Executive Summary

How does New York tax my RSUs and stock options?

If you are a New York State resident, your worldwide compensation—including most equity settled as wages—is generally subject to NYS tax, and New York City residents typically owe NYC tax on the same wage base. If you are a nonresident, New York usually seeks tax only on income sourced to New York, often using a ratio of New York workdays to total workdays over a defined allocation period (for example, grant-to-exercise for options or the vesting period for RSUs, depending on facts and reporting). Exact sourcing follows your facts, employer reporting, and NYS rules—confirm with a NY-licensed advisor.

Tech employees in New York City and New York State routinely stack federal, state, and local taxes on equity that is paid through payroll. The painful surprises usually come from two places: multi-year sourcing (your 2026 vest may still carry 2021–2026 workdays) and withholding gaps (payroll often uses supplemental rates that are not identical to your marginal NYS/NYC bracket).

If your equity is USD-denominated but your living costs are USD in NYC, FX is rarely the main issue—bracket stacking and sourcing are. If you are on a foreign payroll with a US shadow W-2, add cross-border counsel; this article focuses on US payroll mechanics common at NY tech employers.

The bottom line: Treat NY equity tax as a multi-layer wage problem—sourcing for nonresidents, full inclusion for residents, NYC on top for residents of the city, and cash-flow planning so you are not short when the return is filed.1

Critical warning: This article is educational only. New York sourcing is fact-specific, audit-sensitive, and interacts with your employer’s payroll configuration. Do not rely on a single rule-of-thumb day ratio without professional review.

Figure 1: Resident inclusion vs. nonresident allocation—and where NYC fits for city residents.

New York residency: why it changes everything

Residents (NYS and NYC)

If you are a New York State resident, NYS generally taxes your worldwide income, including wage-style equity income reported on Form W-2. If you are also a New York City resident, you typically face an additional City resident tax on the same broad income base, subject to statutory rules and exceptions.

Planning implication: Your “where did I work when the shares vested?” question still matters for credit and allocation discussions—but residency is the first fork.

