Executive Summary

Quick Answer

Is double trigger the same for IPO and M&A?

Not necessarily—your plan defines the corporate event and the employment event. An IPO may be included or excluded depending on drafting; M&A definitions often reference mergers or asset sales.

Source: Plan document

Quick Answer

Why do RSU taxes differ between IPO and M&A?

Tax timing follows settlement and plan terms: RSUs are generally ordinary income when shares deliver. Acceleration can bunch income into a high-tax year—model withholding.

Source: IRC Section 83 basics

Quick Answer

Where should I start reading?

Our vesting acceleration guide explains single vs double trigger mechanics; pair with the M&A equity guide for transaction types.

Source: Internal guides

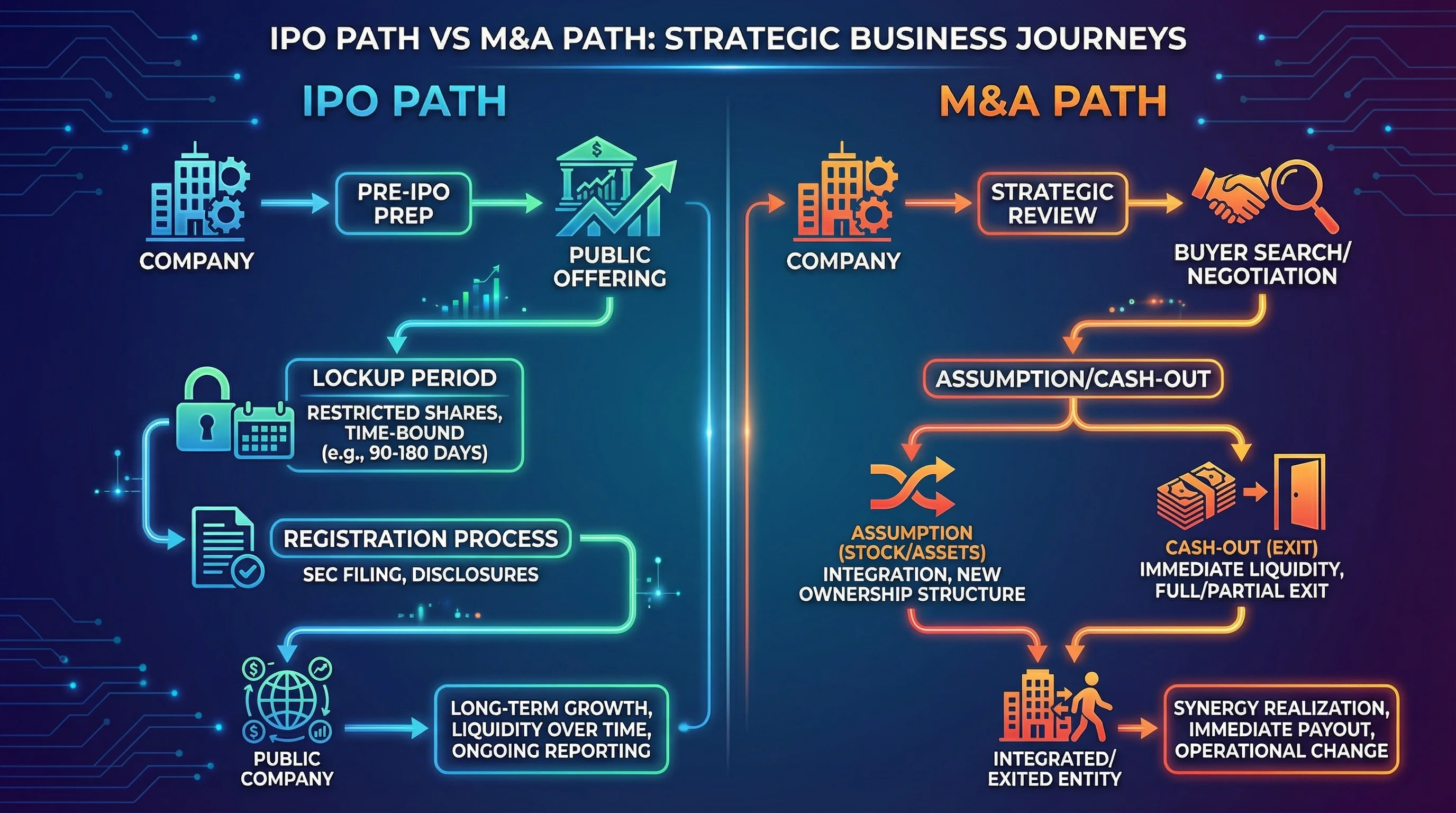

Figure 1: Two conditions—verify definitions in your grant.

Comparison Table (Typical Patterns)

| Dimension | IPO path | M&A path |

|---|---|---|

| Liquidity | Lockup delays selling | May be cash or stock consideration |

| Employment | Often continues | May end or relocate |

| Award handling | May convert to public RSUs | May be assumed/cashed out |

Figure 2: Liquidity and settlement paths differ materially.

Figure 3: Tax timing follows facts—acceleration can bunch income.

Related guides

Disclaimer

Educational—not legal advice.

Primary sources

| Source | URL |

|---|---|

| Investor.gov — IPO | https://www.investor.gov/ipo |