Executive Summary

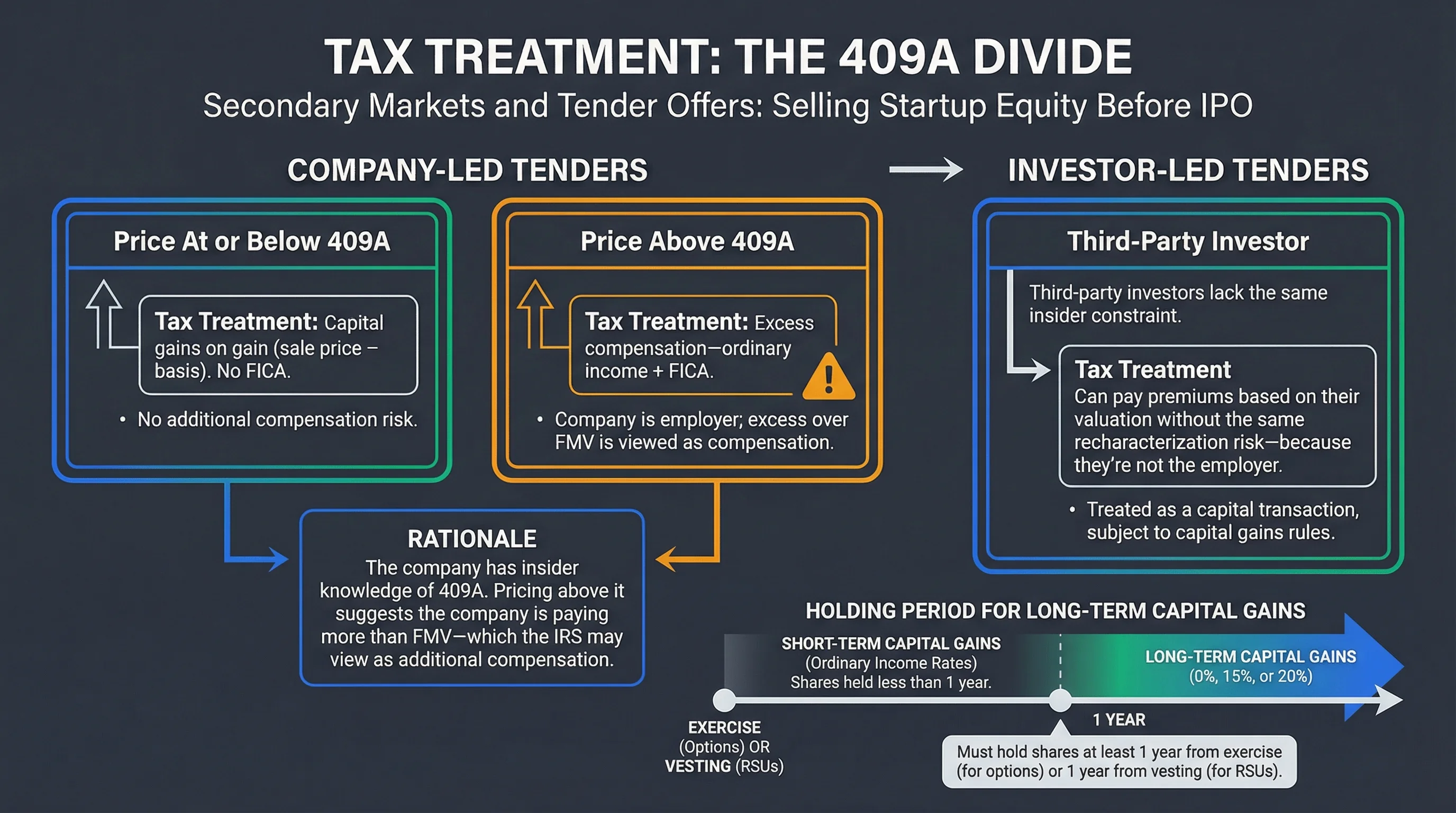

How are tender offer proceeds taxed when selling startup equity?

If the tender price is at or below the company's 409A fair market value, proceeds are generally taxed as capital gains (0%, 15%, or 20% long-term; no FICA). If the company-led tender exceeds 409A FMV, the IRS may treat the excess as compensation—taxed as ordinary income (up to 37%) plus 7.65% FICA. Investor-led tenders from third parties can pay premiums with less recharacterization risk.