Nonresidents

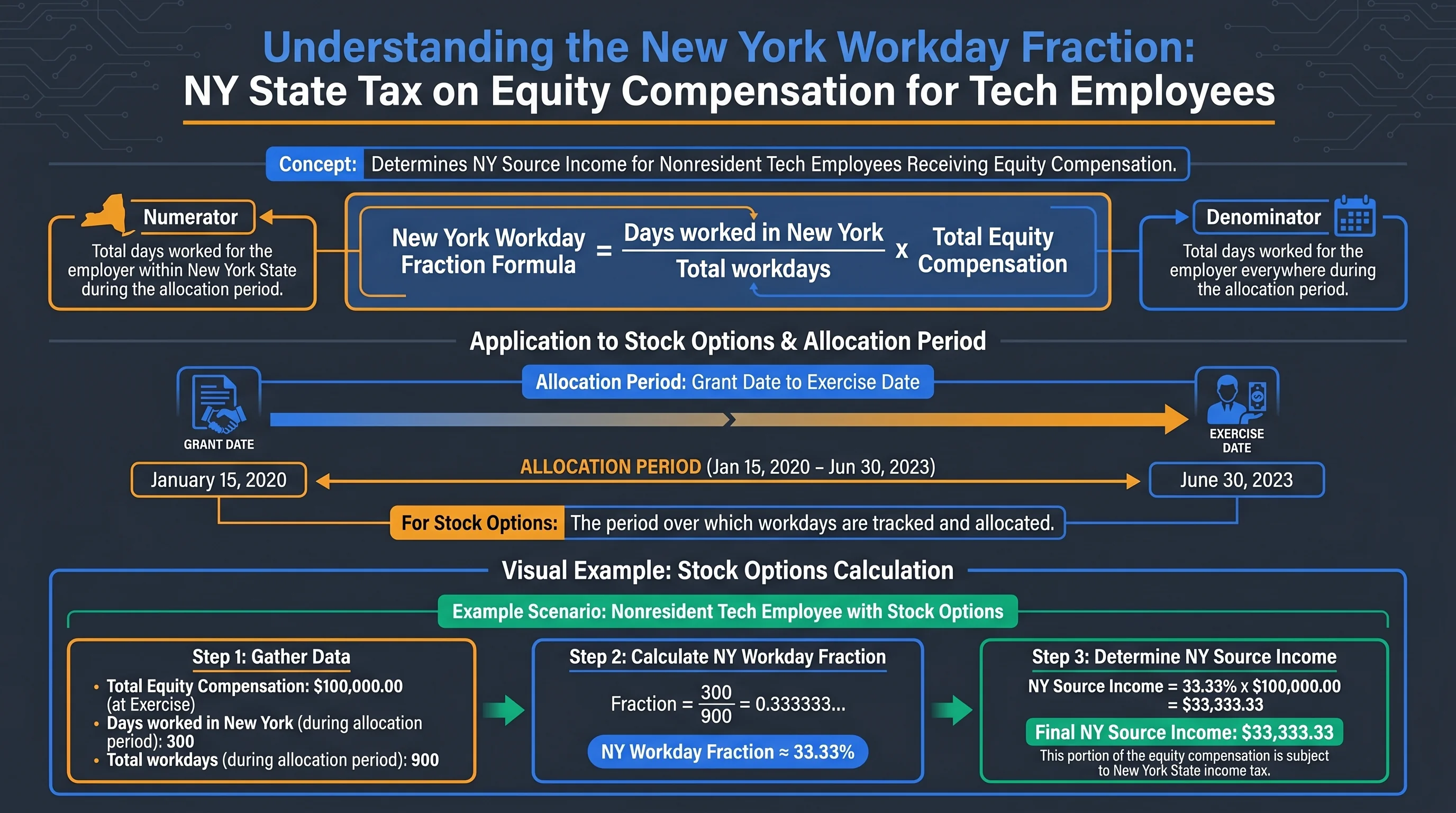

If you are not a New York State resident, NYS generally taxes only New York source income. For compensation equity, that often leads to workday-based allocation over a multi-year period.

Pair this section with our broader mobility framework: State income tax nexus for remote workers with equity and Equity compensation for remote workers (multi-state).

Figure 2: RSU vesting vs. option exercise—different events, often different allocation windows.

RSUs: vesting, payroll, and New York inclusion

Why RSUs feel like “extra salary”

When RSUs vest and shares settle through payroll, employers typically include the fair market value (less any amount you paid, if applicable) in wages. Federal income tax, FICA, and state withholding follow payroll conventions. For NYS/NYC residents, that wage income is usually in the resident base; for nonresidents, employers may allocate wages using workday ratios—but errors and mismatches between payroll reporting and your true facts are common.

Numeric example (illustrative)

Assume you vest 1,000 RSUs at $50 per share, so $50,000 is included in wages.

| Item | Amount |

|---|---|

| RSUs vested | 1,000 |

| FMV per share | $50 |

| Ordinary wage inclusion (conceptual) | $50,000 |

If you are a nonresident and your employer allocates 40% of the wage to New York based on historical New York workdays, $20,000 could be treated as New York source for NYS purposes (illustrative only—your employer methodology may differ).

