Executive Summary

What is Form 3921 and why did I receive it after exercising ISOs?

IRS Form 3921 is an information return your company files when you exercise incentive stock options (ISOs) and receive stock. It reports the grant date, exercise date, exercise price per share, fair market value per share on the exercise date, and how many shares were transferred. You use it to track AMT adjustments when you exercise and hold, and to support correct basis and holding-period calculations when you eventually sell.

ISOs sit in a different tax universe than NSOs or RSUs. No ordinary wage income is generally recognized at exercise for a qualifying ISO—yet the IRS still wants the exercise facts on Form 3921 because alternative minimum tax and disqualifying dispositions can move large dollars across years.

The bottom line: Treat Form 3921 as your official exercise receipt—the numbers your return preparer (or you) will reconcile to Form 6251 (AMT), later Form 8949 sales, and sometimes Form 3921 audits of employer compliance.1

Critical Warning: The AMT preference item from exercising and holding can produce cash tax due even when your W-2 did not grow—model ISO exercises before you click “exercise” in the equity portal. See AMT Planning for Stock Options and our ISO AMT Impact Calculator.

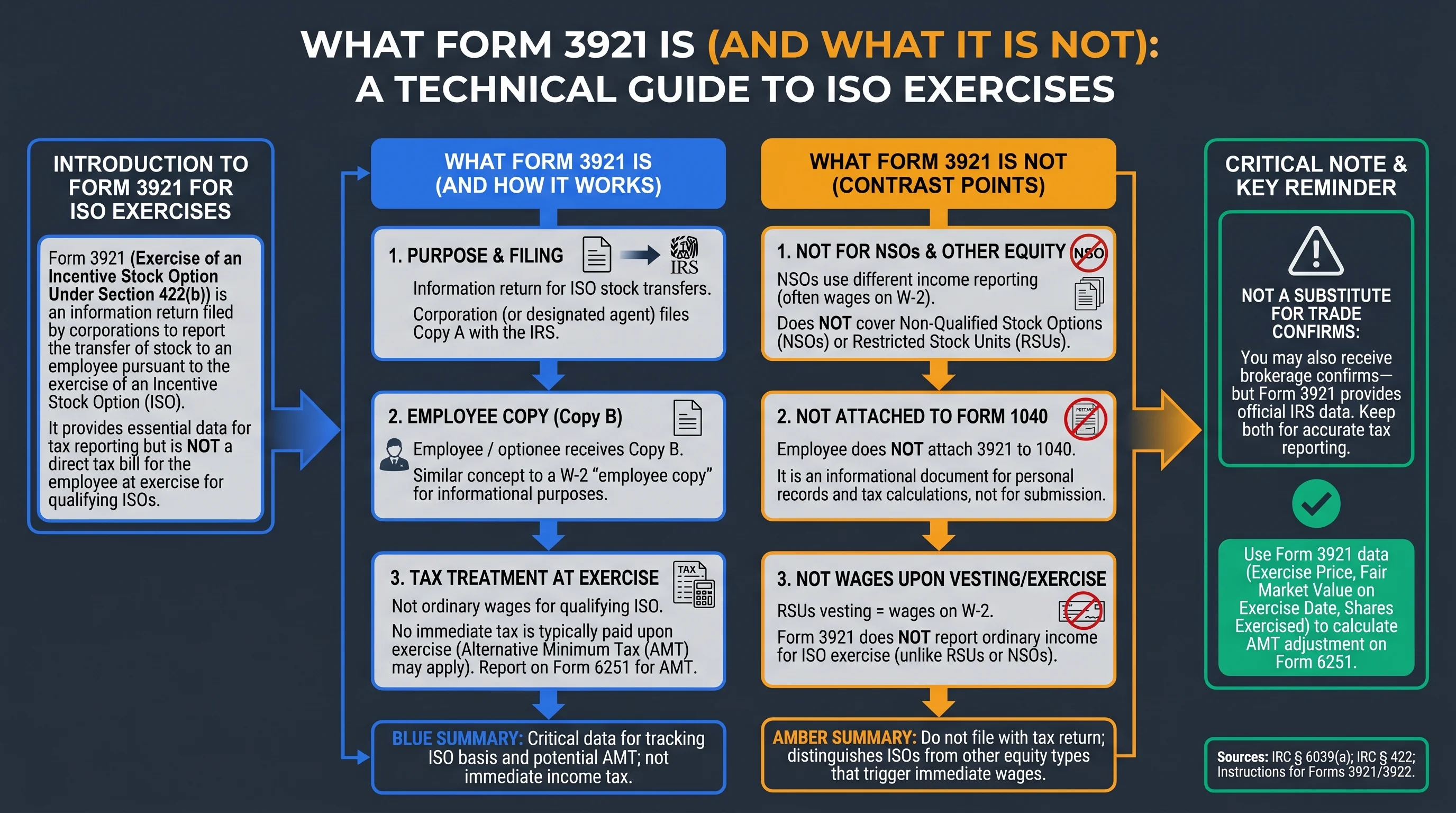

What Form 3921 Is (and What It Is Not)

| Topic | Form 3921 | Contrast |

|---|---|---|

| Purpose | Information return for ISO stock transfers | NSOs use different income reporting (often wages) |

| Who files with IRS | Corporation (or designated agent) | Employee does not attach 3921 to 1040 |

| Who receives Copy B | Employee / optionee | Similar concept to W-2 “employee copy” |

| Tax paid at exercise? | Not ordinary wages for qualifying ISO | RSUs vesting = wages on W-2 |

Sources: IRC § 6039(a); IRC § 422; Instructions for Forms 3921/3922

Not a substitute for trade confirms: You may also receive brokerage confirms—but for tax archeology, 3921 + your grant notice + 83(b) file (if any) are core.

Related hub: Equity Compensation Reporting: Forms 3921, 3922, W-2 Explained.

Figure 1: Who files Form 3921—and how employees use Copy B.

