Executive Summary

Where does my ISO bargain element go on Form 6251?

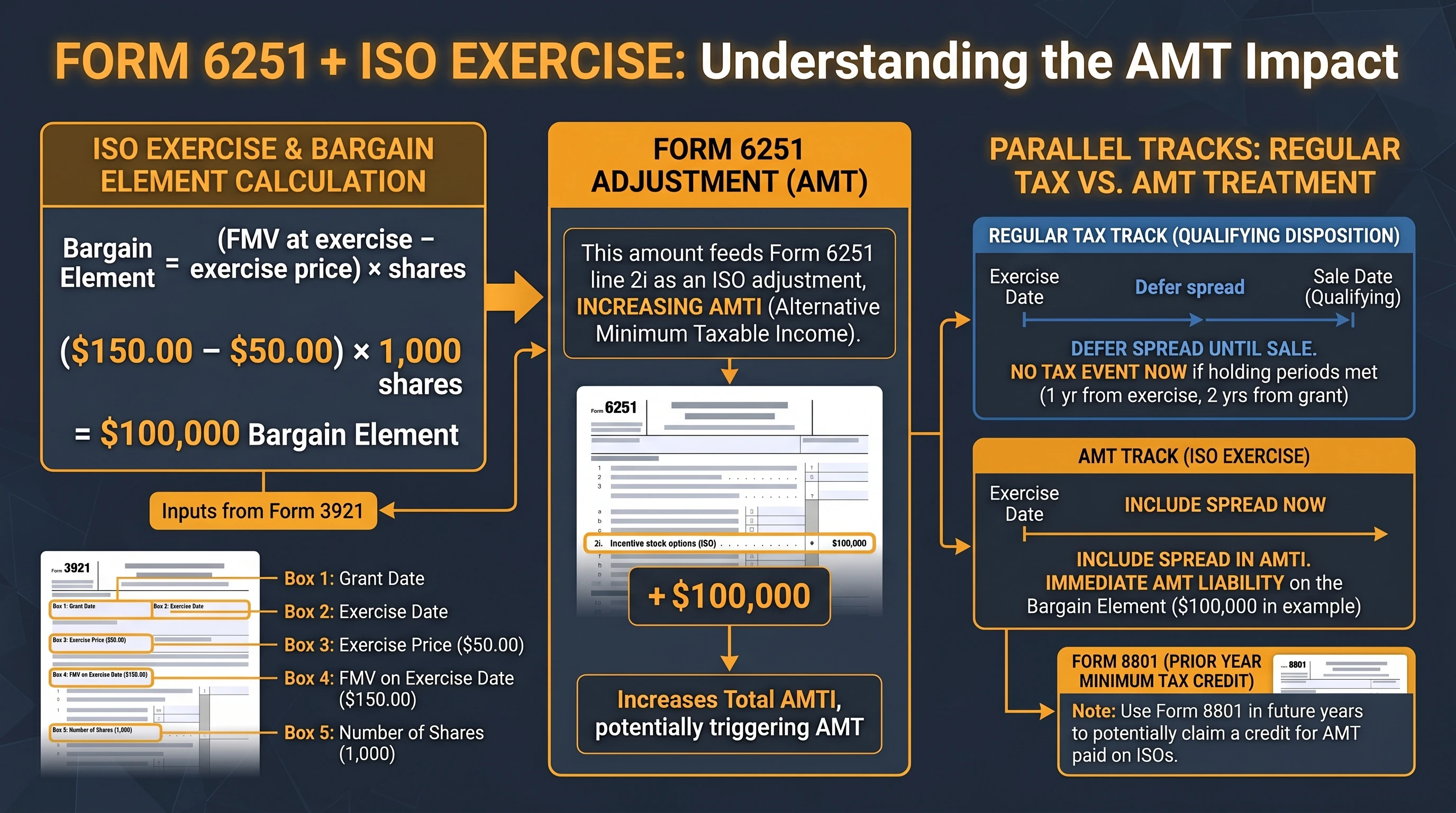

Generally on line 2i as an incentive stock option adjustment—multiplying the spread per share reported on Form 3921-style data by exercised shares generates the preference item widening Alternative Minimum Taxable Income when you exercised and held ISO stock through year-end rather than disqualifying disposition same year.

