Executive Summary

What is an 83(b) election?

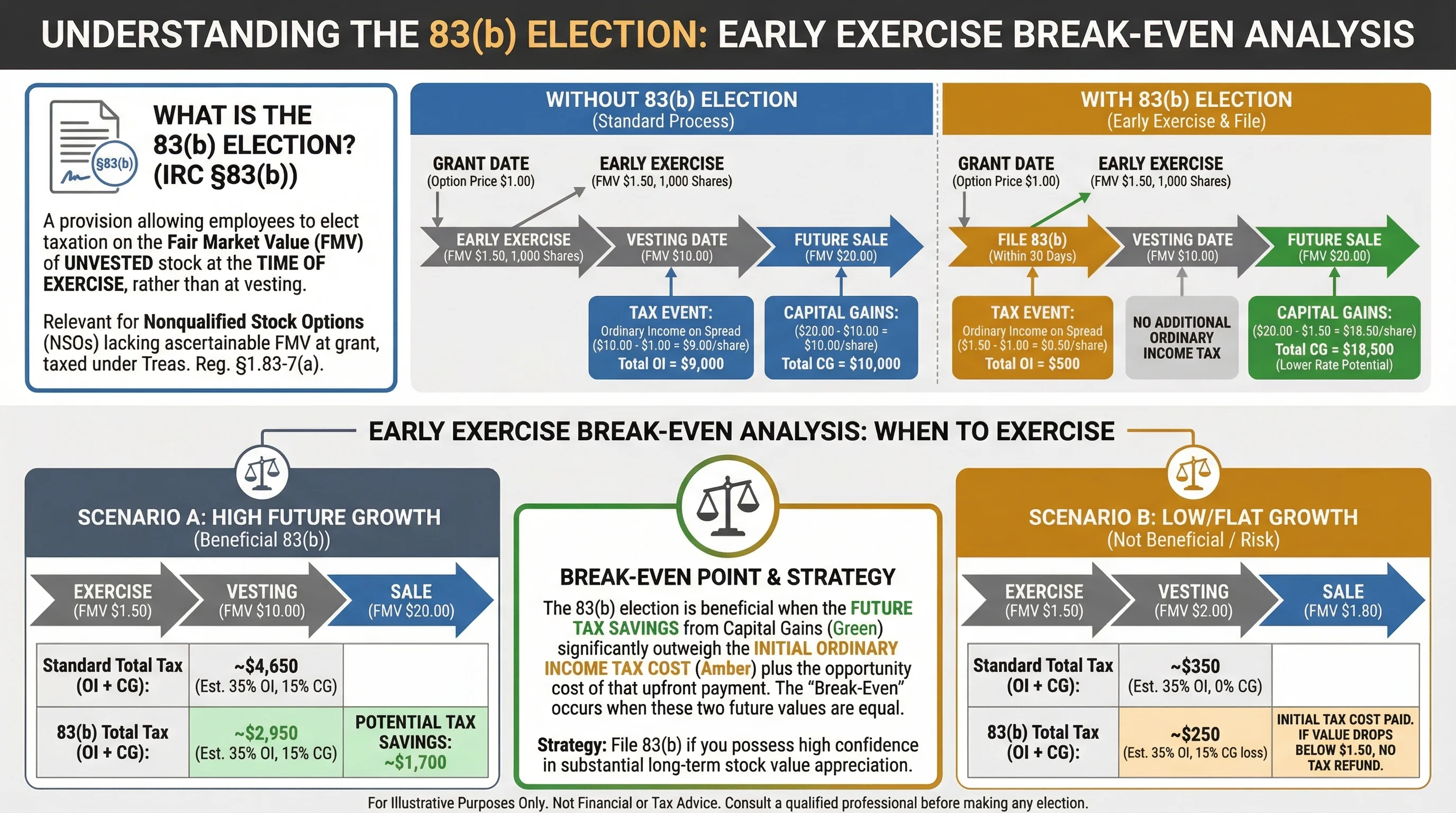

An 83(b) election allows employees to recognize ordinary income on unvested restricted stock from early exercise of nonqualified stock options (NSOs) at exercise-date fair market value (FMV), potentially converting future appreciation to capital gains.

The 83(b) election is a strategic tax decision that can significantly impact the financial outcomes for employees who receive nonqualified stock options (NSOs). By opting to pay taxes on the fair market value of the stock at the time of exercise rather than at vesting, employees can potentially convert future gains into capital gains, which are taxed at a lower rate. This election is particularly beneficial when the stock is expected to appreciate significantly before vesting. However, the decision to file an 83(b) election must be made within a strict 30-day window following the exercise of the options, and it is irrevocable. Understanding the mechanics, benefits, and risks of the 83(b) election is crucial for employees looking to optimize their tax liabilities.

