Executive Summary

If you landed here from a search like "IRS Publication 525 restricted stock units vesting wages," you are not looking for a vague essay on equity—you want the sentence-level bridge between IRS plain-language guidance and the payroll document you actually receive. Publication 525 is intentionally broad: it walks through what counts as taxable income versus statutory exclusions, and it repeatedly reinforces that employee compensation takes many forms beyond cash—stock delivered at vest is still compensation for services in the typical RSU design.1

This guide pairs that framework with the statutory backbone employers rely on—IRC §83—and the operational details you see on Form W-2, sell-to-cover statements, and brokerage 1099-B downloads. It is meant to complement (not replace) our comprehensive RSU tax guide and the focused RSU sell-to-cover explainer.

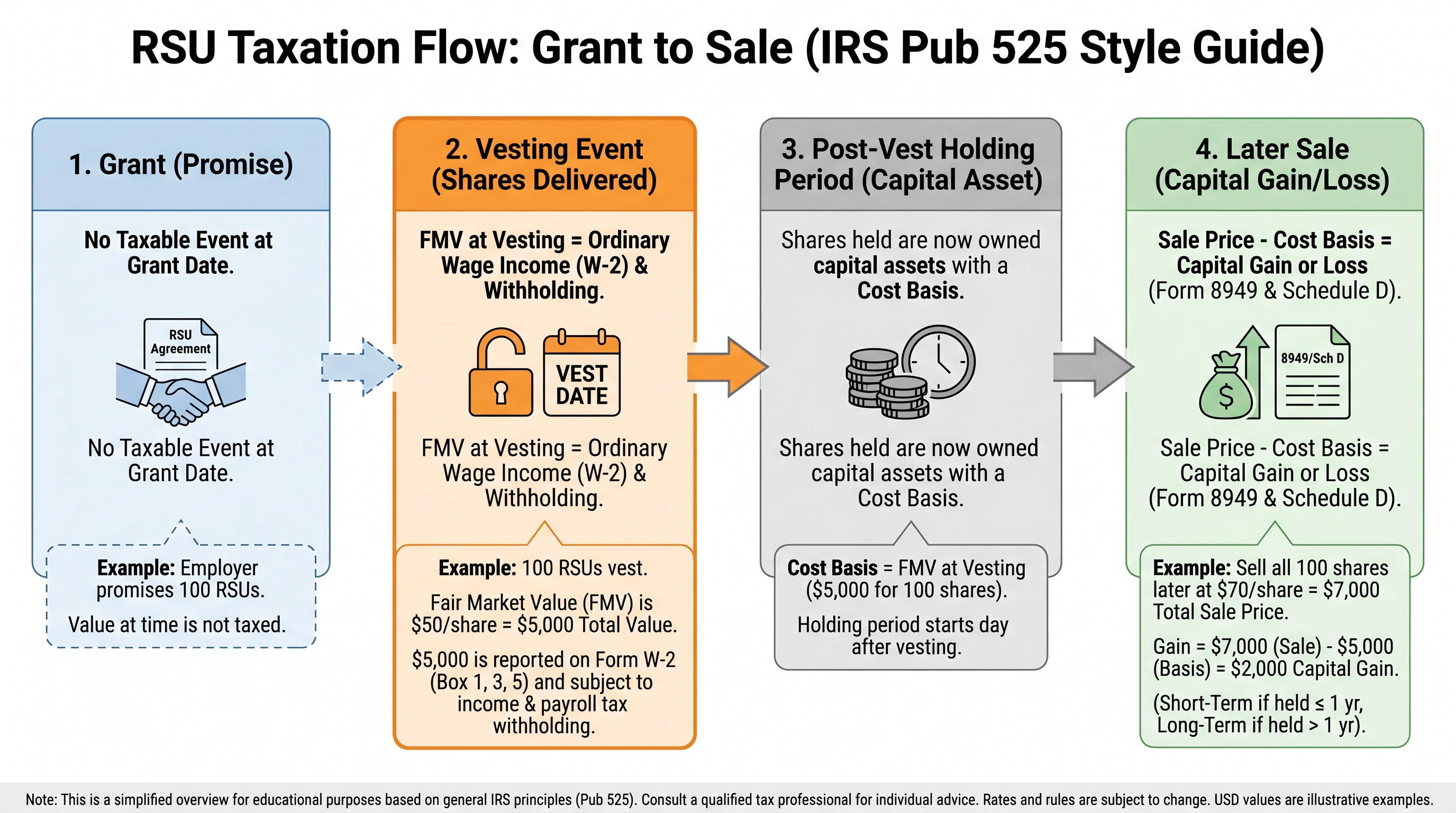

The bottom line: Treat RSU vesting like a paycheck denominated in shares: ordinary income at vest, payroll withholding, then a reset holding clock for capital gains only after you own the stock.2

Critical Warning: Withholding is not the same as your annual tax. If your employer uses supplemental wage flat rates, you can still owe more at filing when your marginal bracket is higher—see why 22% withholding may not be enough.

