Executive Summary

What is an ISO Disqualifying Disposition?

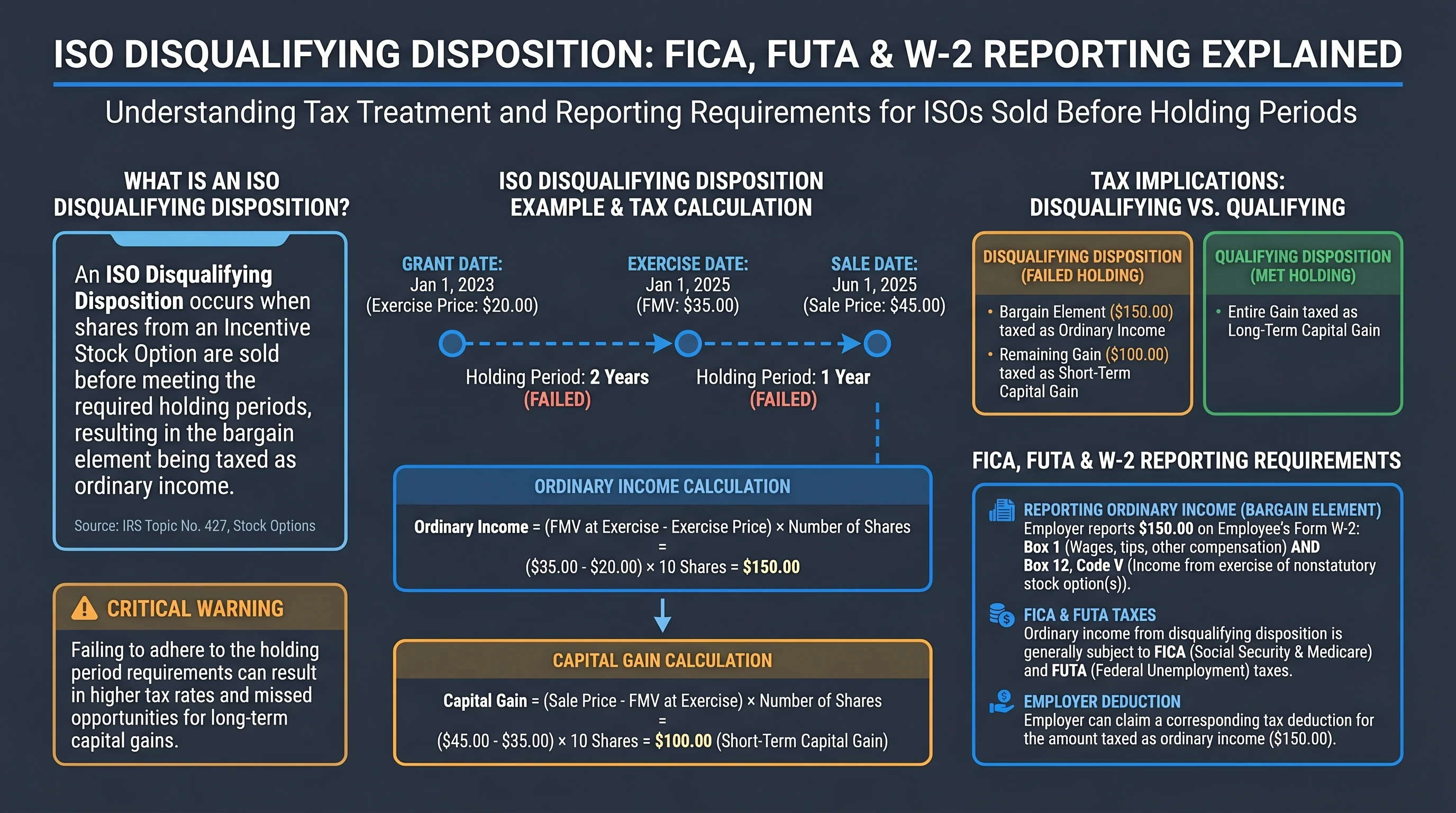

An ISO Disqualifying Disposition occurs when shares from an Incentive Stock Option are sold before meeting the required holding periods, resulting in the bargain element being taxed as ordinary income.

Incentive Stock Options (ISOs) can produce no regular wage income at exercise if you are still inside the statutory ISO rules—but the story changes the moment you sell too early. A disqualifying disposition generally taxes the bargain element (FMV at exercise minus strike) as ordinary wage income for income tax, reported on Form W-2. That wage treatment sounds like “payroll taxes should apply”—and for NSOs they usually do. For ISOs, Congress carved a specific exception: remuneration on account of ISO exercise or any disposition of the stock is excluded from FICA and FUTA wages under 26 U.S.C. §3121(a)(22) and the parallel §3306(b)(19) rule for FUTA.1

This guide is the narrow complement to our ISO qualifying vs disqualifying disposition overview and our broader FICA on equity framing: income tax vs payroll tax often diverge for ISOs even when you disqualify a sale.

