Executive Summary

What percent should I contribute to ESPP?

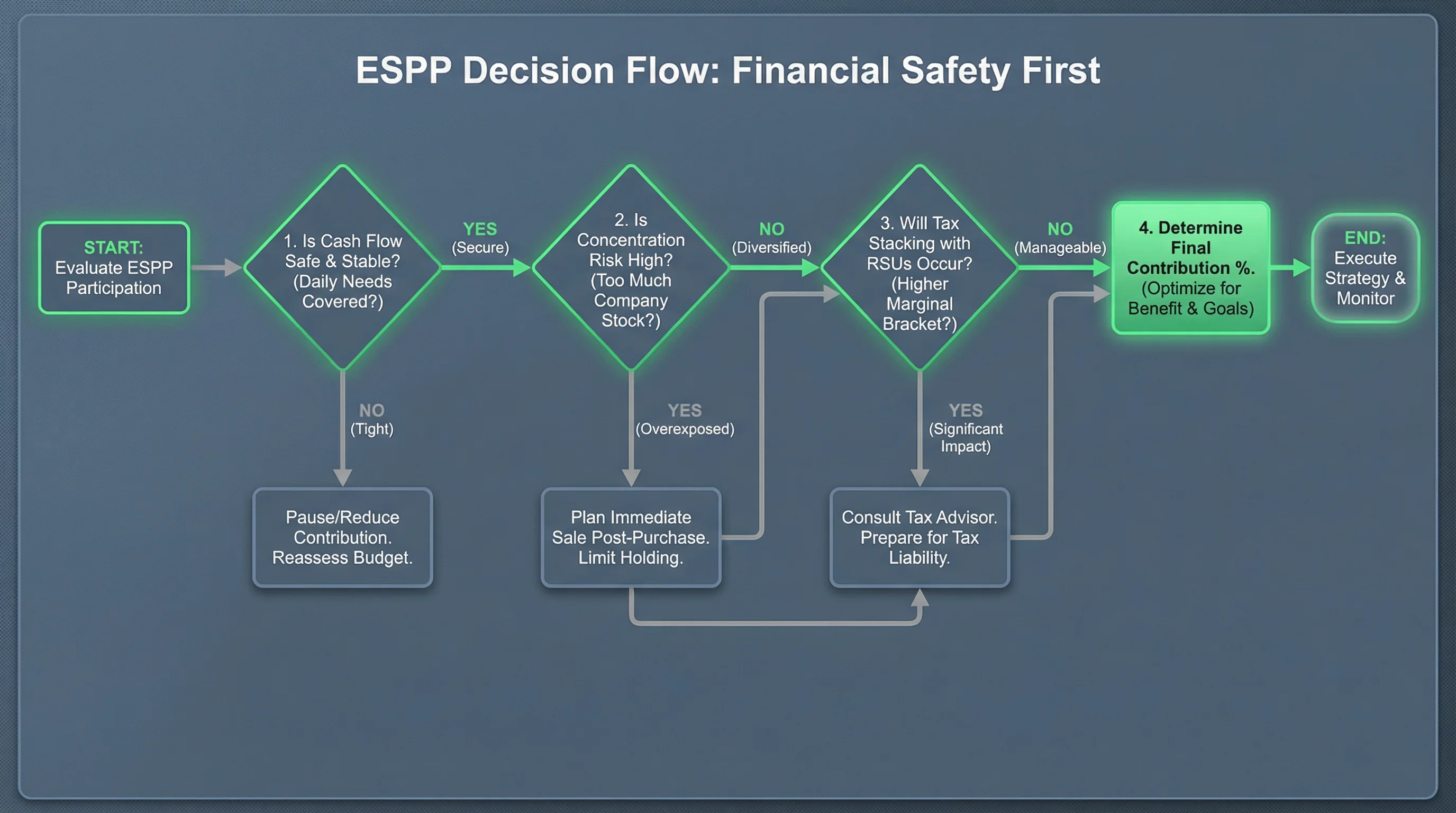

Start from cash-flow safety: set aside taxes on RSU/NSO income, emergency fund, and 401(k) goals—then allocate what remains to ESPP up to plan limits. Higher contributions increase concentration in employer stock.