How Publication 525 Fits RSUs

Publication 525 is structured as a catalog of income types—wages, interest, dividends, business income, rent, and so on—with cross-references to other IRS publications where detail lives (for example Pub. 550 for investment income). RSUs are not always named on a single bullet labeled "RSU," but the compensation chapter is where employees should mentally file the plan: RSUs are pay for services, mediated through equity.

| Idea from Publication 525 | RSU angle | Practical artifact |

|---|---|---|

| Broad inclusion of income | RSU payout is rarely an excluded gift | W-2 Box 1 |

| Wages include non-cash pay | FMV of shares is still wages | Vest confirmation |

| Later investment income is separate | Post-vest sales can produce capital gain | 1099-B |

Publication 525 therefore answers the "is this taxable?" anxiety with a default yes for service-based equity, then points you to how employers report and withhold. For the opposite angle—capital markets math after you already own shares—use our capital gains overview.

Why search queries keep naming Publication 525

Employees trust primary IRS literature. When Google surfaces Publication 525 next to RSU queries, people want confirmation that vesting is wages. Publication 525 supplies that philosophical backbone, even though your payroll team leans on IRC §83 and Treasury Regulations for literal timing language.3

IRC §83 and the Vesting Trigger

IRC §83 governs property transferred in connection with the performance of services. While a full treatise belongs in a treatise, employees need three hinges:

- Transfer — When shares (or cash) are actually in your hands subject to tax rules, not merely a promise on a ledger.

- Substantial risk of forfeiture — Conditions that keep value at risk until vest; when they lapse, taxation usually accelerates for classic RSUs.

- Amount included — Generally FMV minus anything you paid, measured at the tax recognition event.

Conceptual wage inclusion per share ≈ FMV at inclusion event − amount paid (often $0 for RSUs)

For planning cliffs, refresher grants, and double triggers, our vesting schedule guide ties schedule vocabulary to tax moments.

| Concept | Plain English | RSU typical pattern |

|---|---|---|

| Grant | Contractual promise | Usually no shares, often no §83 inclusion yet |

| Vest | Conditions met | Ordinary income recognition for many plans |

| Settlement | Shares arrive at broker | Where FMV is often fixed for payroll |

RSUs vs. Restricted Stock and §83(b)

Publication 525 sits alongside guidance about many equity flavors. Employees routinely confuse RSUs with restricted stock awards. RSAs can sometimes pair with a Section 83(b) election filed within 30 days of an actual share transfer. Classic RSUs usually lack a transferable security at grant, so the election story differs materially.

Read RSA taxation and why 83(b) does not apply to typical RSUs before attempting DIY election filings—getting this wrong can be expensive.

| Feature | Typical RSU | Restricted stock (RSA) |

|---|---|---|

| Property at grant | Usually none | Often yes, but forfeitable |

| §83(b) available? | Generally no | Sometimes yes |

| Income timing | Vest / settlement | Vest unless §83(b) |

Form W-2, FICA, and Box Logic

Employers include RSU income as wages for income tax and payroll taxes, subject to caps and additional Medicare rules. Box 1 aggregates wages; Box 5 Medicare wages often track the same equity additions; state boxes vary.4

If you relocate mid-year, multi-state remote work can change sourcing even when payroll uses one corporate employer of record.

Supplemental Wages and the 22% / 37% Story

Many companies run RSU vest events off-cycle and withhold using Publication 15-T supplemental wage methods—22% federal on the segregated payment below the $1 million cumulative threshold in many cases, jumping to 37% on portions above that threshold in the calendar year for certain employers.5 Those are withholding artifacts, not promises that your annual Form 1040 ends neutral.

Worked example: 80 shares vest at $95 FMV → $7,600 wages. Federal income tax withheld at 22% → $1,672 (illustrative only). FICA (6.2% + 1.45% on applicable amounts) stacks on top until wage bases cap. If your marginal federal rate is 32%, you may still owe $760 of federal tax on that slice at filing before credits—exact numbers depend on your full return.6

Sell-to-Cover, Net Settlement, and Share Count Math

Most public employers sell a portion of vested shares at vest to fund withholding. Our sell-to-cover guide walks through rounding and why your net shares differ from gross vest. Publication 525 does not replace that operational detail—it explains why there was taxable income in the first place.

Brokerage Basis, Form 1099-B, and Double Tax Fears

After vesting, your cost basis for future sales usually equals the FMV taxed as wages (plus purchase price if any). Form 1099-B may be wrong if legacy broker data omits the wage step—your Form 8949 adjustment is how you avoid paying capital gains tax twice on the same spread. If you fear exactly that scenario, read are RSUs taxed twice?—the short answer is "not if basis is right."

Reading Publication 525 Next to Your Actual Tax Return

Publication 525 is best understood as the map, while your Forms W-2, 1099-B, and 8949 are the terrain. Walk the bridge in this order:

- Identify the vest or settlement date on your employer equity statement (sometimes labeled release or settlement).

- Find the FMV per share the employer used for payroll—this is the number embedded in your W-2 wages, not necessarily the opening or closing price you see on a chart.