The bottom line: A disqualifying disposition of ISOs can significantly impact your tax liability, converting potential capital gains into ordinary income2.

Critical Warning: Failing to adhere to the holding period requirements can result in higher tax rates and missed opportunities for long-term capital gains3.

Understanding ISO Disqualifying Dispositions

Definition and Tax Implications

A disqualifying disposition occurs when an employee sells shares acquired through an ISO before satisfying the holding period requirements: two years from the grant date and one year from the exercise date. Under IRC §421(b), this results in the bargain element being taxed as ordinary income, reported on the employee's Form W-2. The employer can claim a corresponding deduction for this amount.

Example Calculation

Consider an ISO granted on January 1, 2023, with a $20 exercise price. The employee exercises on January 1, 2025, when the FMV is $35 per share, and sells on June 1, 2025, for $45 per share for 1,000 shares. The sale is before two years from grant and before one year from exercise—classic disqualifying disposition.

Ordinary wage income (spread at exercise) = ($35 − $20) × 1,000 = $15,000

Post-exercise appreciation taxed as capital gain = ($45 − $35) × 1,000 = $10,000

Because the holding periods fail, the $15,000 is generally ordinary income (often W-2 wages), while the $10,000 is typically short-term capital gain if the holding period from exercise to sale is one year or less. If the stock had been sold below exercise-date FMV, the ordinary wage piece is generally capped at the actual economic gain on the sale—this “cap” rule is why same-day sales with a tiny gain can produce small ordinary income even when the spread at exercise looked large on paper.4

Statutory Framework

Under IRC §422(a)(1), a qualifying disposition allows the entire gain to be taxed as a long-term capital gain. In contrast, a disqualifying disposition under IRC §421(b) results in the bargain element being taxed as ordinary income, with the employer reporting this on Form W-2, Box 1 and Box 12, Code V.

| Scenario | Income tax (individual) | Typical FICA/FUTA on ISO spread / DD wages |

|---|---|---|

| Qualifying disposition | Generally long-term capital gains on sale (no wage inclusion of spread at sale) | No FICA/FUTA on ISO exercise/disposition amounts (same statutory carve-out) |

| Disqualifying disposition | Ordinary wage income equal to spread at exercise (capped by economic gain on sale); remainder often capital gain/loss | Still no FICA/FUTA on amounts within §3121(a)(22) / §3306(b)(19) |

Critical distinction: “No FICA/FUTA” here refers to the ISO statutory exclusion for exercise and stock disposition—not a general rule that wage-labeled income never attracts payroll taxes. If your options lose ISO status (for example, exercise after the post-termination window in IRC §422(a)(2)), the spread is often treated like NSO wages—and FICA/FUTA commonly applies like any other compensation.5

Withholding: Even when payroll taxes do not apply, ordinary income from a disqualifying disposition can still create a large income tax liability. Many employees pair this analysis with supplemental wage withholding concepts and estimated taxes.

ISO disqualifying dispositions: ordinary income on the exercise spread (income tax) can coexist with a federal payroll-tax exclusion for statutory ISO exercise and stock disposition amounts—educational only, not individualized tax advice.

Reporting Requirements and Deadlines

Employer Obligations

Employers must report the ordinary income from a disqualifying disposition on the employee's Form W-2 by January 31 of the following year. Additionally, Form 3921 must be issued to the employee by January 31 following the year of exercise, detailing the ISO exercise information.

Example Reporting

For an ISO exercised in 2025, the employer must:

- Report the bargain element as wages on Form W-2, Box 1 and Box 12, Code V by January 31, 2026.

- Provide Form 3921 to the employee by January 31, 2026.

Employee Reporting

Employees must report the ordinary income on their Form 1040, adjusting the basis of the shares by the amount of ordinary income recognized. The capital gain or loss from the sale is reported on Schedule D.

Example Basis Adjustment

Using the 1,000-share example, basis for the sale generally reflects the ordinary income you already reported:

Basis per share = Strike + (ordinary wage income per share)

Basis per share = $20 + ($15,000 / 1,000) = $35

| Form | Purpose | Typical deadline |

|---|---|---|

| Form W-2 | Wages including disqualifying disposition income (often Box 12, Code V) | January 31 (employee copy) |

| Form 3921 | ISO exercise facts (grant/exercise price, dates, shares) | January 31 following exercise year |

| Schedule D / Form 8949 | Stock sale capital gain/loss after basis adjustment | Tax filing due date |

Critical Warning: Failure to report a disqualifying disposition accurately can result in penalties and interest6.