Form 6251 frightens sober engineers because nothing on the paycheck stub whispers “Congrats—you triggered parallel universe tax.” No email from payroll explains that Federal Regular Tax deferred your ISO appreciation yet Federal AMT swallowed it overnight like rogue AI alignment failure. Instructions begin bluntly that Form exists to compute alternative minimum tax when law delivers favorable treatment elsewhere leaving high economic income untouched by ordinary brackets—which is jargon for “your ISO spreadsheet just became existential.”1

Treat this guide as cockpit placard labeling, not cockpit replacement: read the official PDF concurrently. Deep theory—crossover calculus, disqualifying disposition trade-offs—lives primarily in AMT planning; ISO vs NSO economics in ISO vs NSO; same-day-sale mechanics in when to exercise ISO.

The bottom line: Form 6251 is how you reconcile dual ledgers: where regular tax politely deferred wage-like spread and where AMT says pay now-ish absent protective selling.

Critical Warning: Exercising private ISO blocks can generate six-figure AMT liabilities payable April 15 even if shares remain illiquid. Model cash—not just tax rates—before signature.2

Anatomy of Parallel Tax Computation (Why Line 2i Isn't Isolated Chess Piece)

Federal individual returns compute regular tax first broadly familiar from W-4 withholding tables. Alternative Minimum Tax rebuilds taxable income skeleton into Alternative Minimum Taxable Income (AMTI) by injecting adjustments/preferences IRC enumerates—for ISO exercised-and-held shares IRC §56(b)(3) dictates treatment as adjustment absent statutory carve-outs qualifying as wages elsewhere.3

High-level scaffolding:

AMTI roughly ≈ taxable income BEFORE some regular-only benefits

+ iso spread + other enumerated adjustments (state tax addback, etc.—contextual)

Minus AMT exemption (subject to phaseout)

→ Apply tentative minimum tax marginal rates → compare to regular tax liability

Incremental AMT = max(TMT − Regular tax computed per form, $0 rounded conventions)

Form 6251 implements mechanical tabs—consult PDF each tax year since exemption dollars and phaseouts shift pursuant to statutes like post-OBBA sunsets or One Big Beautiful Bill adjustments discussed in contemporaneous summaries (verify via IRS Publications & Revenue Procedures in effect for your taxable year—not blog posts—even ours). Pair with tax season equity reporting synopsis for calendar orientation.

Source Documents Needed Before Opening Form 6251 Software Tab

| Document | Field highlights | Why it matters |

|---|---|---|

| Form 3921 | Grant date, exercise date, exercise price FMV/share, share count exercised | Validates spread math |

| Supplemental W-2 equity letter | Sometimes clarifies employer adjustments | Cross-check |

| Broker statements | Lot holding status after exercise | Holding vs sale same year |

| Prior year Form 6251/8801 | Credit carryforwards | Continuity |

| State K-1 / CA adjustments | CA taxes spread at exercise | Dual filing traps |

If Form 3921 missing by January 31 deadline, escalate through stock plan admin—without it you’re approximating using internal equity portal exports (dangerous if dispute arises).

Line 2i ISO Adjustment: Quantitative Walkthrough

Assume Form 3921 states:

| Field | Value |

|---|---|

| Exercise price | $8.50 |

| FMV at exercise | $42.10 |

| Shares | 5,000 |

Spread/share = $42.10 − $8.50 = $33.60

Total preference = $33.60 × 5,000 = $168,000

Line 2i includes this $168,000 (subject to possible partial disposition nuance if mixed same-year sales) inflating AMTI before exemption math. Variation: same-day sale may reclassify portion as ordinary via disqualifying path—see disqualifying disposition payroll guide.

Worked partial-year nuance illustration (simplified illustrative only):

| Scenario | Ordinary wage ISO component | Typical AMT line 2i |

|---|---|---|

| Pure hold post exercise | Near $0 statutory wage | Full spread adjustment |

| Disqualifying same calendar year ordinary inclusion | Ordinary income on bargain element reflected on W-2 | Reduced or eliminated ISO preference for those shares |

Always confirm actual IRS instructions—you cannot rely on conversational blogs alone mid-March.