The bottom line: The 83(b) election can offer substantial tax savings by converting future stock appreciation into capital gains, but it requires careful consideration and timely action1.

Critical Warning: Failing to file the 83(b) election within the 30-day window renders the election invalid, potentially resulting in higher tax liabilities2.

Understanding the 83(b) Election

What is the 83(b) Election?

The 83(b) election is a provision under the Internal Revenue Code (IRC) §83(b) that allows employees to elect to be taxed on the fair market value (FMV) of unvested stock at the time of exercise rather than at vesting. This election is particularly relevant for nonqualified stock options (NSOs) that lack a readily ascertainable FMV at the time of grant, triggering taxation at exercise under Treasury Regulation §1.83-7(a).

How Does the 83(b) Election Work?

When an employee exercises NSOs, they typically acquire shares that are subject to a vesting schedule. Without an 83(b) election, the employee would be taxed on the spread—the difference between the FMV at vesting and the exercise price—as ordinary income. By filing an 83(b) election, the employee elects to include the spread as ordinary income in the year of exercise, potentially converting future appreciation into capital gains.

Key Mechanics

- Election Effect: The taxpayer includes the excess of FMV over the amount paid (the "spread") as ordinary income in the transfer year. No further income is recognized at vesting unless the substantial risk of forfeiture lapses. Post-election gain or loss on sale is treated as capital.

- Filing Process: The election must be filed with the IRS within 30 days of the transfer (exercise date). The statement must include the taxpayer's name, address, Social Security Number, property description, transfer date, FMV, amount paid, and the election to apply §83(b), along with the taxpayer's signature.

- Deadlines & Limitations: The 30-day window is strict, and late filings are invalid. The election applies only to substantially nonvested property and is irrevocable.

Example Calculation

Consider an employee who early exercises 1,000 NSOs at a $5 strike price when the FMV is $10 per share. The spread is calculated as follows:

Spread = (1,000 shares × $10 FMV) - (1,000 shares × $5 strike price) = $5,000

This $5,000 is recognized as ordinary income in the year of exercise. Assuming a 37% tax bracket, the tax liability would be approximately $1,850. If the FMV at vesting is $50, no additional income is recognized. If the shares are sold at $60 after a one-year holding period, the $50,000 gain is treated as a long-term capital gain.

| Scenario | Tax at Exercise (83(b)) | Tax at Vesting (No Election) | Savings % (Assume 37% Ordinary, 20% LTCG) |

|---|---|---|---|

| FMV Vest = $50 | $5k ordinary (~$1.9k tax) | $40k ordinary (~$14.8k tax) | 87% |

| Sell Post-1Yr = $60 | $50k LTCG (~$10k tax) | N/A (already taxed vesting) | N/A |

Important Note: The 83(b) election is beneficial when the projected FMV growth exceeds the after-tax cost of the spread3.

Filing the 83(b) Election

Filing Process and Requirements

The 83(b) election must be filed with the IRS within 30 days of the stock transfer. The filing process involves submitting a written statement to the IRS Service Center where the taxpayer files their returns. The statement must include:

- Taxpayer's name, address, and Social Security Number

- Description of the property

- Date of transfer

- Fair market value of the property

- Amount paid for the property

- Statement of election to apply §83(b)

- Taxpayer's signature

Deadlines and Limitations

The 30-day filing window is strict, and no extensions are granted. If the election is not filed within this period, it is invalid. The election applies only to substantially nonvested property, meaning the property is subject to a substantial risk of forfeiture, such as a vesting schedule.

Example of Filing

An employee exercises 100 unvested shares at $10 per share when the FMV is $20 per share. The spread is $10 per share, totaling $1,000. By filing an 83(b) election, the employee elects to include this $1,000 as ordinary income in the year of exercise. The tax basis is set at the FMV, and no additional income is recognized at vesting.

Critical Warning: The 83(b) election is irrevocable once filed. Consider the potential risks and benefits carefully before making the election4.

Common Mistakes and Pitfalls to Avoid

- Missing the 30-Day Deadline: The election must be postmarked within 30 days of the exercise date. Late filings are not accepted.

- Incorrect or Incomplete Information: Ensure all required information is included in the election statement to avoid invalidation.

- Failure to Consider Future Stock Performance: Evaluate the likelihood of stock appreciation to determine if the election is beneficial.

Benefits and Risks of the 83(b) Election

Potential Benefits

- Tax Savings: By recognizing income at exercise, future appreciation is taxed at the lower capital gains rate rather than as ordinary income.

- Locking in Lower Tax Rates: If the stock appreciates significantly, the tax savings can be substantial.

Risks and Considerations

- Forfeiture Risk: If the employee leaves the company before vesting, they may forfeit the stock, resulting in a loss of the taxes paid.