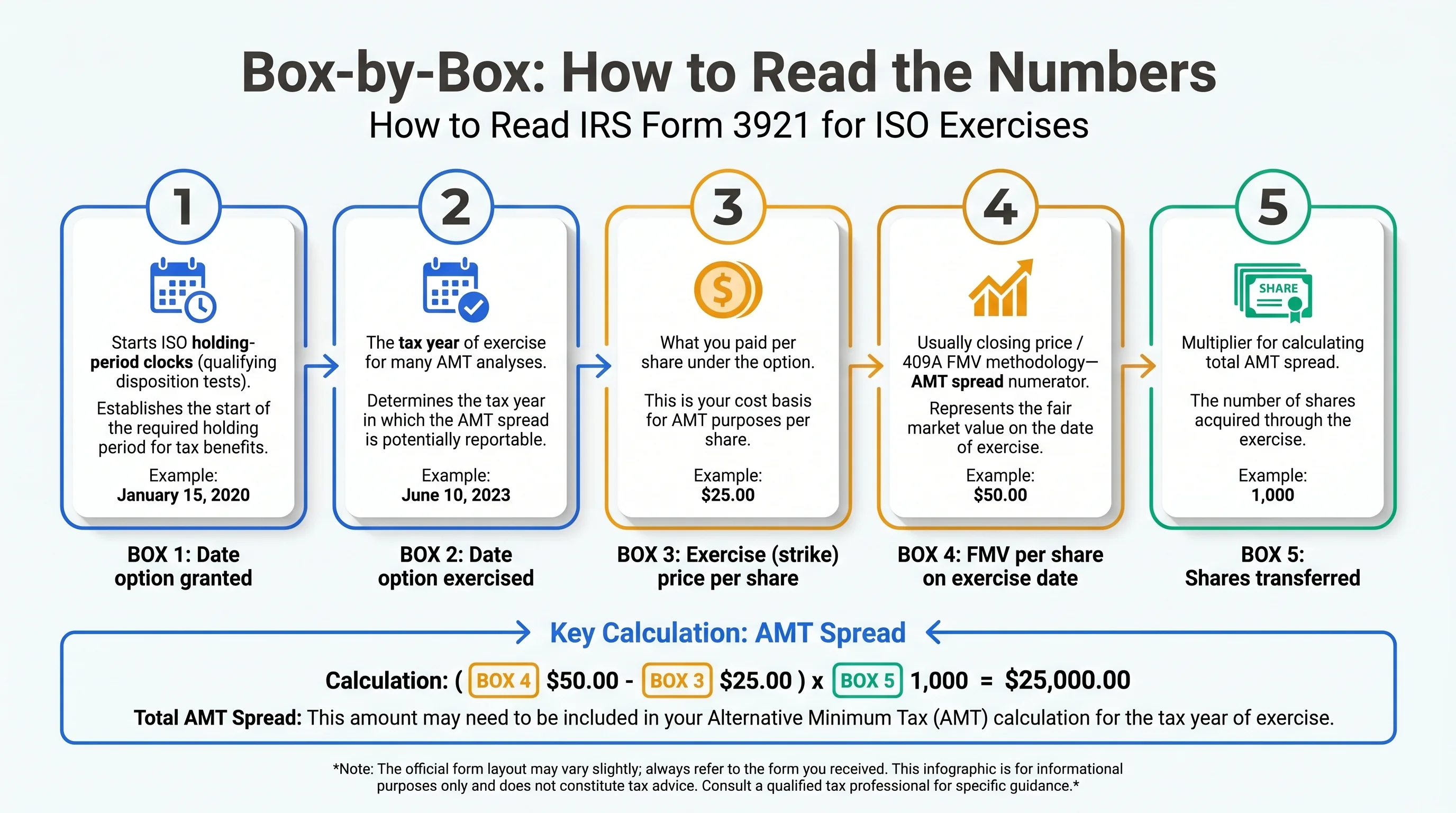

Box-by-Box: How to Read the Numbers

The current official form layout may use slightly different labels year to year; always tie to the form you actually received. The economic fields you need are almost always these five concepts:

| Box (typical layout) | Label (conceptual) | What it means for you |

|---|---|---|

| 1 | Date option granted | Starts ISO holding-period clocks (qualifying disposition tests) |

| 2 | Date option exercised | The tax year of exercise for many AMT analyses |

| 3 | Exercise (strike) price per share | What you paid per share under the option |

| 4 | FMV per share on exercise date | Usually closing price / 409A FMV methodology—AMT spread numerator |

| 5 | Shares transferred | Multiplier for totals |

Source: Form 3921 (PDF) and Instructions

Reading Box 1–2 Together (Grant vs Exercise)

Qualifying disposition (for ISO long-term capital gains treatment on some gain) generally requires holding > 2 years from grant and > 1 year from exercise—both dates appear on Form 3921. Compare to sale date before you assume long-term treatment.

Source: IRC § 422(a)

Reading Box 3–5 Together (The Spread)

Define (economic spread):

Bargain element ≈ (Box 4 - Box 3) * Box 5

Example:

Box 3 = $5/share, Box 4 = $45/share, Box 5 = 1,000 shares

Spread/share = $40 → Bargain element = $40,000

That $40,000 is not automatically “taxable wages”—but it may feed AMT when you exercise and hold (see next section).

