Executive Summary

How do I report RSU income on my tax return?

Your employer reports RSU vesting as ordinary wages on Form W-2 (Box 1, and typically Social Security/Medicare wages in Boxes 3 and 5). That amount carries to Form 1040 as wages—you do not enter RSUs again as separate income. When you sell the shares, report gain or loss on Form 8949 and Schedule D. Your basis is usually the FMV per share already taxed at vest; if Form 1099-B shows basis $0 or wrong basis, adjust on Form 8949 to avoid double taxation.

When RSUs vest, the fair market value of the shares on the vesting date is compensation income under IRC § 83(a). Most tech employees first see this as a large W-2 and a surprise tax obligation. The second pain point arrives at tax filing or when they sell: reconciling what was already taxed as wages with what brokers report to the IRS.

The bottom line: Think in two layers—(1) vesting = wages already on your return via W-2, and (2) sale = capital gain/loss only on the change in value after vesting, with basis tied to the vest FMV, not your $0 out-of-pocket.1

Critical Warning: If you accept Form 1099-B as-is when basis is blank or wrong, you can pay tax twice on the same economics—once as wages at vest and again as false capital gain on sale. Fixing this on Form 8949 is standard practice when you have documentation (vest statements, W-2 detail, employer confirmations).2

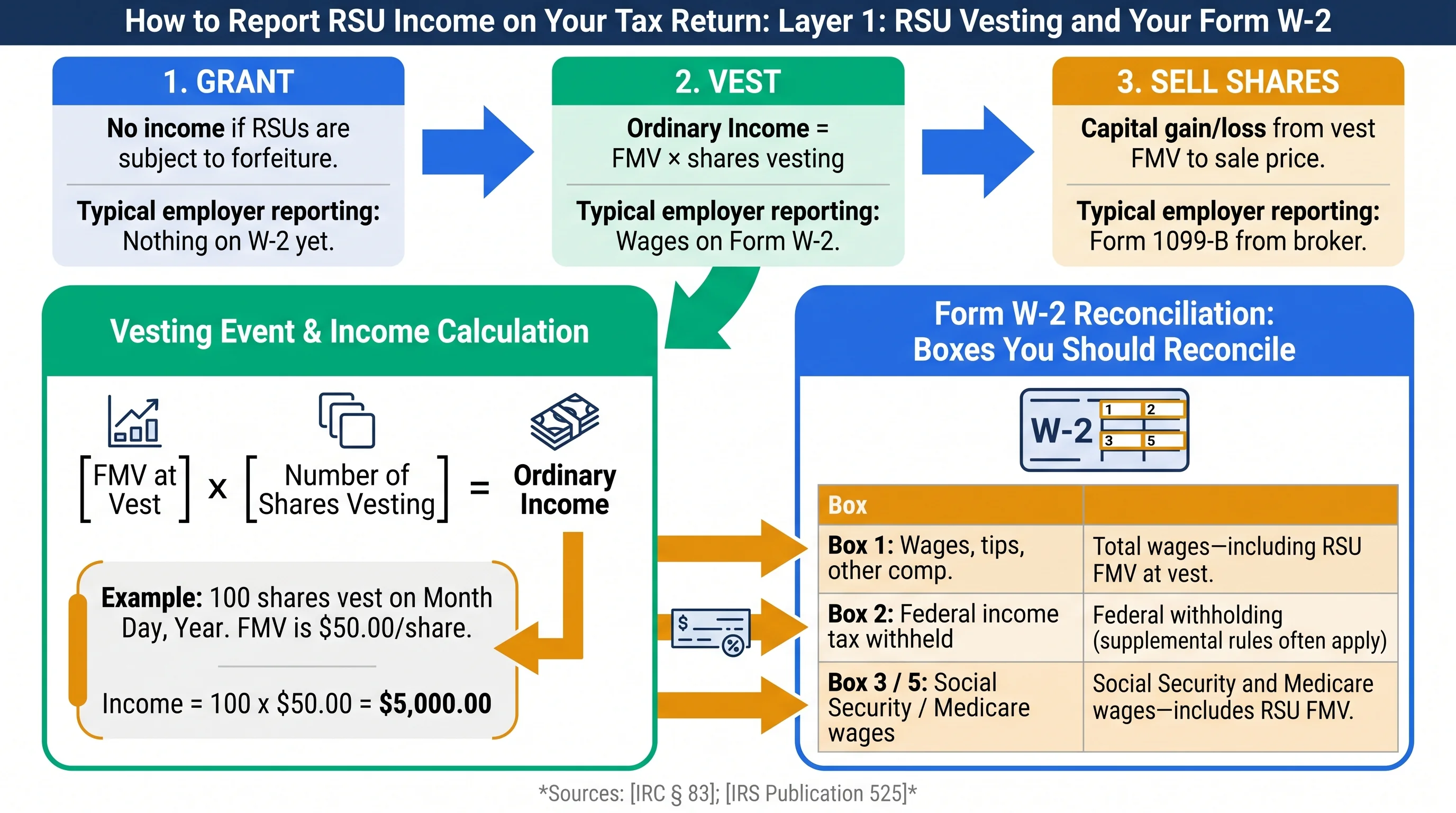

Layer 1: RSU Vesting and Your Form W-2

What Gets Taxed, and When

| Event | Regular tax treatment | Typical employer reporting |

|---|---|---|

| Grant | No income if RSUs are subject to forfeiture | Nothing on W-2 yet |

| Vest | Ordinary income = FMV × shares vesting | Wages on Form W-2 |

| Sell shares | Capital gain/loss from vest FMV to sale price | Form 1099-B from broker |

Sources: IRC § 83; IRS Publication 525

W-2 Boxes You Should Reconcile

| Box | What to verify for RSUs |

|---|---|

| 1 | Total wages—including RSU FMV at vest |

| 2 | Federal withholding (supplemental rules often apply) |

| 3 / 5 | Social Security and Medicare wages (RSU FMV included; Social Security only up to the annual wage base) |

| 14 | Some employers label RSU / equity details (optional; amounts still in Box 1) |

Source: Form W-2 Instructions

Why This Matters for Form 1040

Software imports W-2 wages into Form 1040, line 1a. There is generally no extra line for “RSU income” because it is already inside wages. If you manually duplicate vest FMV elsewhere (for example, as miscellaneous income), you will over-report.

Related reading: For withholding mechanics and why 22% often falls short, see RSU and Option Withholding: Why 22% May Not Be Enough. For the big-picture RSU rules, see the Comprehensive Tax Guide to RSUs.

Figure 1: RSU income path from vest (W-2 wages) to eventual sale (8949/D).