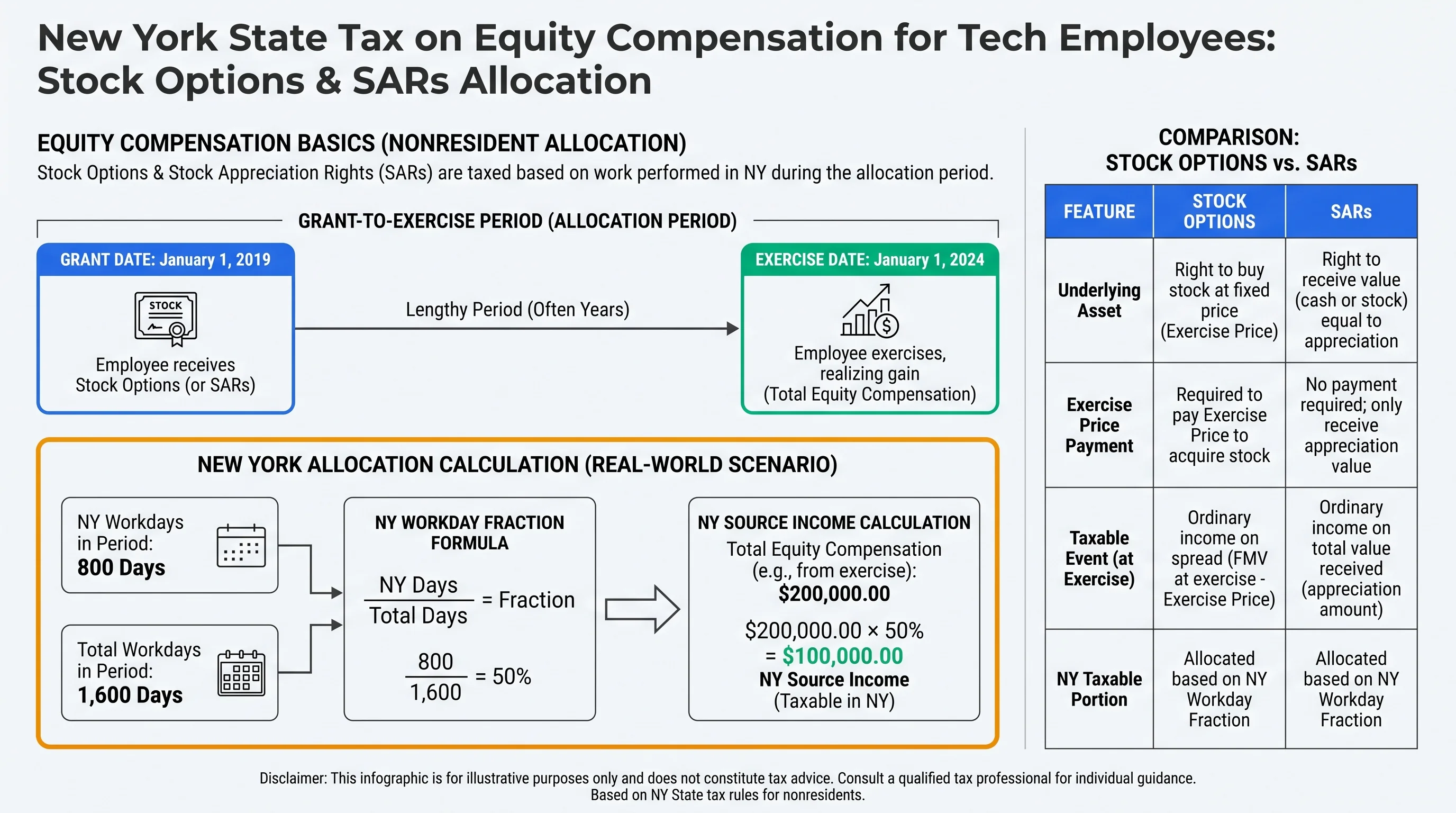

Stock options: grant-to-exercise sourcing (conceptual)

Nonqualified stock options (NSOs)

NSOs usually trigger ordinary wage income at exercise equal to the spread (FMV minus strike), unless an uncommon fact pattern says otherwise. For nonresidents, New York sourcing may examine the period from grant to exercise when determining the portion of the spread earned in New York.

Incentive stock options (ISOs)

ISOs have a bifurcated story:

- Regular tax: No ordinary wage income at exercise if you hold and meet ISO rules—but the AMT adjustment can create a federal AMT bill. See AMT planning for stock options.

- New York: If an ISO is disqualified (same-day sale, etc.), the disqualifying disposition can produce wage-like income reported on Form W-2. Sourcing and withholding then resemble NSO economics.

Figure 3: Withholding is a cash-flow tool; your true liability may be higher.

Withholding: why 22% federal does not solve New York

Employers frequently withhold federal tax on supplemental wages using the IRS’s supplemental wage rates (commonly 22% below the $1 million threshold, and 37% once supplemental wages exceed $1 million in a calendar year). That federal mechanism does not automatically mirror NYS/NYC marginal rates.

Read the deep dive: RSU and option withholding: why 22% may not be enough. For a calculator starting point, see the Supplemental wage withholding calculator.

Illustrative bracket gap

Suppose your combined marginal cash tax on the next dollar of ordinary income is 40% (federal + payroll + NYS + NYC, illustrative), but your employer withheld 22% federal on a large RSU vest plus state amounts that still leave you short. The delta becomes cash due at filing unless you increase withholding or make estimated payments (federal and state).

| Concept | Why it matters |

|---|---|

| Supplemental federal rate | Flat percentages that may trail high earners |

| NYS/NYC withholding | May not track your full marginal stack |

| Bonuses + equity same year | Multiple “peaks” can push you into higher bands |

NYC and commuters: practical buckets

City residents

If you are a NYC resident, local tax generally applies to wage income included in the city base—equity paid as wages is often in the same practical bucket as salary for planning purposes.