- Multiply shares × FMV to reconcile to the delta in Box 1 across vest events (rounding and multiple tranches make penny-perfect checks rare).

- On the eventual 1099-B, confirm cost basis reflects that wage inclusion; if not, adjust on Form 8949 with the IRS basis codes your software expects.

State income tax follows the same wage inclusion in most cases, but residency moves can reallocate sourcing—see state tax nexus for remote workers when your family or employer footprint changes mid-year.

AMT orientation (RSUs vs. ISOs)

Employees juggling RSUs and incentive stock options sometimes worry that every equity line on a W-2 drags them into alternative minimum tax complexity. In practice, typical RSU vesting generates ordinary wages under the rules discussed above—not the ISO-specific AMT adjustment at exercise that drives AMT planning for stock options. Publication 525 still matters because it reinforces that wages are wages: RSU income increases adjusted gross income, which can indirectly affect credits, phase-outs, and the room you have for other tax planning. If you hold both RSUs and ISOs, model them on separate tabs of the same spreadsheet so you do not import exercise bargain elements into RSU basis tracking.

When change-of-control clauses accelerate RSUs, the taxable moment still tracks facts on the ground—when restrictions lapse and shares become yours. M&A teams may settle in cash versus shares, which changes your securities law and tax profile but not the core wage characterization for many employees.

Pair this section with what happens in M&A if a transaction is imminent.

Frequently Asked Questions

Does Publication 525 list my exact RSU dollar amount?

Answer: No—your employer systems compute FMV per vest. Publication 525 tells you the character of income (wages vs. excluded windfalls), not your personal amounts.

Source: IRS Publication 525

Is RSU vesting the same as a stock sale?

Answer: No. Vesting creates ordinary wage income. A later sale is a disposition of stock with separate gain/loss rules.

Source: IRC §83

Why is my W-2 bigger than my salary?

Answer: Equity wage lines stack on top of cash salary in Box 1 when shares vest.

Source: IRS Publication 525

Can I file §83(b) on RSUs to accelerate tax?

Answer: Usually no for classic RSU structures—see dedicated 83(b) / RSU article.

Source: Treasury Regulation §1.83-2

Does the 22% withheld cover my taxes?

Answer: Maybe not. Compare withholding to your marginal bracket and use estimated tax planning if you have repeated gaps.

Source: IRS Publication 15-T

What if I relocate internationally after grant?

Answer: Sourcing and treaty rules dominate; start with international planning before assuming U.S. wage treatment forever.

Source: IRS international guidance index

Where do RSUs meet Pub. 525 examples about stock?

Answer: Publication 525 crosswalks you to the IRS mental model—compensation first—then you apply §83 mechanics from regulations and employer reporting.

Source: About Publication 525

Which calculator helps model vest withholding?

Answer: Try the RSU tax estimator alongside your payroll department's official model.

Source: VestingStrategy tools index

Does NIIT apply after RSU vesting income?

Answer: Net investment income tax under IRC §1411 generally matters when you have net investment income—often interest, dividends, rent, and capital gains on sold stocks—not the RSU wage inclusion itself. Large RSU wages can push modified adjusted gross income over the thresholds, making investment gains elsewhere subject to the surtax. Coordinate with NIIT and equity if your return spans wages plus sizable portfolio sales.

Source: IRS — Topic 559

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| Publication 525 | IRS | irs.gov |

| About Publication 525 | IRS | irs.gov |

| IRC §83 | Statute | law.cornell.edu |

| Publication 15-T | IRS | irs.gov |

Figure 1: How Publication 525’s wage framing connects to IRC §83 timing, payroll reporting, and later capital gain math.

Disclaimer: This article discusses general U.S. federal tax principles only and is not personalized advice. Employer plans, state taxes, and non-U.S. aspects can change results. Confirm facts with the IRS publications cited and a qualified tax professional.

Research note: The content angle was selected from VestingStrategy's Chief Content Officer (CCO) API (npm run cco:recommend). Perplexity Sonar produced structured notes saved at docs/research/RESEARCH-CCO-IRS-PUBLICATION-525-RSU-VESTING-WAGES-EXPLAINED-PERPLEXITY-BRUT.md. Final editorial structure targets the MDX checklist used across content/guides/.

Footnotes

-

IRS, Publication 525, Taxable and Nontaxable Income—general framework for wages and compensation. irs.gov/publications/p525 ↩

-

Wage inclusion timing is plan-specific; default analysis assumes ordinary income at vest/settlement for service-based RSUs under §83. ↩

-

Statutory fine print lives in IRC §83 and regulations—Publication 525 orients taxpayers without replacing statute. ↩

-

Compare Medicare surtax rules for high earners in IRS Pub. 17 contexts; RSU wages count in the earnings base that drives additional Medicare. ↩

-

Supplemental wage rules summarized in IRS Publication 15-T—employers choose among permitted methods. ↩

-

Illustration only; run your full Form 1040 projection with a CPA or enrolled agent. ↩