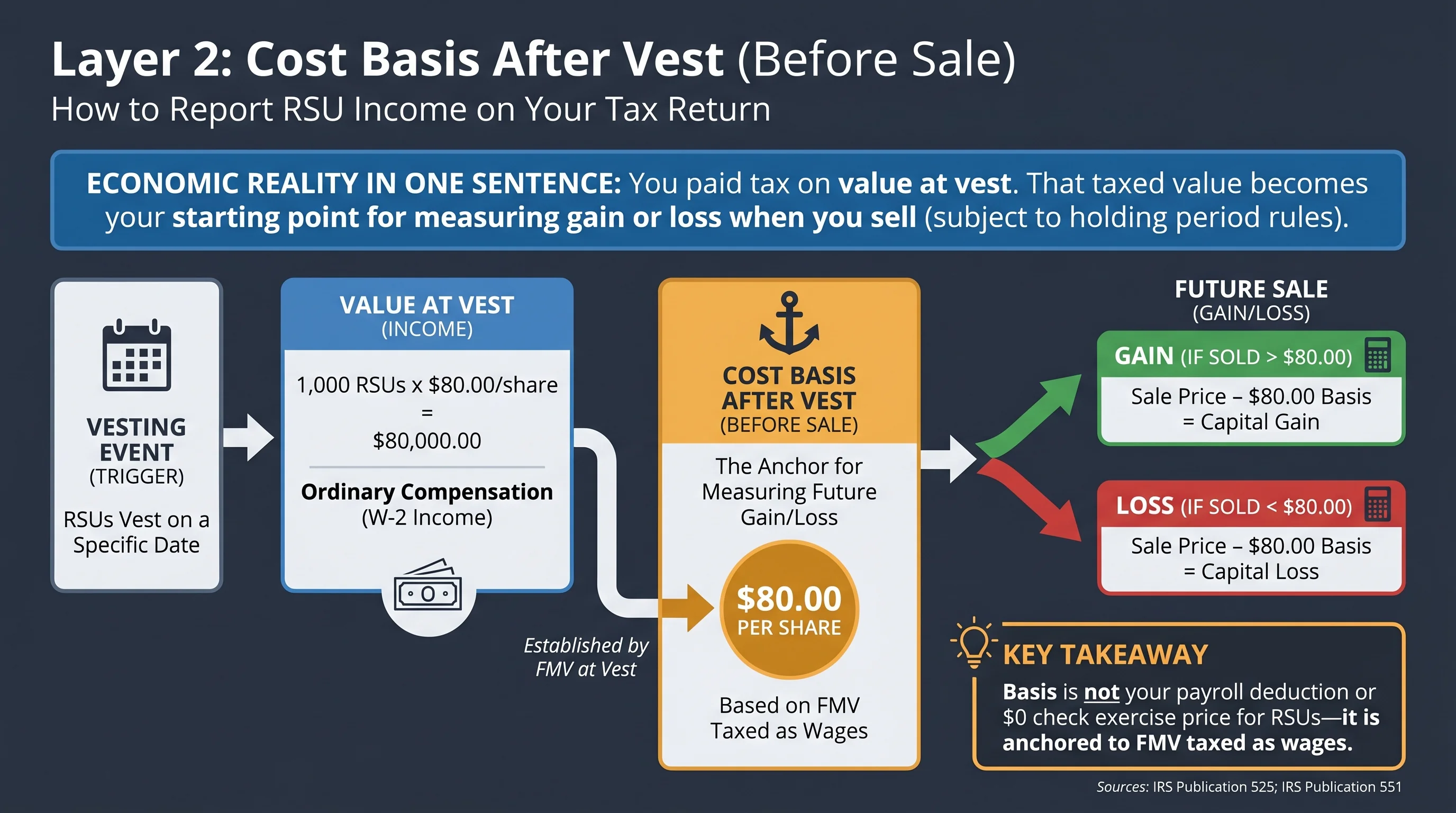

Layer 2: Cost Basis After Vest (Before Sale)

Economic Reality in One Sentence

You paid tax on value at vest. That taxed value becomes your starting point for measuring gain or loss when you sell (subject to holding period rules).

Per-Share Basis (Typical Case)

If 1,000 RSUs vest when the stock is $80/share, you have $80,000 of ordinary compensation (before any sell-to-cover mechanics). The $80/share figure is the common anchor for basis per share for those vested shares going forward (your employer or broker statements should agree).

Key takeaway: Basis is not your payroll deduction or $0 check exercise price for RSUs—it is anchored to FMV taxed as wages.

Sources: IRS Publication 525; IRS Publication 551

Sell-to-Cover and Net Shares

Many plans sell a portion of shares at vest to cover withholding. You still had gross income on the full vest; withholding is handled via shares sold or cash. Keep the confirmation statement—it shows gross shares, shares sold for taxes, and net deposited shares. You need this if broker basis looks wrong.