Strategic Considerations for ISO Holders

Timing and Tax Planning

To maximize tax benefits, employees should aim to meet the holding period requirements for ISOs. This strategy allows the entire gain to be taxed at the more favorable long-term capital gains rate.

Example Timing Strategy

If the employee in the 1,000-share example had waited until January 2, 2026 to sell (after two years from grant and one year from exercise), the sale is generally a qualifying disposition: the $15/share spread at exercise is not ordinary wages, and the gain is typically long-term capital gain measured against your exercise price basis:

Long-term capital gain ≈ ($45 − $20) × 1,000 = $25,000

You may still have had AMT consequences in 2025 if you exercised and held—this is why “hold for LTCG” is not automatically “free” tax planning.4

Post-Termination Considerations

Employees must exercise ISOs within three months of termination to retain their status. If exercised later, the options are treated as non-qualified stock options (NQSOs), subjecting the bargain element to ordinary income tax at exercise.

| Scenario | ISO Status |

|---|---|

| Exercise within 3 months | Retain ISO status |

| Exercise after 3 months | Treated as NQSO |

Important Note: Exercising ISOs post-termination without meeting the three-month deadline results in immediate taxation of the bargain element7.

Same-day sale vs “hold a little, still disqualify”

Not every disqualifying disposition is a broker same-day sale. Some employees exercise, hold a few months, then sell before the one-year exercise clock finishes—still a disqualifying sale, but the capital gain/loss leg depends on movement after exercise.

| Pattern | Ordinary income piece (typical) | Capital gain/loss piece (typical) | Payroll tax (typical for statutory ISO) |

|---|---|---|---|

| Same-day sale / cashless exercise | Spread at exercise (subject to cap if sale price < FMV) | Often small; may be tiny if sale price ≈ FMV | FICA/FUTA carve-out for ISO amounts |

| Sell 6 months after exercise (too early) | Spread at exercise (capped by gain) | Price change after exercise | FICA/FUTA carve-out for ISO amounts |

| Exercise after ISO lapses to NSO | Spread at exercise as wages | Later stock sale separately | FICA/FUTA often apply like other wages |

If your plan uses a sell-to-cover mechanic on an ISO exercise, treat it as a disqualifying disposition unless you already met the holding periods—see stock option exercise methods compared.

Form 3921 vs brokerage 1099-B (why basis looks “wrong”)

Form 3921 tells the IRS the ISO exercise facts. Your broker’s Form 1099-B may show cost basis that does not yet reflect the W-2 ordinary income you must fold into basis for a disqualifying disposition. Before you import 1099-B totals into tax software, reconcile:

- W-2 Box 12 Code V (or other wage reporting your payroll team uses)

- Form 3921 exercise price and FMV

- Trade confirmations for sale date and proceeds

Deeper form walkthrough: equity reporting: Forms 3921, 3922, and W-2. Box 14 memos: W-2 Box 14 equity codes.

Alternative Minimum Tax (AMT) Considerations

AMT Implications

Exercising ISOs can trigger the Alternative Minimum Tax (AMT) due to the bargain element being included in AMT income. However, a disqualifying disposition eliminates the AMT adjustment for the bargain element, as it is taxed as ordinary income instead.

Example AMT Calculation

Assume an employee exercises ISOs with a $10 exercise price and a $50 FMV, resulting in a $40 bargain element per share. If the shares are sold in the same year, the AMT adjustment is avoided:

AMT Adjustment = 0 (due to disqualifying disposition)

AMT Relief Strategies

To mitigate AMT exposure, employees can:

- Plan the timing of ISO exercises and sales to avoid overlapping tax years.

- Consider exercising ISOs in years with lower overall income to minimize AMT impact.

| Strategy | Benefit |

|---|---|

| Same-year exercise/sale | Avoids AMT adjustment |

| Low-income year exercise | Reduces AMT exposure |

Critical Warning: AMT can significantly increase tax liability if not properly planned for8.

Comparison with Non-Qualified Stock Options (NQSOs)

Key Differences

Unlike ISOs, nonqualified stock options (NSOs) generally treat the spread at exercise as wages for both income tax and payroll tax purposes—see our ISO vs NSO comparison.

| Feature | ISO (statutory) | NQSO |

|---|---|---|

| Regular tax at exercise | Usually none if ISO rules satisfied | Ordinary wages on spread |

| FICA/FUTA on spread | Excluded for ISO exercise/disposition amounts under §3121(a)(22) / §3306(b)(19) | Generally wages for payroll tax |

| AMT | Common AMT adjustment at exercise if you hold | No ISO-style AMT adjustment |

Example Comparison

Consider 100 options, $10 strike, $50 FMV at exercise:

- ISO hold (no same-year sale): Often $0 regular wages at exercise; potential AMT on the $4,000/share × 100 spread.