A Worked “TMT vs Regular Tax” Illustration (Highly Simplified)

Assume (illustrative numbers only—not your tax bracket promise):

| Item | Hypothetical amount |

|---|---|

| Regular taxable income before ISO preference | $420,000 |

| ISO spread from line 2i style adjustment | $168,000 |

| Other AMT additions (illustrative SALT addback etc.) | $40,000 |

Conceptual AMTI balloon might land near $628,000 before exemptions and phaseouts—not your actual return, but this is how one large exercise can jump tax bases orthogonal to withholdings from salary. Subtract AMT exemption (if available after phaseout rules in the Instructions), apply tentative marginal rates (often described as blended 26%/28% bands in explanatory literature—still read the authoritative rate schedule in the Instructions each year rather than trusting static blog tables), subtract regular income tax liability already computed, and the surplus (if positive) is the incremental AMT you must fund by April deadlines or estimated payments.

When your already computed regular tax is high—because RSUs vesting stacked ordinary wages at 37%—the gap between tentative minimum tax and regular tax narrows or vanishes entirely. Conversely, exercising ISOs during a sabbatical / parental leave low-cash‑salary year frequently maximizes unpleasant AMT relative to withheld taxes. Coordination narratives appear across married filing equity strategies and year‑end equity planning if household timing flexibility exists.

Employees sometimes ask whether bonus deferral elections interplay—corporate payroll rules vary widely; securities law and Section 409A constraints dominate before tax optimization fantasies mature.

Form 3921 Boxes You Should Triple-Read Before Touching Line 2i

Form 3921 is not poetic literature—it's a grid. Before typing anything into TurboTax Deluxe’s “ISO exercise” worksheet, verify:

| Typical data element | Verification hack |

|---|---|

| Date granted versus early exercise quirks | Wrong grant date nukes disqualifying timelines |

| Exercise price per share | Typo cascades squared across thousands of shares |

| Fair market value on exercise date employer certifies | Board minute vs internal equity portal—escalate conflicts |

| Number of shares transferred exercise event | Split‑adjusted historical grants sometimes surprise |

If supplemental statements reconcile sell-to-cover ISO mechanics (shares sold at exercise to fund cost), ensure you know which share lots continued—only continuing lots drive future AMT basis conversations on disposition. Our stock option exercise methods guide enumerates trade-offs at high level.

Where Form 6251 Sits in the Filing Stack (Sequencing Discipline)

Although every software vendor UX differs, conceptually you should:

- Complete ordinary Form 1040 wage and investment income skeleton (W-2, interest, ordinary dividends, capital gains summary imports).

- Insert ISO exercise information from Form 3921 into both regular modules (if any ordinary components or state differences) and AMT modules.

- Allow Form 6251 to compute incremental AMT; verify Form 1040 line mapping in current year instructions (line numbers move—never memorize).

- If incremental AMT > 0, open Form 8801 to update credit carryforwards and document future recovery scenarios.

- Print PDF review package—spot check that line 2i equals spreadsheet spread unless partial dispositions spread adjustments.

Skipping step 5 is how otherwise brilliant engineers pay penalties for transposed digits discoverable in ten minutes of human review.

Relationship Between Basis for Regular Capital Gains vs AMT Carryforward Stock

Employees selling ISO shares after exercise track dual basis:

| Ledger | Typical basis anchor | Commentary |

|---|---|---|

| Regular schedule D | Strike paid + adjustments from qualifying/disqualifying rules per IRC §422 | Mirrors consumer brokerage reporting quirks |

| AMT parallel | Often FMV at exercise layering | Generates future negative adjustments / credit interplay |

Selling triggers potential negative AMT adjustments summarized in Instructions around disposition timing—coordinate with CPA when multi-year ladders exist. Mentioned interplay appears also in AMT planning guide Figures.

Form 8801: Not Optional Bonus Round

IRS About Form 8801 states purpose: credit for prior year minimum tax—Individuals/Estates—but practical translation: leftover AMT you effectively prepaid may offset regular tax future years via carryforward tracked there when regular tax dominates AMT later.4 Credits do not spontaneously auto-attach—maintain spreadsheets.

Misconception patrol:

| Myth | Reality |

|---|---|

| “AMT vanished after TCJA—I ignore 6251” | ISO exercises still resurrect AMT for many—not dead |

| “I can deduct ISO AMT on Schedule A” | No—capital/finance Twitter lies |

| “Form 3921 duplicates W-2 so skip” | W-2 narratives differ—3921 authoritative for spreads |

California / State Non-Conformity Flash Warning

Federal may defer taxing ISO appreciation until disposition while computing AMT quirks; California historically taxes spread at ordinary rates at exercise—employees oscillating Palo Alto ↔ Austin must model dual ledgers. See California equity guide—but remember our Form 6251 narrative is predominantly federal anatomy.