- Stock Depreciation: If the stock value decreases, the employee may pay more in taxes than necessary.

Real-World Scenarios

Consider an employee who exercises NSOs when the FMV is low, anticipating significant growth. By filing an 83(b) election, they lock in a lower tax rate on future gains. However, if the stock value declines or the employee leaves the company, they may face financial losses.

Key Takeaways

- Evaluate Stock Potential: Consider the company's growth prospects and stock performance before making the election.

- Understand the Risks: Be aware of the potential for stock forfeiture and depreciation.

Comparing 83(b) Election with No Election

Tax Implications

The primary difference between filing an 83(b) election and not filing lies in the timing and type of income recognized. With an 83(b) election, the spread is recognized as ordinary income at exercise, and future gains are capital gains. Without the election, the spread is recognized as ordinary income at vesting.

Example Comparison

| Scenario | With 83(b) Election | Without 83(b) Election |

|---|---|---|

| Exercise Year | $5,000 ordinary income | $0 income |

| Vesting Year | $0 income | $40,000 ordinary income |

| Sale Year | $50,000 LTCG | N/A |

Best Practices

- Consult a Tax Advisor: Given the complexity and potential financial impact, consulting a tax advisor is recommended.

- Plan for Future Scenarios: Consider potential changes in employment status and stock performance.

Important Note: The decision to file an 83(b) election should be based on a thorough analysis of the potential tax savings and risks5.

Frequently Asked Questions

What is the deadline for filing an 83(b) election?

Answer: The 83(b) election must be filed within 30 days of the stock transfer (exercise date). This deadline is strict, and late filings are not accepted.

Source: Treas. Reg. §1.83-2(b)

Can the 83(b) election be revoked once filed?

Answer: No, the 83(b) election is irrevocable once filed. It is important to carefully consider the decision before filing.

Source: Rev. Proc. 2012-29

What happens if the stock value decreases after filing an 83(b) election?

Answer: If the stock value decreases, the employee may end up paying more in taxes than necessary, as the election locks in the tax basis at the FMV at exercise.

Source: Treas. Reg. §1.83-2

Are there any exceptions to the 83(b) election rules?

Answer: The 83(b) election applies only to substantially nonvested property. It does not apply to stock options with a readily ascertainable FMV at grant.

Source: IRC §83(e)(3)

How does the 83(b) election affect capital gains tax?

Answer: By filing an 83(b) election, future appreciation of the stock is taxed as a capital gain rather than ordinary income, potentially resulting in lower tax rates.

Source: Treas. Reg. §1.83-7

What are the tax implications of not filing an 83(b) election?

Answer: Without an 83(b) election, the spread is taxed as ordinary income at vesting, which may result in higher taxes if the stock appreciates significantly.

Source: Treas. Reg. §1.83-2

Can an 83(b) election be filed for incentive stock options (ISOs)?

Answer: No, the 83(b) election does not apply to incentive stock options (ISOs), which are governed by different tax rules.

Source: IRC §83(e)(3)

What documentation is required for an 83(b) election?

Answer: The election statement must include the taxpayer's name, address, Social Security Number, property description, transfer date, FMV, amount paid, and the election to apply §83(b), along with the taxpayer's signature.

Source: Treas. Reg. §1.83-2(b)

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| Treasury Regulation §1.83-2 | Regulation | Link |

| IRC §83 | Statute | Link |

| Rev. Proc. 2012-29 | Revenue Procedure | Link |

| Treasury Regulation §1.83-7 | Regulation | Link |

This comprehensive guide provides an in-depth understanding of the 83(b) election, its benefits, risks, and filing requirements. By carefully considering the potential tax implications and consulting with a tax advisor, employees can make informed decisions to optimize their tax liabilities.

For more detailed guides on related topics, check out our articles on Section 83(b) Election: A Strategic Tax Decision, ISO vs NSO Guide, Early Exercise Strategies, and AMT Planning for Stock Options. Use our Early Exercise Break-Even Calculator to model your specific scenario.

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Tax laws vary by jurisdiction and change frequently. Always consult a qualified tax professional (CPA, tax attorney, enrolled agent) before making decisions based on this information. The authors accept no liability for actions taken based on this content.

Footnotes

-

IRC §83(b) provides the framework for the 83(b) election, allowing employees to recognize income at exercise. ↩

-

The 30-day filing deadline is strict, and late filings are not accepted, as per Treasury Regulation §1.83-2. ↩

-

The 83(b) election is beneficial when the projected FMV growth exceeds the after-tax cost of the spread. ↩

-

The election is irrevocable once filed, requiring careful consideration of potential risks and benefits. ↩

-

Consulting a tax advisor is recommended to evaluate the potential tax savings and risks associated with the 83(b) election. ↩