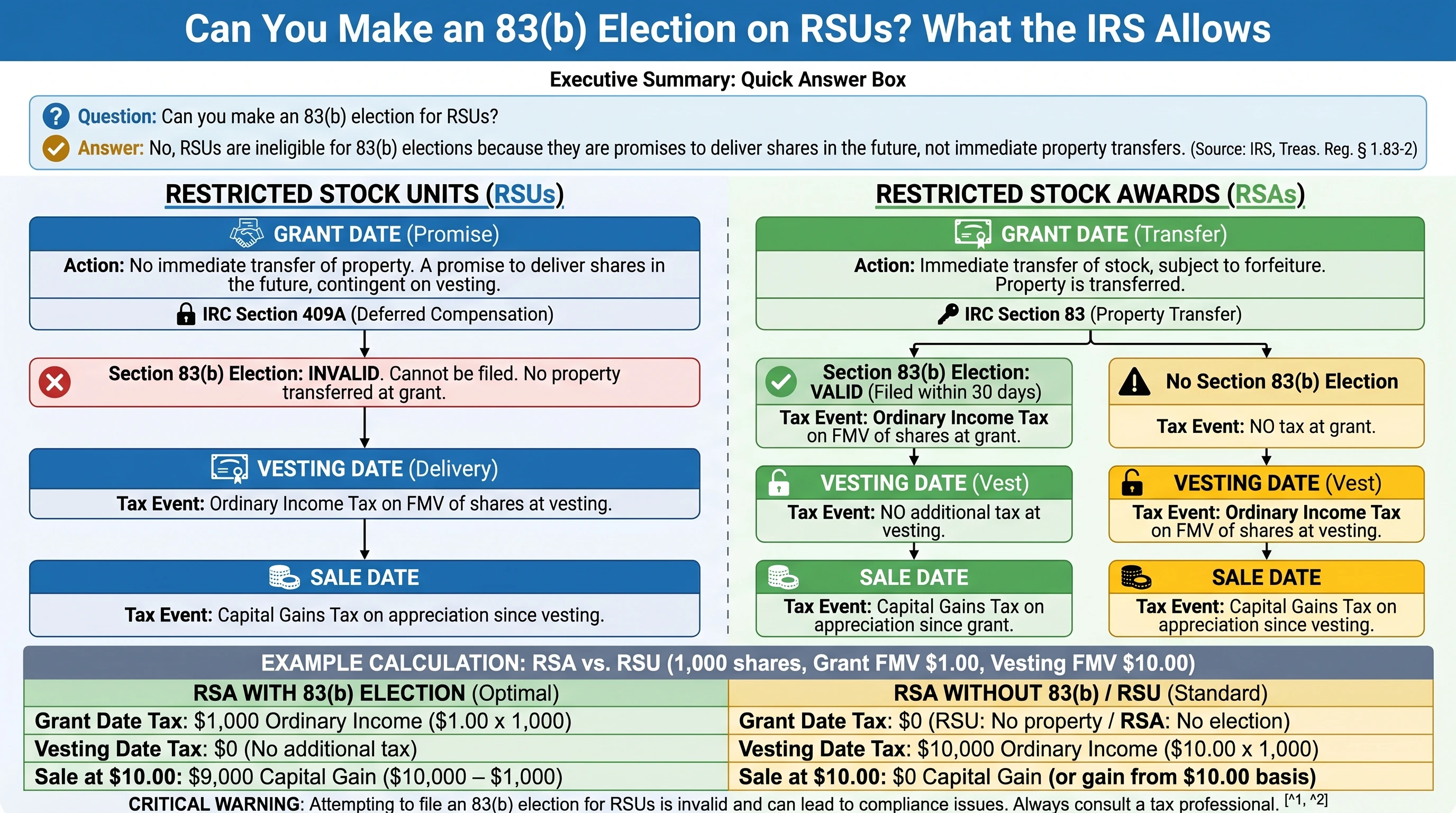

Executive Summary

Why can’t I file an 83(b) election on my standard RSUs?

Because a Section 83(b) election attaches to forfeitable stock (or similar property) transferred to you under IRC §83—with income inclusion at transfer if you properly elect—not to the typical RSU fact pattern where actual shares are delivered later (often at vest or settlement). With no qualifying transfer at grant, there is usually nothing to elect on in the way counsel means when they say “file an 83(b).”

If you searched “RSU 83(b) election” or “IRS 83(b) election restricted stock 30 days,” you are bumping into a definitions problem: Section 83(b) is about electing to include the value of transferred restricted property in income early, while many RSUs are structured as deferred delivery of stock or cash. That is not a loophole against RSUs—it reflects different transfer timing and payroll tax mechanics than restricted stock awards (RSAs) or early exercise of options.

The bottom line: Do not assume your RSU grant secretly supports an 83(b). Confirm—in your grant, plan, and confirmation notices—whether you received actual shares subject to forfeiture at a defined transfer date; if not, plan around vesting income, withholding, and the alternative strategies linked below—not a misplaced 83(b) filing.1

Planning tools on this site: If your fact pattern is restricted stock or early exercise, model economics with the 83(b) break-even calculator and early exercise break-even tools; for RSU cash flow at vest, use the RSU tax estimator.