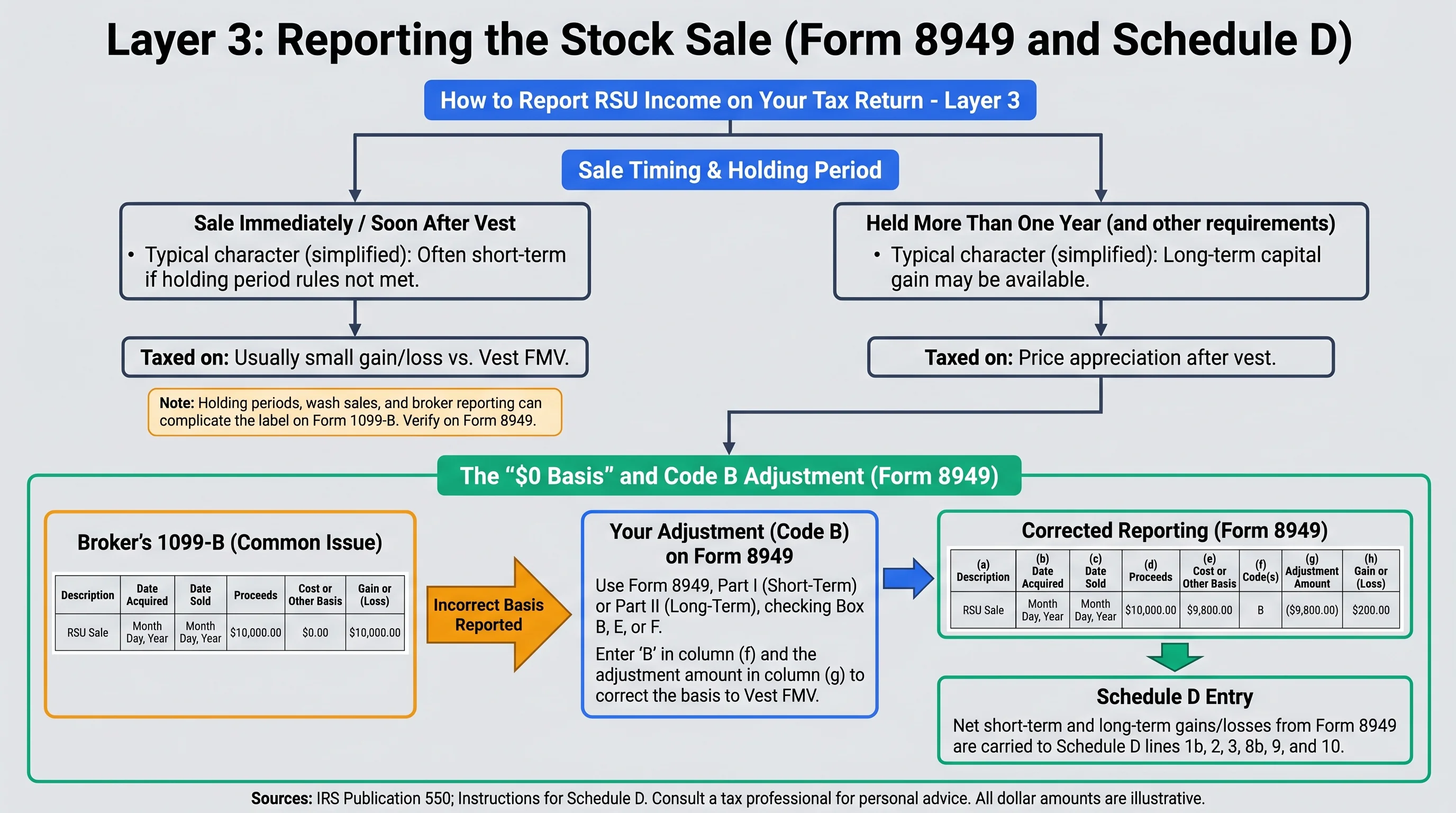

Layer 3: Reporting the Stock Sale (Form 8949 and Schedule D)

For column-level Form 8949 instructions (which Part/box, adjustment codes, holding period), use our dedicated How to Report RSU Sales on Form 8949 and Schedule D. The section below summarizes the economic story so the two guides work together.