- ISO same-day sale (disqualifying): Roughly $4,000/share × 100 = $40,000 ordinary wages for income tax; still generally outside FICA/FUTA wage base under the ISO carve-outs.

- NQSO exercise: Roughly $40,000 wages with typical payroll tax mechanics.

Important Note: The choice between ISOs and NQSOs should consider both tax implications and personal financial goals9.

Frequently Asked Questions

What is a disqualifying disposition of ISOs?

Answer: A disqualifying disposition occurs when shares acquired through an ISO are sold before meeting the required holding periods: two years from the grant date and one year from the exercise date. This results in the bargain element being taxed as ordinary income.

Source: IRS Topic No. 427, Stock Options

How is the bargain element taxed in a disqualifying disposition?

Answer: The bargain element, which is the difference between the FMV at exercise and the exercise price, is taxed as ordinary income and reported on Form W-2.

Source: Treas. Reg. §1.421-2

Are there any payroll taxes on a disqualifying ISO disposition?

Answer: For statutory ISO amounts, federal FICA and FUTA generally do not apply to remuneration on account of ISO exercise or disposition of the stock—see 26 U.S.C. §3121(a)(22) and §3306(b)(19). That is different from income tax: the disqualifying disposition can still produce large ordinary income on your W-2. It is also different from NSOs, where the spread is commonly wages for both income and payroll tax. If your option ceases to be an ISO, expect payroll tax treatment closer to NSOs.

Source: 26 U.S.C. §3121(a)(22); 26 U.S.C. §3306(b)(19)

What forms are required for reporting a disqualifying disposition?

Answer: Employers must report the income on Form W-2, and provide Form 3921 to the employee detailing the ISO exercise.

Source: IRS Form 3921 Instructions

How does a disqualifying disposition affect AMT?

Answer: A disqualifying disposition eliminates the AMT adjustment for the bargain element, as it is taxed as ordinary income instead.

Source: IRS Publication 525

Can ISOs be exercised after termination?

Answer: Yes, but to retain ISO status, they must be exercised within three months of termination. Otherwise, they are treated as NQSOs.

Source: IRC §422(a)(2)

What happens if I sell my ISO shares at a loss?

Answer: If you sell your ISO shares at a loss, the loss can be used to offset other capital gains. If the loss exceeds your capital gains, you can use up to $3,000 ($1,500 if married filing separately) to offset other income, with the remainder carried forward to future years.

Source: IRS Publication 550

How does a disqualifying disposition impact state taxes?

Answer: State tax treatment of a disqualifying disposition can vary. Some states conform to federal tax treatment, taxing the bargain element as ordinary income, while others may have different rules. It's important to consult with a tax advisor familiar with your state's tax laws.

Source: State Tax Departments

Can I avoid a disqualifying disposition by gifting ISO shares?

Answer: Gifting ISO shares before meeting the holding period requirements generally results in a disqualifying disposition. The bargain element is still taxed as ordinary income to the donor, and the recipient takes the donor's basis and holding period.

Source: IRS Gift Tax

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRS Topic No. 427, Stock Options | IRS | irs.gov |

| IRC §3121(a)(22) (FICA wage exclusion for ISO exercise/disposition) | Statute | law.cornell.edu |

| IRC §3306(b)(19) (FUTA wage exclusion—parallel) | Statute | law.cornell.edu |

| IRC §421 / §422 (ISO statutory rules) | Statute | law.cornell.edu §421; §422 |

| Treas. Reg. §1.422-1 | Regulation | eCFR |

| IRS Form 3921 Instructions | IRS | irs.gov |

| IRS Publication 525 | IRS | irs.gov |

Disclaimer: This guide is for general education only and is not individualized tax, legal, or investment advice. Tax rules change, and your facts (employer plan design, residency, treaty status, payroll reporting) may differ. Consult a qualified tax professional before making decisions.

Footnotes

-

26 U.S.C. §3121(a)(22) excludes from FICA wages remuneration on account of ISO exercise or disposition of the stock; 26 U.S.C. §3306(b)(19) parallels the exclusion for FUTA wages. ↩

-

IRS Topic No. 427, Stock Options — high-level ISO overview. ↩

-

Treas. Reg. §1.422-1 — holding period mechanics for ISO dispositions. ↩

-

IRS Publication 525 discusses ISO disqualifying disposition income measurement and basis adjustments—verify examples against your facts. ↩ ↩2

-

IRC §422(a)(2) generally limits post-termination ISO exercise to three months (longer disability death exceptions exist in statute)—late exercise can terminate ISO status and change payroll tax results. ↩

-

IRS Form 3921 Instructions — employer filing and employee copy timing. ↩

-

IRC §422(a)(2) — post-termination exercise window to preserve ISO status. ↩

-

IRS Publication 525 — AMT and stock compensation examples. ↩

-

IRC §422(a) — qualifying disposition holding periods. ↩