Selling startup equity before an IPO—through a company tender offer or a secondary market—can provide liquidity years before a public exit. But tax treatment varies dramatically based on pricing relative to 409A valuation, and SEC rules impose strict timelines.1 Misunderstanding these can turn a $1M gain into a $447K tax bill instead of $200K.

The bottom line: Company-led tenders should price at or below 409A FMV to secure capital gains treatment. Exceeding it by even a small margin can trigger compensation recharacterization for all participants.2

Critical Warning: Company-led tenders priced above 409A valuation can trigger IRS scrutiny. The excess may be treated as compensation across all participants—potentially doubling effective tax rates. Example: $1M at 37% + FICA = ~$447K vs $200K at 20% capital gains.3

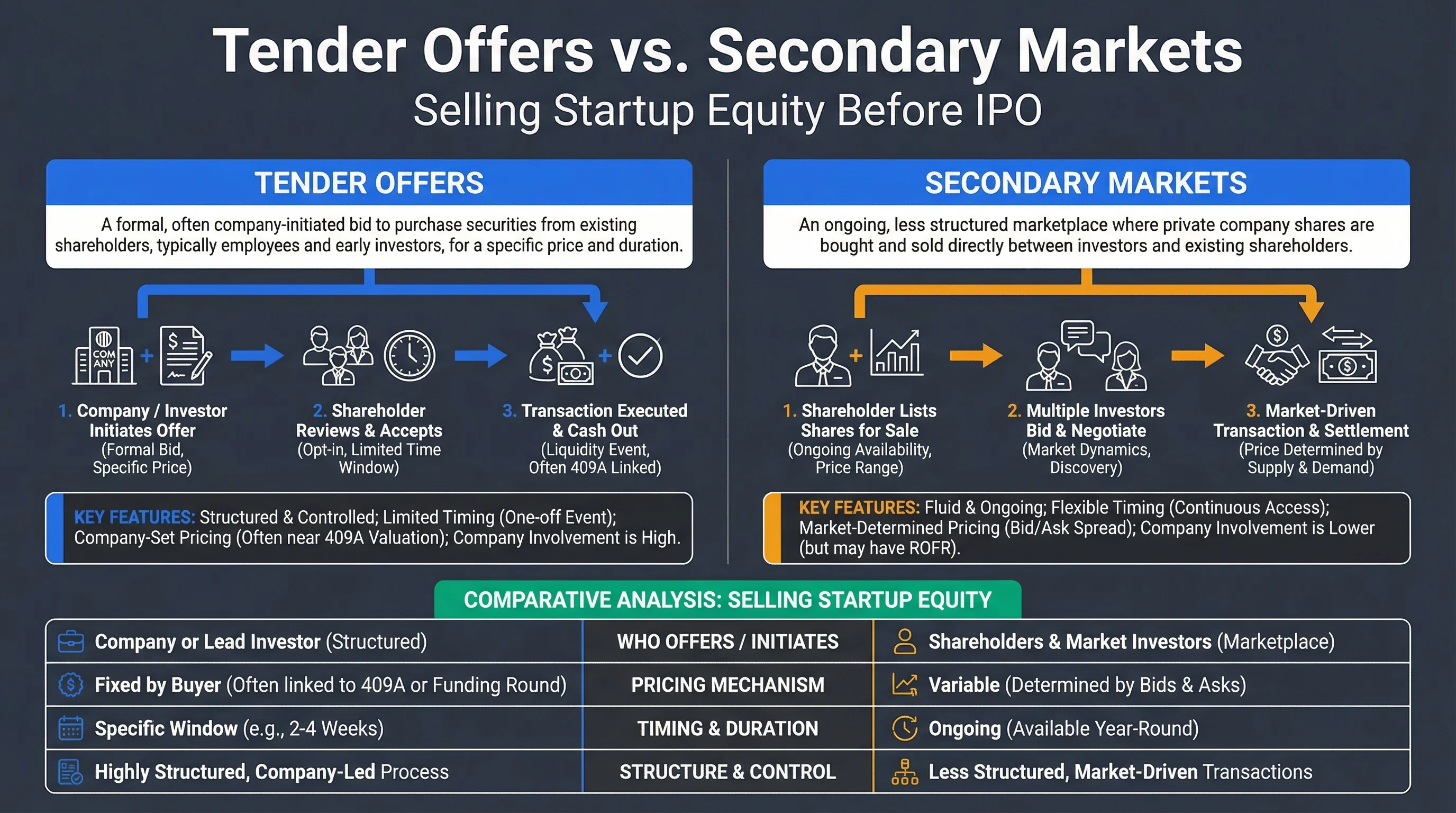

Tender Offers vs Secondary Markets

Tender Offers

A tender offer is a formal bid to purchase securities from shareholders. In startups, the company or an investor typically offers to buy shares from employees and early holders.