Nonresident commuters

If you live outside NYC but work for a NYC-based employer, your facts still matter: residency, days in city, remote work policies, and employer payroll location. Do not assume that “I never go to the office” automatically eliminates NYC sourcing without a professional analysis.

Part-year residents and “allocation years”

Many tech employees relocate in the middle of a multi-year vest. A single vest event can therefore intersect:

- A part-year resident return for the year you moved,

- Nonresident sourcing for months you were not a resident, and

- Prior-year over-withholding or under-withholding if payroll did not update residency flags quickly enough.

Practical approach:

- Fix payroll residency as soon as the move is definitive—HR systems drive default withholding.

- Build a day log that matches the same definitions your employer uses (workday vs. PTO vs. holiday).

- Reconcile per-paycheck state breakdowns to your expected annual liability before Q4 estimated tax deadlines.

For international moves, pair this guide with relocating with equity—New York is often only one layer of the story.

Estimated tax and safe harbor (why April surprises happen)

Even if your employer withholds on every vest, you can still owe interest and penalties if total payments (withholding + estimates) miss federal or state safe harbors. Large equity events in November or December are especially dangerous because there are few pay periods left to catch up.

| Scenario | Risk |

|---|---|

| Mid-year promotion + RSU acceleration | Marginal rate jumps late in the year |

| Single December vest > 50% of annual cash | Withholding may not “smooth” the bracket |

| ISO AMT + NSO exercise same year | Federal and state cash needs diverge |

Use estimated tax payments with equity as the companion playbook; New York’s underpayment rules add a state-specific column to the same calendar.

