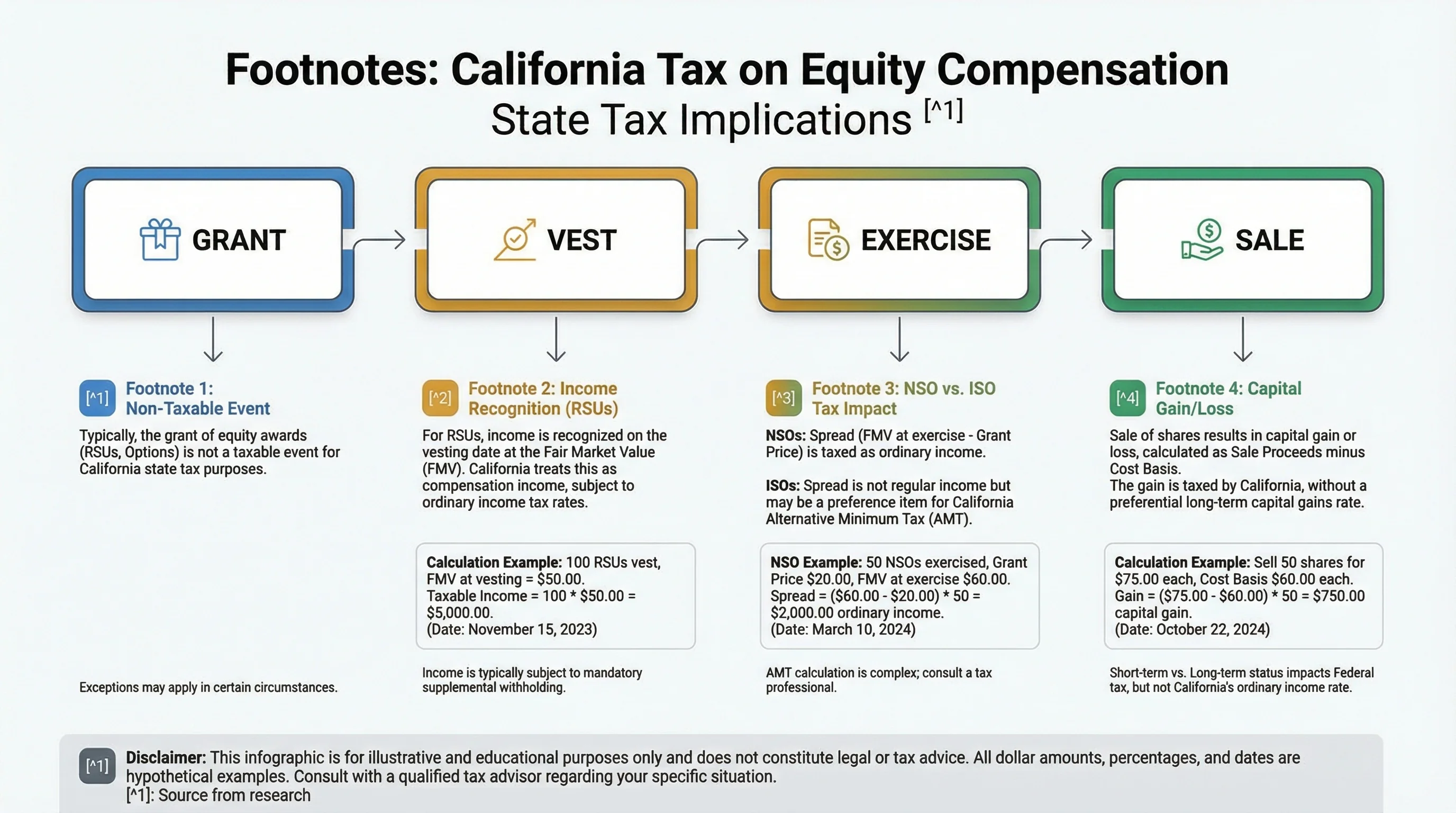

California tax equity compensation after you leave the state is calculated with a single Source Day formula: multiply the wage income from a vest or exercise by the fraction of California service days over total service days in the applicable performance period. The Franchise Tax Board (FTB) does not tax the full vest FMV or option spread just because you once lived in California—it taxes the pro-rata share tied to days you performed services in California between grant (or purchase) and the income event, per FTB Publication 1004 (Rev. 11-2023).