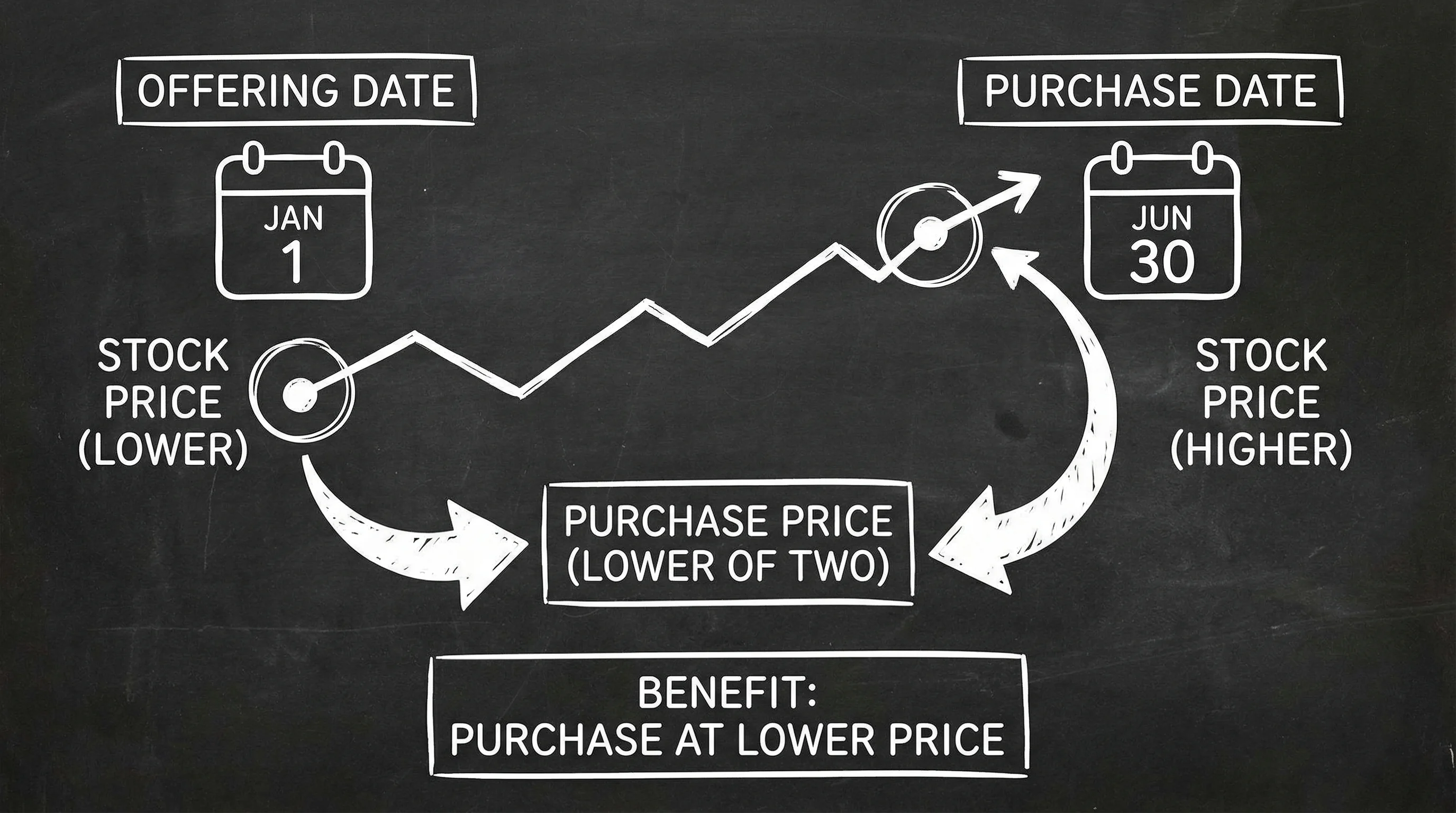

Why does lookback matter?

Many plans let you purchase at a discount from the lower of start/end price—if the stock rises, economic return can exceed the headline discount percentage.

Which tools help?

Use the ESPP total return calculator, $25k limit tool, qualifying disposition tool, and basis adjustment calculator on this site.

Figure 1: Order of operations before maxing contributions.

Decision Framework

| Factor | Question |

|---|---|

| Liquidity | Can you fund living costs if ESPP locks payroll cash? |

| Concentration | How much employer stock do you already hold? |

| Tax stacking | Will vesting events create underpayment risk? |

Figure 2: Why lookback can amplify economics when the stock rises—confirm your plan text.