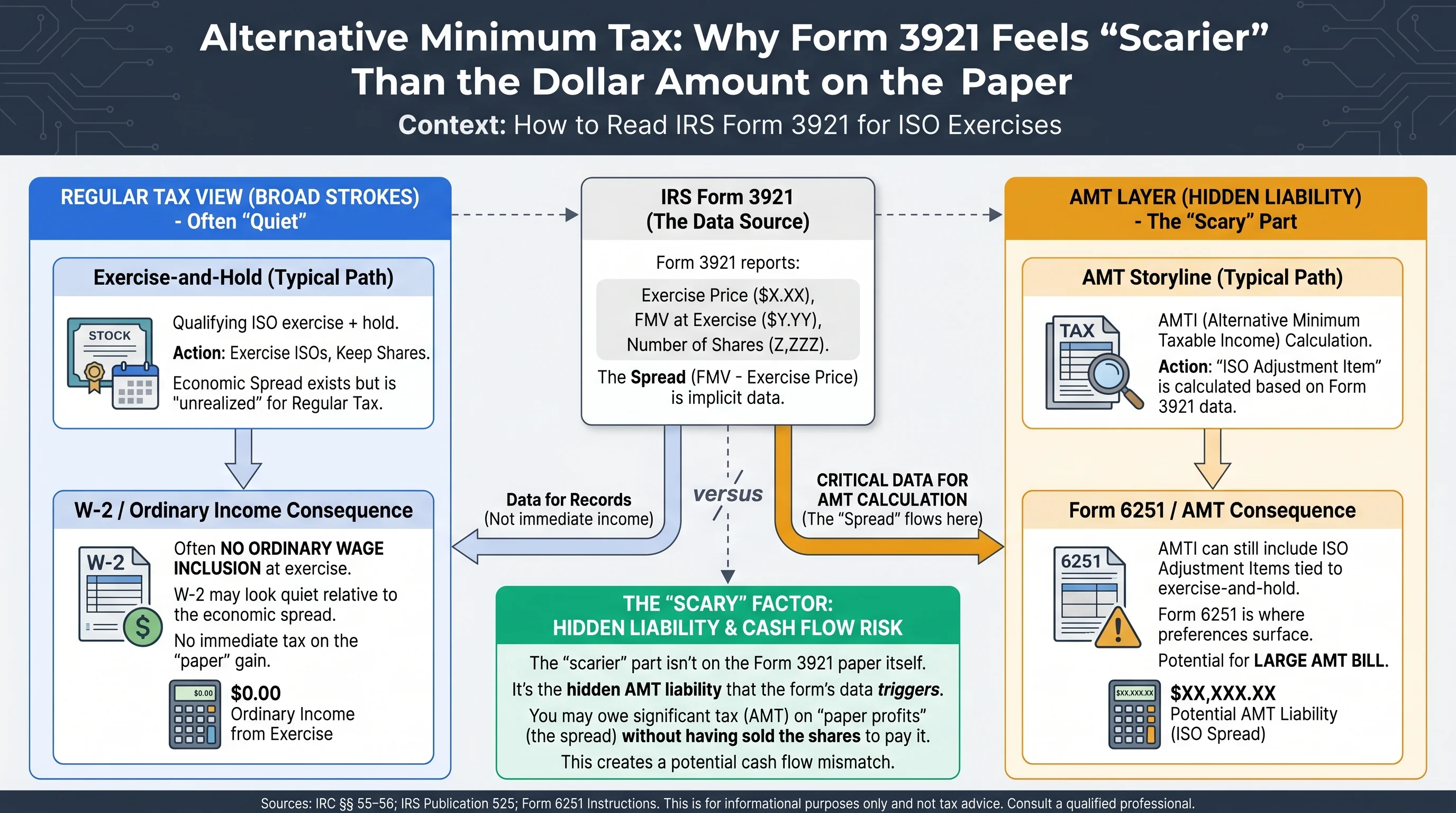

Alternative Minimum Tax: Why Form 3921 Feels “Scarier” Than the Dollar Amount on the Paper

| Regular tax (broad strokes) | AMT layer |

|---|---|

| Qualifying ISO exercise + hold often has no ordinary wage inclusion at exercise | AMTI can still include ISO adjustment items tied to exercise-and-hold |

| W-2 may look quiet relative to economic spread | Form 6251 is where preferences surface |

Sources: IRC §§ 55–56; IRS Publication 525; Form 6251 Instructions

Exercise-and-Hold vs Same-Day Sale

| Path | Ordinary income at exercise (typical) | AMT storyline (typical) |

|---|---|---|

| Exercise and hold | Often none for qualifying ISO | AMT adjustment often matters (publication examples; confirm forms for your year) |

| Same-day sale / disqualifier | Wages/compensation elements often appear (disqualifying disposition) | AMT story may differ—you are not in the “typical ISO exercise with no wages” mode |

This is why generic blog posts mislead—your broker path changes the tax character.