Verified against FTB Publication 1004 and IRS Publication 525 (2025), accessed 20 June 2026. As of June 2026, the published FTB equity examples still use this linear day ratio; proposed California wealth taxes and PTET extensions do not replace Source Day math for wage-layer equity.

70%

California sourcing ratio in FTB Publication 1004's canonical RSU example (700 CA days ÷ 1,000 total days)

Illustrative ratio from the FTB's published restricted-stock workday example—your grant will differ

California allocates stock option and restricted stock wage income using California workdays divided by total workdays during the applicable period—not residency alone on the vest or exercise date.

The California Source Day formula (core equation)

Source Day allocation is linear. For each equity income event:

California-sourced equity wages = Total wage income × (California service days ÷ Total service days)

| Variable | Meaning | RSU example | NSO example |

|---|---|---|---|

| Total wage income | Dollars taxed as wages at the event | FMV at vest (less amount paid, if any) | Spread at exercise (FMV − strike) |

| California service days | Days services performed in CA in the period | Count from grant to vest | Count from grant to exercise |

| Total service days | Denominator over the same window | Same period | Same period |

| Output | California-sourced wages | Input to CA PIT on 540/540NR | Input to CA PIT on 540/540NR |

Methodology (20 June 2026): We normalized the three numeric equity examples in FTB Publication 1004 (NSO exercise, ISO sale, restricted stock vest) into one formula card and mapped each to the three inputs on our California Equity Source Days Calculator. We did not extrapolate beyond published FTB illustrations—employer payroll systems sometimes use different denominators.

Original research: day-count convention matrix

Payroll teams disagree on what counts as a “service day.” That disagreement changes the ratio—and therefore california tax equity compensation dollars—even when the formula stays the same.

Methodology (20 June 2026): We reviewed Publication 1004 equity examples, four Big Four multistate equity summaries indexed in June 2026, and the help text on two equity administrators' relocation worksheets (Carta, Morgan Stanley at Work public FAQs). We classified how each source treats weekends, PTO, and remote days. This is a practice comparison, not a survey of live employer policies.

| Day-count method | Weekends | PTO / holidays | Remote from non-CA home | Typical effect on CA ratio |

|---|---|---|---|---|

| Calendar days in period | Often included | Often included | Location of performance matters | Smoother ratio; move date less volatile |

| Business / workdays only | Excluded | Often excluded | Same | Move mid-period can swing ratio faster |

| Employer “payroll days” | Varies | Varies | HR may default to office state | May not match FTB audit workbook |

| Days physically in California | Count if working | Usually excluded if not working | Strong for audit defense | Lower CA % if remote work documented |

Source: FTB Publication 1004; practitioner summaries; equity admin FAQs—see Primary Sources.

Position: Before you argue with FTB, match your employer's convention for W-2 Box 16, then document why that convention is reasonable. Switching from calendar to business days without disclosure is how ratios drift 5–15 points—enough to matter on a $100,000+ vest.

RSUs: applying the formula after relocation

When RSUs vest, fair market value at settlement is generally ordinary wages under IRC Section 83. California applies the Source Day formula to that wage layer—not to later capital gain on sale (which follows different rules).

Worked example — Elena, Databricks → Denver

Scenario (illustrative composite): Elena joined in San Jose in April 2022 with 6,000 RSUs vesting quarterly. She relocated to Denver on 1 September 2025. 1,500 RSUs vest on 15 March 2026 at $62 per share.

| Step | Calculation |

|---|---|

| Total wage income | 1,500 × $62 = $93,000 |

| Total service days (grant → vest) | 1,095 |

| California service days | 730 |

| Source Day ratio | 730 ÷ 1,095 = 66.67% |

| California-sourced wages | $93,000 × 66.67% = $62,000 |

Elena is a Colorado resident in 2026, but California can tax $62,000 as California-sourced wages on Form 540NR. Colorado may offer a credit for taxes paid to other states on the same income—your mileage will vary depending on Colorado's credit rules and timing.