What Happens If You Sell Immediately vs Later

| Sale timing vs vest | Typical character (simplified) | What you are taxed on at sale |

|---|---|---|

| Same day / soon after vest | Often short-term if holding period rules not met | Usually small gain/loss vs vest FMV |

| Held more than one year (and other requirements) | Long-term capital gain may be available | Price appreciation after vest |

Note: Holding periods, wash sales, and broker reporting can complicate the label on Form 1099-B. Verify on Form 8949.

Sources: IRS Publication 550; Instructions for Schedule D

The “$0 Basis” and Code B Adjustment Pattern

Brokers sometimes report proceeds correctly but cost basis as blank or $0 for RSU-linked sales. If you do nothing, tax software may compute a inflated gain.

Fix: On Form 8949, report the sale and adjust basis to match the compensation income you already recognized (per vest lot), with documentation. The Form 8949 instructions discuss correction of basis and appropriate codes depending on facts (common scenarios involve basis not reported to the IRS, or needing adjustment in column (g)).

Source: Instructions for Form 8949

Worked Example A — No Broker Basis, Full Vest Then Sale

- Vest: 500 shares @ $100 FMV → $50,000 in Box 1 (simplified).

- Later sale: all 500 shares @ $130/share → proceeds $65,000.

- Gain (before state/NII nuances): ($130 − $100) × 500 = $15,000 (often short-term if not held long enough).

If 1099-B shows $0 basis, your naive gain would show $65,000—$50,000 too high.

Worked Example B — Partial Lot, Two Vests

You vest 200 shares @ $40 in February and 200 shares @ $55 in August. Later you sell 300 shares for $75 each:

| Lot (FIFO assumed for illustration) | Basis/share | Shares sold | Basis used |

|---|---|---|---|

| Feb vest | $40 | 200 | $8,000 |

| Aug vest | $55 | 100 | $5,500 |

| Total basis | 300 | $13,500 |

Proceeds: 300 × $75 = $22,500.

Gain ≈ $9,000 (holding period rules still apply).

Best practice: Track lots (vest dates, share counts, FMV) in a spreadsheet; match employer confirmations to 1099-B.

If you use tax software, import forms first—then override only the 8949 basis cells backed by your vest evidence, so you do not lose automated consistency checks on dates and proceeds.

Figure 2: Avoiding double tax—vest FMV basis vs $0 basis error.

Withholding Shortfalls and Estimated Tax

Even with correct reporting, you can owe balance due if withholding on vesting was too low relative to your marginal rate (common when only 22% federal supplemental rate applied to a large vest). Estimated tax rules and Form W-4 adjustments are the usual fix.

| Issue | Symptom | Mitigation (high level) |

|---|---|---|

| 22% withholding vs 35% bracket | Large tax due on filing | Extra withholding, quarterly estimates per Form 1040-ES |

| Multiple cliffs / mega-vests | Underpayment even with “normal” settings | Model year in advance; use Publication 505 safe-harbor rules |

Sources: IRS Publication 505; Treasury regulations on supplemental wages

Related: Year-End Tax Planning for Equity Compensation.

How Supplemental Wage “Chunks” Interact With RSU Vests

If your employer uses optional flat-rate withholding on supplemental pay, a single large vest can still be under-withheld versus your annual effective rate—especially if you have two vest dates in one calendar year that each look “reasonable” in isolation but stack you into the top bracket on total income. Model cumulative income, not just one pay stub.

Net Investment Income Tax (NIIT) on Post-Vest Sales

After RSUs vest, any capital gain recognized on later sale may interact with the Net Investment Income Tax if your modified AGI exceeds statutory thresholds (single vs married filing jointly thresholds in the instructions). RSU wage income at vest is not “net investment income,” but capital gain on sale generally is for NIIT purposes. High earners can face federal ordinary bracket tax + 3.8% NIIT on investment income layers—another reason accurate basis matters (wrong basis inflates both capital gain and NIIT exposure on paper).