Related: ISO Qualifying vs Disqualifying Disposition.

Figure 2: From Form 3921 fields to the economic “spread.”

The ISO $100,000 Rule (Why Some “ISO” Exercises Are Not ISO for Tax)

IRC § 422(d) limits how much ISO can first become exercisable in a calendar year (valued at FMV as of grant). Excess may be treated as nonqualified options for tax—your payroll / equity team should track this, but you should notice if exercise packets mention NSO characterization for part of a grant.

If a portion failed ISO limits, do not blindly apply “no wage income at exercise” folklore—get a pro.

Deadlines and Penalties (Corporate Compliance—Employee Perspective)

You mainly care whether you received Copy B timely—because audits of your return may cross-check employer filings.

| Responsibility | Typical due date (calendar year exercises) |

|---|---|

| Furnish Copy B to employee | January 31 following the exercise year (next business day if weekend/holiday under IRC § 7503) |

| File with IRS (paper) | Often February 28 following the year (confirm instructions annually) |

| File with IRS (e-file) | Often March 31 following the year (confirm instructions annually) |

Penalties for late / incorrect information returns exist under IRC §§ 6721–6722—amounts escalate with intentional disregard. You rarely pay these—the corporation does—but missing statements delay your compliance.

Source: Instructions for Forms 3921 and 3922

From Exercise to Sale: Basis and Form 1099-B

When you eventually sell:

| Concept | Regular tax basis (simplified) | AMT basis (if relevant) |

|---|---|---|

| Starting point | Often exercise price paid plus ordinary income recognized along the way (if any) | AMT carryover rules can create dual basis tracking (“AMT basis vs regular basis”) |

Dual-basis tracking is infamous for ISO-heavy employees. Form 3921 is an anchor document, but complete history includes subsequent sales, prior disqualifiers, and prior AMT credit themes.

Related: ISO vs NSO: Tax Treatment Compared.

Practical Workflow: What to Do When the Mail (or Portal) Arrives

| Step | Action |

|---|---|

| 1 | PDF + print Copy B into your tax folder for the exercise year |

| 2 | Verify grant/exercise dates against equity portal |

| 3 | Compute spread sanity check (Boxes 3–5) vs broker FMV |

| 4 | Give to CPA with grant agreement and exercise election |

| 5 | When you sell, link to broker 1099-B / 8949 basis reconciliation |

Recordkeeping Duration

Keep ISO records through full disposition of shares and through any AMT credit recovery horizon your CPA discusses—many employees benefit from AMT credit carryforward analysis after AMT years.

Figure 3: Employee checklist after receiving Form 3921.

Worked Scenarios

Scenario A — Mid-Year Exercise, Hold Through December

- Grant 01/10/2022, exercise 07/01/2025, strike $8, FMV $48, 2,000 shares.

- Spread/share = $40 → $80,000 economic bargain element.

- Hold all shares through 12/31/2025 → AMT planning for 2025 return is the headline (exact line item mapping to Form 6251 follows instructions for that year).

Scenario B — Partial Exercise Ladder

You exercise 500 shares in March and 300 in June—two Forms 3921 (or consolidated reporting depending on payroll vendor). Track per-lot AMT and basis—do not merge mentally.

Scenario C — Disqualifying Same-Day Sale

Exercise and sell same day for $52 when FMV at exercise is $52 and strike $10—you are often not trying to model a multi-year AMT hold; compensation elements can dominate. 3921 still matters as the exercise fact pattern.

Scenario D — Public Company With Daily FMV Visibility

If your employer stock trades on an exchange, employees sometimes assume 3921 Box 4 must equal the last trade of the day. Corporate 409A and plan administrators may use a defined valuation method (for example, closing price on primary exchange on exercise date, or an average per plan terms). If your DIY FMV check differs slightly from Box 4 by pennies, that may still be acceptable; if it differs materially, open a ticket with stock admin and obtain the written method.