Crossover Exercise Planning Tie-In

Before scaling exercises, compute crossover shares using methodology in AMT planning—functionally solving how many shares keep TMT below regular tax line after exemption phaseouts. Not legal advice; purely mechanical guardrail.

Documentation Discipline for Future Audits

Maintain immutable folder:

- PDF Form 3921 each year

- Exercise acceptance emails with timestamps

- Broker lot creation screenshot post-settlement

- Copy of filed Form 6251 + Form 8801 PDF export

- Spreadsheet linking each lot to regular vs AMT basis

If IRS examination letter arrives, calm responses beat frantic broker calls.

Figure 1: ISO exercise data (Form 3921) feeding the Form 6251 ISO adjustment path and linking conceptually to Form 8801 credit tracking.

Frequently Asked Questions

Must I file Form 6251 if I only exercised NSOs?

Answer: NSO exercises generally generate ordinary wage income at exercise—no statutory ISO AMT preference duplicating line 2i pattern. However other AMT adjustments may still apply depending on full return—run diagnostic in software or professional model.5

Source: IRS About Form 6251

What if my employer mis-reported FMV on Form 3921?

Answer: Freeze documentation from board valuation / 409A memo contemporaneous with grant/exercise cycles; escalate through legal/tax—not DIY silent override without representation.

Can estimated tax installments cover ISO AMT April surprise?

Answer: Estimated rules hinge on annualized income method vs safe harbors—estimated tax equity guide explains mechanics; AMT lumps can break safe harbor if ignored until Q4.

Does holding ISO shares through IPO lockup change line 2i timing?

Answer: AMT event tied to exercise year hold past Dec 31—not lockup release—liquidity mismatch is risk not timing shift.

What about Form 6251 for ISO exercises done via net exercise?

Answer: Mechanical share counts differ; economic spread still matters—reconcile plan administrator PDF with broker net-share deposit; consider option exercise methods compared.

Should I use the VestingStrategy ISO AMT calculator?

Answer: ISO AMT impact tool offers modeling guardrails but cannot replace personalized advice or final Form 6251 software validation.

How does Form 8801 differ from Form 6251?

Answer: Form 6251 computes current-year AMT liability; Form 8801 tracks prior-year minimum tax credit mechanics when regular tax later exceeds AMT—sequential not substitutive.6

Source: About Form 8801

Can renouncing ISO status mid-year retroactively lower AMT?

Answer: Statutory ISO requirements are strict—once valid ISO exercise occurs, you cannot “undo” by wishful thinking; disposition strategies exist but have tax trade-offs—consult advisor before attempting label games.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| About Form 6251 | IRS overview | irs.gov/forms-pubs/about-form-6251 |

| Instructions for Form 6251 | irs.gov/pub/irs-pdf/i6251.pdf | |

| IRC §56 | Statute | law.cornell.edu/uscode/text/26/56 |

| Instructions for Form 3921 | IRS | irs.gov/instructions/i3921 |

| About Form 8801 | IRS | irs.gov/forms-pubs/about-form-8801 |

Research note

Topic selection followed the CCO topic queue (docs/processes/CCO-CONTENT-RECOMMENDATIONS.md). The automated Perplexity research pipeline could not run here due to API quota exhaustion, so this article was drafted from IRS primary materials (About Form 6251, Form 6251 instructions PDF, About Form 8801, Form 3921 instructions, IRC §56) and cross-linked internal guides. The infographic was generated with Gemini gemini-3-pro-image-preview and saved as WebP per docs/processes/CURSOR-CONTENT-CREATION.md.

Disclaimer

Educational only—not individualized tax advice. AMT parameters change with legislation; confirm each tax year’s Form 6251 instructions and your specific grant agreements with a qualified professional.

Footnotes

-

IRS About Form 6251 overview language—AMT limits benefits reducing regular tax. irs.gov/forms-pubs/about-form-6251 ↩

-

Liquidity vs AMT mismatch discussed qualitatively across multiple site ISO strategy guides; not quantified legal rule. ↩

-

IRC §56(b)(3) statutory anchor. law.cornell.edu/uscode/text/26/56 ↩

-

About Form 8801 description. irs.gov/forms-pubs/about-form-8801 ↩

-

General NSO wage inclusion vs ISO deferral contrast—see also ISO vs NSO guide. ↩

-

Distinct forms—read both PDF instruction sets annually. ↩