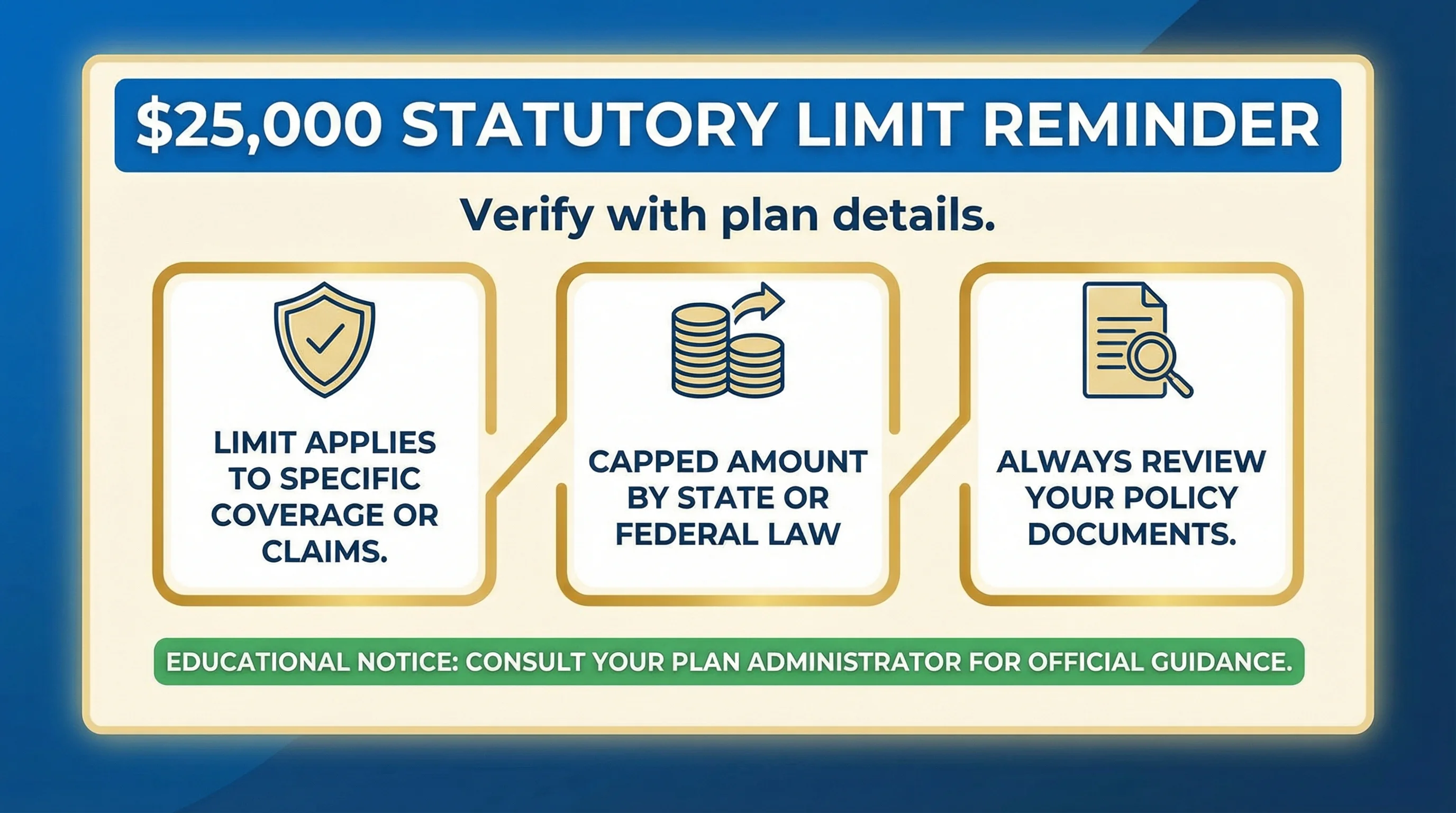

Figure 3: Statutory limit awareness—your administrator enforces mechanics.

Links

Disclaimer

Educational—not personalized advice.

Primary sources

| Source | URL |

|---|---|

| IRS publications hub | https://www.irs.gov/ |