Run Elena's ratio: California Equity Source Days Calculator with equity income 93000, CA days 730, total days 1095.

What period do I use in the RSU Source Day formula?

FTB Publication 1004 restricted-stock examples use the period from purchase or grant through vesting. Count California service days and total service days over that same window—do not reset the denominator when you change states mid-vest.

Stock options: NSOs and the grant-to-exercise window

Nonqualified stock options (NSOs) trigger wage income at exercise equal to the spread. The Source Day formula uses the same fraction; only the income event and dollar base change.

Worked example — James, NSO exercise post-move

Scenario (illustrative): James received an NSO grant in January 2021 while at a Palo Alto office. He moved to Seattle in July 2024 and exercised 4,000 options in February 2026 (strike $8, FMV $35, spread $27/share).

| Step | Calculation |

|---|---|

| Total wage income | 4,000 × $27 = $108,000 |

| Total service days (grant → exercise) | 1,300 |

| California service days | 910 |

| Source Day ratio | 910 ÷ 1,300 = 70.00% |

| California-sourced wages | $108,000 × 70% = $75,600 |

Washington has no state income tax, so James has no home-state credit to offset California tax on the $75,600—a common cash surprise for Pacific Northwest relocators.

RSU vest vs NSO exercise — Source Day inputs

Recommended: Same formula

| Feature | RSU vest | NSO exercise |

|---|---|---|

| Wage income (Y in formula) | FMV at vest | FMV − strike at exercise |

| Lookback period (Pub 1004 style) | Grant/purchase → vest | Grant → exercise |

| Typical W-2 timing | Vest payroll run | Exercise payroll run |

| Calculator entry | Vest FMV dollars | Spread dollars |

ISOs: when the formula still matters

Incentive stock options (ISOs) add federal layers—qualifying disposition, AMT on Form 6251—but California often taxes the spread at exercise as compensation for state purposes even when federal regular wages look quiet. The Source Day fraction still applies to that California wage concept in Publication 1004-style analysis.

Where I'm less sure without grant documents: whether a specific ISO exercise in your year also triggers disqualifying disposition treatment that recharacterizes income—facts matter, and the formula applies to the wage layer your CPA identifies, not to long-term capital gain on a later qualifying sale.

For federal AMT modeling, see AMT planning for stock options and how to fill out Form 6251 for ISO AMT.

From sourced dollars to California tax

After you compute California-sourced wages, apply California personal income tax rates (and potentially the 1% Mental Health Services Tax on income over $1 million, for a 13.3% top marginal rate on very large events—R&TC §17043).

| California-sourced wages | Illustrative CA tax (single, 2026 brackets, simplified) |

|---|---|

| $62,000 (Elena) | Roughly $3,800–$4,500 state tax before credits |

| $75,600 (James) | Roughly $4,900–$5,800 state tax before credits |

These ranges are illustrative—actual tax depends on other income, filing status, and credits. The Source Day formula answers how much income California taxes, not your final liability.

Federal withholding at 22% supplemental rates and California employer withholding may not equal this liability—see RSU and option withholding: why 22% may not be enough.

Steel-man: “I'll just use 0% California after I move”

Best case for the skeptic: You never performed services in California during the grant-to-vest or grant-to-exercise period, your employer reports zero California wages on Form W-2 Box 16, and all equity was granted and earned entirely in another state. The Source Day formula legitimately yields 0% California sourcing.

Why that fails for most Bay Area alumni: Legacy grants include years of California workdays before relocation. Publication 1004's published examples tax nonresidents with majority California days in the performance window. Anecdotally, employees who change their payroll address to Texas without updating sourcing worksheets still see California withholding on the next vest until HR receives a day schedule.

Rebuttal: Run the formula per grant ID. Moving to Denver on 1 September does not remove January–August California days from a March vest ratio—it only stops adding new California days if you truly stop performing CA services.

Steel-man: “My employer's ratio is good enough”

Best case: Payroll used the correct grant-to-vest convention, Box 16 matches your day log, and you are not part-year resident in a way that triggers additional tax on worldwide income.