Legal Framework and Distinctions

Understanding RSUs and RSAs

Restricted Stock Units (RSUs) and Restricted Stock Awards (RSAs) are both common in tech, but the transfer timing is different. Most RSUs are structured as a contractual promise to deliver stock (or cash) only after vesting or another settlement event—so you may have no shares to “elect on” at grant. Plans must still be designed to comply with Section 409A rules for deferred compensation where applicable. RSAs, by contrast, often issue shares up front subject to forfeiture, which is the classic IRC Section 83 fact pattern where an 83(b) may be discussed with counsel.

Section 83(b) Election

When it applies, Section 83(b) lets you voluntarily include transferred forfeitable property in income near the grant/transfer, instead of deferring wages treatment until vesting under §83(a)—changing the economics of later appreciation versus forfeiture risk. That pattern lines up cleanly with RSAs or early-exercised option shares transferred to you and still subject to repurchase—not with the archetypal placeholder RSU.

Important: Sending an 83(b) package for awards that never transferred restricted shares to you at grant rarely creates a coherent federal income-tax election (and may create confusion if payroll and your return disagree). Align paperwork with counsel and employer stock administration using your actual facts.2

Treasury Regulation and IRS Guidance

According to Treasury Regulation 1.83-2, an 83(b) election must be filed within 30 days of the property transfer. For many RSAs, that clock starts when unrestricted or restricted stock is actually transferred to you. For a classic RSU, there is often no transfer of shares at grant, which leaves no parallel event to pair with an 83(b) in the way people mean when they say “tax it early at low FMV.” IRS Publication 525 and employer plan language routinely distinguish RSUs at settlement from restricted stock—see also our Publication 525 and RSUs explainer.

Example Calculation: RSA vs. RSU

Consider an employee who receives 1,000 RSAs at a grant date fair market value (FMV) of $1 per share. If they file an 83(b) election, they recognize $1,000 as ordinary income immediately. If the stock appreciates to $10 per share by the vesting date, the $9,000 gain is treated as a capital gain.

**With 83(b) Election:**

- Grant Date: $1,000 ordinary income

- Vesting Date: No additional tax

- Sale: $9,000 capital gain

**Without 83(b) Election:**

- Grant Date: No tax

- Vesting Date: $10,000 ordinary income

- Sale: Capital gains on appreciation beyond $10/share

In contrast, RSUs are taxed at vesting based on the FMV at that time, resulting in $10,000 of ordinary income if the stock is worth $10 per share at vesting.

Why RSUs rarely support an 83(b) “property transfer” story

Section 83 generally looks for transfer of property to the service provider subject to substantial risk of forfeiture. Many RSUs describe a future issuance contingent on vesting—you often do not hold shares until settlement. With nothing to mark-to-market at grant, there is usually no 83(b) hook the way there is for RSAs or early-exercised options (see our how to file a Section 83(b) within 30 days checklist).

This is also why “can I 83(b) my RSUs?” is a different question than “should I 83(b) my RSA?” If you need the RSU mechanics end-to-end, read the comprehensive RSU tax guide first, then return here for the narrow ineligibility issue.

Does the IRS Pub. 525 ‘restricted stock’ wording make my RSUs eligible?

Publication 525 summarizes how restricted property and RSU-style income are reported—it does not rewrite your plan. If your employer never transferred shares to your brokerage at grant, Publication 525 alone will not create an 83(b) fact pattern; you still verify property transfer dates and award type with equity admin and counsel.

Visual primer: RSAs can align a Section 83 timeline with a tangible share transfer, while classic RSUs normally tax at delivery—educational only, not individualized tax advice.

Filing Requirements and Deadlines

Form 15620 and Filing Process

The IRS publishes Form 15620 as an optional format for making 83(b) elections. The filing is still subject to Treasury Regulation §1.83-2, including the 30-calendar-day window measured from the qualifying transfer of property. The form collects the facts the regulations require—your name, description of the shares, transfer date, FMV, amount paid, restriction summary, and required statements about copies.

Filing Steps

- Mail the Original Form: Send the completed Form 15620 to the IRS service center corresponding to your tax filing location.

- Provide a Copy to the Employer: Deliver a copy of the form to your employer on the same day.

- Retain a Copy for Records: Keep a copy of the form for personal recordkeeping.

Important Note: The 30-day filing deadline is strict, with no extensions or exceptions. Missing this deadline means forfeiting the ability to make the election.

Example Calculation: Missed 83(b) Election

Assume an employee receives 5,000 RSAs at a $0.50 FMV per share but misses the 30-day deadline for filing an 83(b) election. If the stock appreciates to $5 per share by vesting, they will recognize $25,000 as ordinary income at vesting, compared to $2,500 if they had filed the election.

**Missed 83(b) Election:**

- Vesting Date: $25,000 ordinary income

- Tax Rate: 37% (federal) = $9,250 tax liability

Tax Implications for RSU Holders

Taxation at Vesting

RSUs are taxed as ordinary income at the time of vesting, based on the fair market value of the shares. This means that the entire value of the shares at vesting is subject to income tax, which can be significant if the stock has appreciated.