Employer Filing Logistics and Common Employee Follow-Ups

Why the IRS Cross-Checks These Information Returns

Third-party statements like Form 3921 help the IRS reconcile corporate-reported ISO exercises to individual AMT and disposition reporting. That does not mean every employee receives an audit if Copy B is a week late—but persistent material FMV discrepancies relative to public prices can invite questions. Treat employer errors like W-2 errors: escalate quickly and document corrections.

Corporate Filings, TCC, and FIRE (Why Startups Sometimes Miss January)

Many employers use payroll vendors or IRS FIRE-compatible e-file providers for Copy A batches. If your company is late, employees still must estimate AMT facts from broker/exercise statements for timely payments; you cannot wait forever on Copy B. Conversely, if Copy B arrives wrong (wrong FMV, wrong grant date), escalate to stock admin early—corrected forms exist, and your CPA may need an amended employer statement trail.

ISO “Spread” vs What Brokers Show in the App

Your equity portal may display per-share spread or total gain graphs that are not labeled for AMT vs regular tax. Form 3921’s FMV should match the board/409A methodology the company used on the exercise date—not necessarily the price you saw for one second in extended hours. Ask for the official closing price / valuation memo if Copy B FMV looks off versus your trade confirm.

How Form 3921 Interacts With Form 3922 in the Same Year

Some employees trigger both ISO exercises (3921) and ESPP transfers (3922) in one calendar year. Keep them separate in folders—they answer different IRC questions and feed different sale-basis logic later.

Some planners pair Form 3921 modeling with a cash needs worksheet: the form tells you the spread; your bank account tells you whether you can pay AMT and quarterly estimates without a forced sale. If those two stories diverge, adjust the exercise plan before settlement—not after December bonuses land.

Frequently Asked Questions

Do I attach Form 3921 to my Form 1040?

Answer: No attachment is standard—you retain Copy B and use the data on Form 6251 / related lines as required. Follow your tax software interview.

Why doesn’t my Form 3921 match my brokerage 1099-B?

Answer: They report different events—3921 is exercise transfer; 1099-B is sale. Timing and basis rules differ.

I lost Copy B—what now?

Answer: Request a duplicate from employer/payroll; also use grant/exercise statements as secondary evidence.

Does Form 3921 prove my cost basis?

Answer: It is strong evidence of exercise price and FMV at exercise—but full basis may require other adjustments (disqualifying events, fees, corporate actions).

Are ESPP purchases on Form 3921?

Answer: No—Form 3922 is the ESPP transfer statement (different form family).

Source: Instructions for Forms 3921 and 3922

What if I’m a nonresident alien?

Answer: Exceptions can apply—employers sometimes do not issue certain U.S. wage statements; confirm treaty and payroll facts. Do not assume U.S. ISO rules mirror your home country.

My company was acquired—who sends Form 3921?

Answer: Often the successor corporation or payroll agent—watch for vendor changes post-merger.

Could one exercise generate more than one Form 3921?

Answer: Possible depending on how payroll splits transfers—reconcile total shares to your broker statement.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| Instructions for Forms 3921 and 3922 | IRS | https://www.irs.gov/instructions/i3921 |

| Form 3921 (PDF) | IRS | https://www.irs.gov/pub/irs-pdf/f3921.pdf |

| IRC § 422 | Statute | https://www.law.cornell.edu/uscode/text/26/422 |

| IRC § 6039 | Statute | https://www.law.cornell.edu/uscode/text/26/6039 |

| Form 6251 Instructions | IRS | https://www.irs.gov/instructions/i6251 |

Disclaimer: This guide discusses compliance and educational tax concepts only. ISO taxation—including AMT, disposition, and corporate actions—is fact-specific. Consult a qualified tax advisor before exercising, selling, or filing.

Footnotes

-

IRC § 6039 reporting overlay on ISO exercises; Form 3921 instructions for employee use of Copy B. ↩