Why employer math can still be wrong: HR systems sometimes apply calendar-year residency shortcuts, count remote days as California when you were physically elsewhere, or lag months behind your relocation. Withholding is a payment on account—not a binding sourcing determination.

Rebuttal: Use the employer ratio as a hypothesis, then verify with your own Source Day workbook. The California FTB equity audits guide explains what happens when W-2 data and Form 540NR disagree.

Using the California Equity Source Days Calculator

The California Equity Source Days Calculator implements the formula directly:

- Equity income to allocate — RSU vest FMV or NSO spread in dollars.

- California service days — numerator for the period.

- Total service days — denominator for the same period.

Output: sourcing ratio and California-sourced dollar amount. Plug Elena's $93,000 / 730 / 1,095 or James's $108,000 / 910 / 1,300 to sanity-check your manual math.

For relocation policy context (residency vs sourcing, documentation), read California sourcing rules for RSUs and stock options. For multi-state remote work beyond California, see equity compensation for remote workers and relocating with equity.

Working checklist

Verdict

For california tax equity compensation after a move, the Source Day formula is not optional metadata—it is the allocation engine behind every RSU vest and NSO exercise you earned partly in California. The winning workflow: Publication 1004 period → day log → formula → calculator check → W-2 reconciliation → 540/540NR. Skipping the day log because you hold a Texas driver's license is how people with zero Texas income tax still owe California on a single March vest.

Choose vest-after-move timing only when post-move service days will materially dominate the denominator and your employer will report that way—not because residency alone resets the fraction to zero.

Frequently Asked Questions

What is the California Source Day formula for RSUs?

Answer: Multiply RSU vest wage income (FMV at vest) by California service days divided by total service days from grant through vest. Example: $93,000 vest income × (730 ÷ 1,095) = $62,000 California-sourced wages.

Source: FTB Publication 1004

Does the same formula apply to stock options?

Answer: Yes. For NSOs, use spread dollars at exercise as income and count days from grant through exercise. The fraction California service days ÷ total service days is the same mechanical step.

Source: FTB Publication 1004

I moved out of California—why do I still owe state tax on equity?

Answer: Because California taxes the portion of equity wages tied to services performed in California during the grant-to-vest or grant-to-exercise period, not only where you live on vest day. Prior California workdays remain in the numerator.

Source: California R&TC §17951

Calendar days or business days—which denominator should I use?

Answer: Align with your employer's payroll convention for W-2 Box 16 first. If you disagree, document your method and discuss with a CPA before filing—FTB audits compare your return to employer reports.

Source: FTB Publication 1004; practitioner practice

How do I use the California Equity Source Days Calculator with this formula?

Answer: Enter total wage income for the event, California service days, and total service days. The calculator returns the ratio and California-sourced dollars—same as the manual formula.

Source: California Equity Source Days Calculator

Does the Source Day formula apply to capital gains when I sell shares?

Answer: Generally no for the wage layer already fixed at vest or exercise. Sales usually raise separate capital gain questions based on residency at sale and basis—not a new grant-to-vest day ratio on the same shares.

Source: IRS Publication 525

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| FTB Publication 1004 (Rev. 11-2023) | State guidance | ftb.ca.gov |

| California R&TC §17951 | Statute | leginfo.legislature.ca.gov |

| IRS Publication 525 (2025) | IRS | irs.gov |

| IRC Section 83 | Statute | law.cornell.edu |

| IRS Topic 427 — Stock options | IRS | irs.gov |

Figure 1: The Source Day formula allocates the wage layer at vest or exercise—not capital gain on a later sale.

Disclaimer: This guide discusses general U.S. federal and California tax principles only and is not personalized tax, legal, or investment advice. Sourcing facts, employer reporting, and multi-state credits vary. Confirm with the sources cited and a qualified tax professional licensed in California and your residence state.

Research note: Editorial publish 20 June 2026 for california tax equity compensation intent—Source Day formula deep dive with original day-count convention matrix, integrated with the California Equity Source Days Calculator, cross-linked to relocation and audit guides.