Sources: IRS Form 8960 Instructions; IRC § 1411

Wash Sales and RSU-Related Trades

If you harvest losses in other securities around the same period as RSU activity, wash sale rules can defer loss recognition. RSU vesting itself is not a market purchase, but the way you manage overlapping stock positions can still trigger wash-sale complexity on Schedule D. See our dedicated Wash Sale Rules and Equity Compensation guide when loss harvesting.

State Income Tax Reporting (Overview)

States generally tax RSU vesting as wages for residents. If you moved mid-year or worked in multiple states, sourcing rules can split vest income—this is beyond a simple filing walkthrough and often needs a multi-state CPA.

| Scenario | What often happens |

|---|---|

| Resident of high-tax state | RSU wages sourced to that state on W-2 / state return |

| Travel / temporary assignment | Employer may allocate; verify state wages on W-2 state copy |

| Remote multi-state | Complex—see Multi-State Remote Workers |

Common Mistakes (and How to Avoid Them)

| Mistake | Why it hurts | Fix |

|---|---|---|

| Duplicating RSU income beyond W-2 | Overstates tax | Remove extra “RSU” manual entries; trust wage import |

| Accepting 0 basis on 1099-B | Double taxation | Adjust on Form 8949 with vest documentation |

| Mixing ISO and RSU logic | Wrong AMT / basis story | RSUs are not ISOs—different forms; see Forms 3921/3922 overview |

| Ignoring supplemental wage stacking | Surprise balance due | Plan withholding/estimates early |

Figure 3: Practical filing checklist for RSU recipients.

Frequently Asked Questions

Do I enter RSU income separately on Form 1040?

Answer: Generally no. RSU vesting is included in wages on Form W-2 Box 1, which flows to Form 1040 wages. You only address RSUs again when reporting sales (8949/D) or special elections (rare).

Why does my 1099-B show $0 cost basis?

Answer: Brokers may not have employer vest data integrated; you supply correct basis using vest notices and payroll records. Correct on Form 8949.

Source: Form 8949 Instructions

Is my RSU gain taxed twice?

Answer: Not if you report correctly. You pay ordinary tax on vest FMV as wages, then capital gains tax only on appreciation after vest (if any). Double taxation is usually a reporting error, not the law.

What records should I keep?

Answer: Keep grant/vest statements, trade confirms, W-2, 1099-B, and a lot ledger at least through the statute of limitations and until positions are fully closed.

Source: IRC § 6001 (general recordkeeping expectation)

Does AMT apply to RSU vesting like ISO exercises?

Answer: Generally no in the same way as ISO AMT adjustment on exercise. RSU vesting is ordinary wage income already. ISO interactions are different—see AMT Planning for Stock Options.

What if my employer put RSUs in Box 14 only?

Answer: Box 14 is informational. Taxable wages must still be reflected in Box 1. If Box 1 looks too low versus vest FMV, resolve with payroll before filing.

Can I deduct broker fees against RSU gain?

Answer: Personal investment expenses are generally not deductible in the way employees expect; specifics depend on year and facts. Ask a professional.

I moved states the month I vested—who taxes me?

Answer: Possibly multiple states or specific allocation—get multi-state help; do not guess from a single W-2 line.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRS Publication 525 | IRS Publication | https://www.irs.gov/publications/p525 |

| IRS Publication 550 | IRS Publication | https://www.irs.gov/publications/p550 |

| Form W-2 Instructions | IRS Form Instructions | https://www.irs.gov/pub/irs-pdf/iw2w3.pdf |

| Instructions for Form 8949 | IRS Form Instructions | https://www.irs.gov/instructions/i8949 |

| IRC Section 83 | Statute | https://www.law.cornell.edu/uscode/text/26/83 |

Disclaimer: This guide discusses legal tax compliance and planning concepts only. Tax evasion is illegal. This content is educational and not individualized tax, legal, or financial advice. Rules change, and your facts (employer procedures, state residency, foreign reporting) may differ. Consult a qualified tax professional before filing or making elections.