Figure 1: Tender offers vs secondary markets — liquidity before IPO.

| Type | Who Offers | Typical Pricing |

|---|---|---|

| Company-led | The company | At or near 409A FMV |

| Investor-led | VC or other buyer | May pay premium; less 409A constraint |

Secondary Markets

Secondary markets (e.g., Forge, SharesPost, company-approved platforms) allow shareholders to sell to qualified buyers. Pricing is often set by the platform or negotiated.

| Consideration | Impact |

|---|---|

| Company approval | Many companies restrict or prohibit secondary sales |

| Right of first refusal | Company may have right to match or block |

| 409A | Sales above 409A can still trigger compensation treatment if structured as company facilitation |

Tax Treatment: The 409A Divide

Company-Led Tenders

| Price vs 409A | Tax Treatment |

|---|---|

| At or below 409A | Capital gains on gain (sale price − basis). No FICA. |

| Above 409A | Excess may be compensation—ordinary income + FICA |

Rationale: The company has insider knowledge of 409A. Pricing above it suggests the company is paying more than FMV—which the IRS may view as additional compensation.

Investor-Led Tenders

Third-party investors lack the same insider constraint. They can pay premiums based on their valuation without the same recharacterization risk—because they're not the employer.

Holding Period

For long-term capital gains (0%, 15%, or 20%), you must hold shares at least 1 year from exercise (for options) or 1 year from vesting (for RSUs). Short-term gains are taxed as ordinary income.

Related Guides: Section 409A Valuation, Capital Gains Calculator.

Figure 2: The 409A divide — capital gains vs compensation treatment.

