | irs.gov/instructions/i8949 |

Disclaimer: This guide discusses legal tax compliance and literacy only. Tax evasion is illegal. This is not individualized tax advice. Consult a qualified professional for your facts.

Footnotes

-

IRS wage reporting framework: Instructions for Forms W-2 and W-3 and equity overview Publication 525. ↩