Net Share Settlement

Many companies use a net share settlement approach, where a portion of the shares is withheld to cover the tax liability. For example, if 1,000 RSUs vest at $50 per share, the total income is $50,000. Assuming a 37% federal tax rate, approximately 370 shares would be withheld to cover the $18,500 tax liability.

**Net Share Settlement Example:**

- Total Income: $50,000

- Tax Liability: $18,500 (37%)

- Shares Withheld: 370

- Net Shares Issued: 630

Capital Gains Treatment

Once RSUs vest and the shares are delivered, any subsequent appreciation is eligible for capital gains treatment. The holding period for capital gains begins at vesting, requiring a one-year hold to qualify for long-term capital gains rates.

Critical Warning: RSU holders cannot accelerate their holding period for capital gains purposes through an 83(b) election, unlike RSA holders.

Double-Trigger and IPO Planning Considerations

Double-Trigger Vesting

Double-trigger RSUs require both a time-based vesting condition and a liquidity event, such as an IPO, to vest. This structure can defer taxation until both conditions are met, but it does not change the ineligibility for an 83(b) election.

IPO Planning

In the context of an IPO, RSUs with double-trigger provisions may accelerate vesting, leading to a significant tax event. Companies and employees must plan for the potential tax liability, often using net share settlements to manage the cash impact.

Example Calculation: Double-Trigger RSUs

Consider an employee with 2,000 double-trigger RSUs that vest upon an IPO at $25 per share. The total income recognized is $50,000, with a tax liability of $18,500 at a 37% federal rate. Approximately 740 shares would be withheld to cover taxes, leaving 1,260 shares.

**Double-Trigger RSU Example:**

- Total Income: $50,000

- Tax Liability: $18,500 (37%)

- Shares Withheld: 740

- Net Shares Issued: 1,260

Important Note: Double-trigger RSUs remain ineligible for 83(b) elections, and taxation occurs at settlement.

Not the same thing: Section 83(i) deferral

Some private-company employees explore Section 83(i) qualified equity grant deferral. 83(i) is not an 83(b) election, eligibility is different, and it does not turn RSUs into “early taxed property” in the 83(b) sense. If you are weighing RSU deferral vs RSA 83(b), treat them as separate elections with separate risks (including prospectively lost rates if law changes).

RSA Eligibility for 83(b) Elections

Advantages of 83(b) Elections

The primary advantage of an 83(b) election is the potential to convert future appreciation into capital gains, which are taxed at a lower rate than ordinary income. This can result in significant tax savings, especially for early-stage companies with low initial stock values.

Example Calculation: RSA with 83(b) Election

Assume an employee receives 10,000 RSAs at a $0.10 FMV per share and files an 83(b) election. They recognize $1,000 as ordinary income. If the stock appreciates to $10 per share by vesting, the $99,000 gain is treated as a capital gain.

**RSA with 83(b) Election:**

- Grant Date: $1,000 ordinary income

- Vesting Date: No additional tax

- Sale: $99,000 capital gain

Comparison Table: RSUs vs. RSAs

| Aspect | RSUs (typical) | RSAs + timely 83(b) (when eligible) |

|---|---|---|

| Taxation Timing | Vesting / settlement (wage income) | Ordinary income accelerated to grant transfer |

| Later appreciation | Post-delivery gain may be capital | Often capital if stock is held after vest |

| Holding Period Start | Usually from share delivery after vest | Often earlier (election-dependent) |

| 83(b) Eligibility | Generally no | Sometimes yes—confirm transfer dates |

Phantom units and “RSU-like” awards

Companies sometimes label equity as “units” or “phantom” cash plans. Payroll treatment can resemble RSUs for employees even when branding differs. Naming does not decide tax treatment—plan terms, delivery mechanics, forfeiture, and risk of loss do. If delivery is conditioned on tenure and contingent cash, you may still be outside Section 83 property transfer framing.

Related reading and calculators

- Section 83(b) election: strategic overview — economics, risk, and who should even consider an election

- How to file a Section 83(b) within 30 days — operational checklist (IRS Form 15620, copies, proof of mailing)

- Restricted stock awards (RSA) tax guide — the award type most often compared to RSUs for 83(b)

- Early exercise strategies — when options + 83(b) may be part of the picture

Interactive tools: 83(b) break-even calculator · Early exercise break-even · RSU tax estimator

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRC Section 83 — Property transferred for services | Statute | Link |

| Treasury Regulation 1.83-2 — 83(b) election | Regulation | Link |

| IRS — About Form 15620 (Section 83(b)) | IRS | Link |

| IRS Publication 525 — Taxable income | IRS | Link |

| Andersen | Article | Link |

| Brooklyn FI | Blog | Link |

| IRS | Topic | Link |

Disclaimer: This guide is for general education only and is not individualized tax, legal, or investment advice. Tax rules change, and your facts (employer plan design, residency, treaty status, payroll reporting) may differ. Consult a qualified tax professional before making decisions.