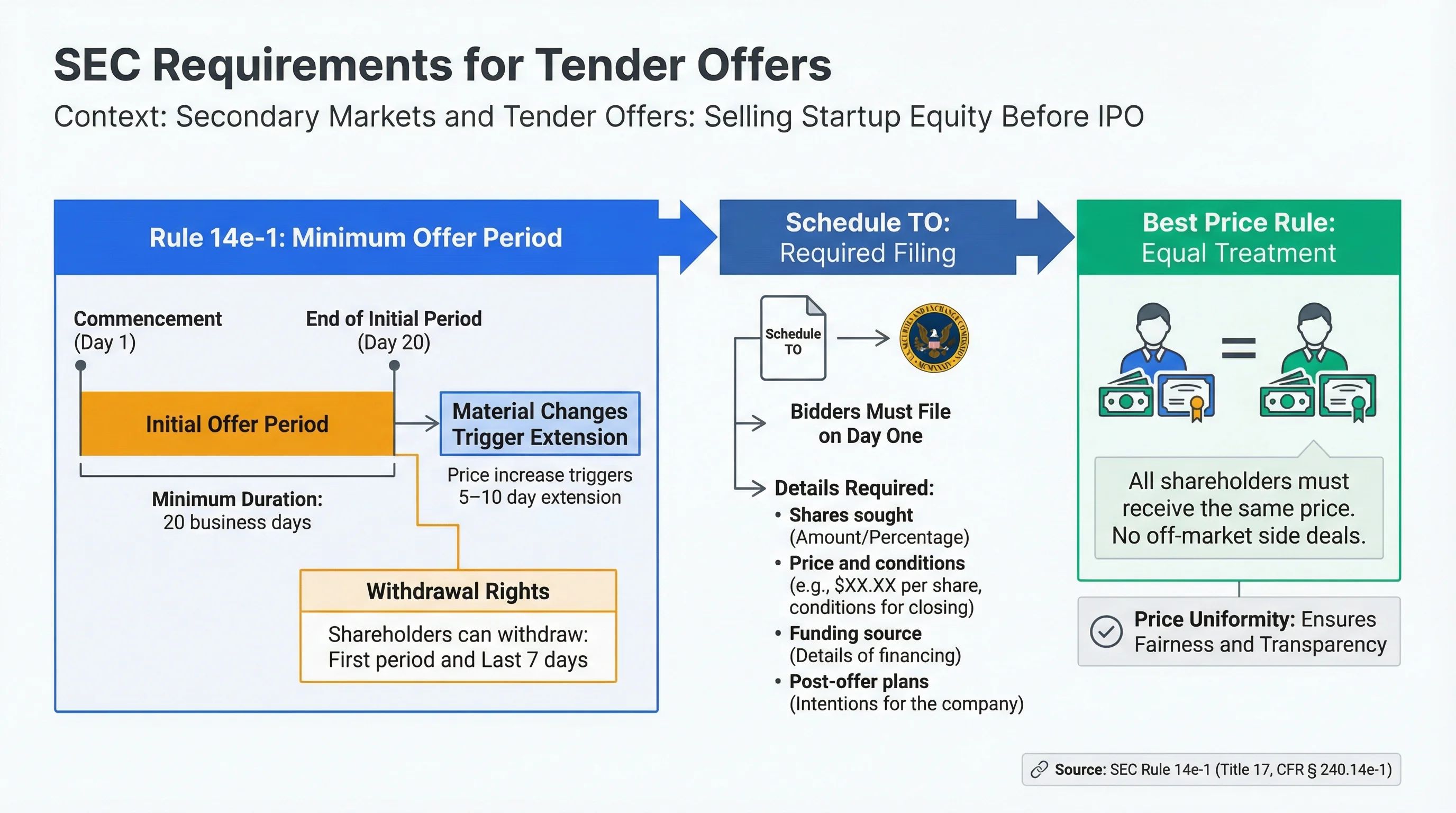

SEC Requirements for Tender Offers

Rule 14e-1: Minimum Offer Period

| Requirement | Specification |

|---|---|

| Minimum duration | 20 business days from commencement |

| Material changes | Price increase triggers 5–10 day extension |

| Withdrawal rights | Shareholders can withdraw in first period and last 7 days |

Schedule TO

Bidders must file Schedule TO with the SEC on day one, detailing:

- Shares sought

- Price and conditions

- Funding source

- Post-offer plans

Best Price Rule

All shareholders must receive the same price. No off-market side deals.

Source: SEC Rule 14e-1

QSBS Considerations

If you hold Qualified Small Business Stock (QSBS) under IRC Section 1202, redemptions can affect eligibility:

| Redemption Level | QSBS Impact |

|---|---|

| Under 5% | Generally no disqualification |

| Over 5% | Can disqualify QSBS for shares issued in prior 2-year windows—even for non-sellers |

Implication: Large company-led tenders (e.g., 10% of shares) can wipe out QSBS benefits for other shareholders. Structure matters.

Related Guides: QSBS Exclusion: Tax-Free Startup Exit.

Figure 3: SEC requirements — minimum offer period and filings.

Practical Considerations

Eligibility

Many tenders are limited to:

- Vested shares only (no unvested)

- 6-month post-exercise hold (for options)

- Board approval and plan compliance

- Eligible shareholders (employees, former employees, etc.)

Documentation

Keep records of:

- 409A valuation at time of offer

- Your cost basis

- Holding period (grant, exercise, sale dates)

- Offer documents and communications

Frequently Asked Questions

Can I sell on a secondary market without company approval?

Answer: Depends on your company's policy and stock agreement. Many agreements include right of first refusal, transfer restrictions, or outright prohibitions. Violating can trigger repurchase at unfavorable terms.

What if the tender price is between my basis and 409A?

Answer: Your gain (sale price − basis) is generally capital gains if the price is at or below 409A. The 409A ceiling matters for whether the company is seen as paying above FMV—not for your personal gain calculation.

How often do companies run tender offers?

Answer: Varies. Some run annual tenders; others do them before a funding round or when liquidity is needed. Ask your company or equity administrator.

Does participating in a tender affect my other equity?

Answer: Selling in a tender is a taxable event for the shares sold. It doesn't directly affect unvested or unsold shares—but large redemptions can affect QSBS for the company.

What is the typical discount on secondary markets?

Answer: Secondary buyers often demand a discount (10–30%) for illiquidity and risk. Pricing depends on company stage, traction, and buyer demand.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRC Section 409A | Reference | https://www.law.cornell.edu/uscode/text/26/409A |

| SEC Rule 14e-1 | Reference | https://www.law.cornell.edu/cfr/text/17/240.14e-1 |

| IRC Section 1202 | Reference | https://www.law.cornell.edu/uscode/text/26/1202 |

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Always consult a qualified tax professional before making decisions based on this information.