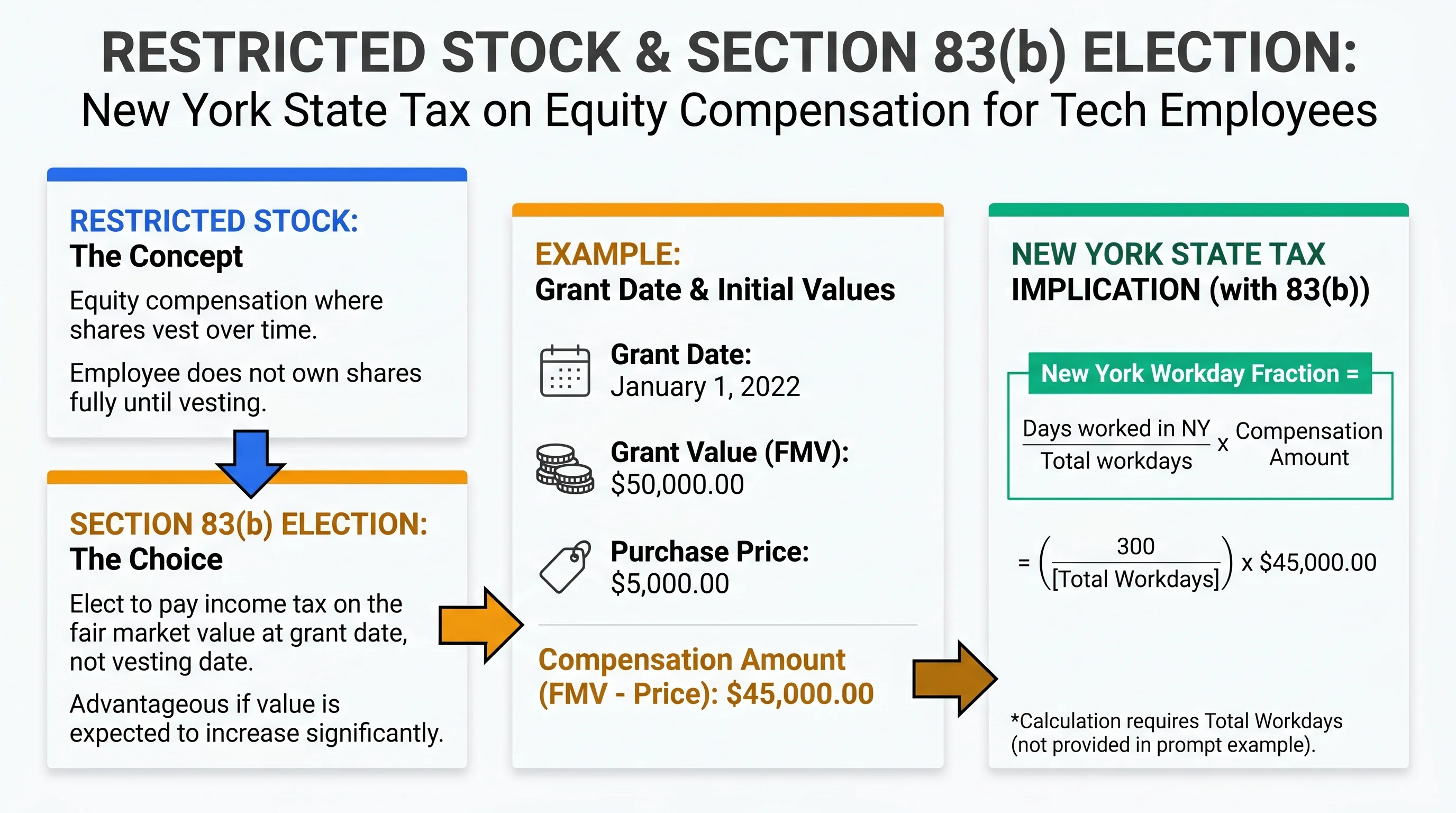

Section 83(b) and equity taxed at grant (coordination reminder)

If you file a Section 83(b) election on restricted stock (not RSUs), you may accelerate federal ordinary income to grant. New York sourcing for that inclusion can still turn on where services were performed in the year of grant—and on whether the income is New York source for nonresidents.

This is not “optional planning trivia.” Mis-coordinating grant-year inclusion with multi-year vesting can produce state-federal mismatches on W-2s. Read how to file a Section 83(b) election in 30 days before you rely on any grant-day strategy.

Documentation that survives an audit

- Employer work-location records (HRIS, badge swipes where used, corporate travel policy).

- Calendar proof for relocation dates (lease, utility bills, driver license timeline—privacy permitting).

- Grant statements showing grant date, vest schedules, exercise dates, and settlement currency.

- Payroll stubs for each vest or exercise event (federal, state, local breakdowns).

- Prior-year returns if you amend allocation methodologies—consistency matters.

For form-level reconciliation, also read Tax season reporting for stock compensation.

Multi-year scenario (numbers are simplified)

Facts (illustrative):

- NSO grant Jan 1, Year 1; exercise Jan 1, Year 5.

- Total workdays from grant to exercise: 1,000.

- New York workdays: 400.

- Spread at exercise: $300,000.

Illustrative NY source spread:

NY source ≈ $300,000 × (400 / 1,000) = $120,000

If you are a resident, the illustrative allocation changes—residents generally do not use that fraction for the same item in the same way. This is why residency is always step one.

Frequently Asked Questions

Do I owe New York taxes on RSUs if I moved to Florida mid-year?

Answer: If you were a New York resident for part of the year, you may file a part-year resident return. If you were a nonresident, NYS may still seek tax on income sourced to New York workdays during the performance or allocation period. Your payroll W-2 state allocation may not match your filing position—reconcile with a CPA.

Source: NYS — Nonresident and part-year resident income

Does New York follow the federal supplemental withholding rate?

Answer: Federal supplemental withholding is an IRS payroll rule; New York has its own withholding tables and methods. Employers must follow applicable NYS guidance; employees should verify withholding separately from federal.

Source: NYS withholding guidance

Are ISO exercises taxed the same as NSOs for New York?

Answer: Not necessarily. ISOs may have no regular wage income at exercise but can trigger AMT federally. Disqualifying dispositions can produce W-2 wage income that flows into state wage rules. Model both federal and state columns.

Source: IRS Topic 427 — Stock options

How does New York City tax RSU income?

Answer: If you are a New York City resident, NYC tax generally applies to income in the resident tax base, which commonly includes wage-style equity income. Nonresidents may have different NYC rules depending on facts—confirm with a NYC-aware preparer.

Source: NYC Department of Finance — personal income tax resources

Can my employer’s state allocation on my W-2 be wrong?

Answer: Yes. Payroll systems sometimes default to residence or office location in ways that do not match multi-year sourcing. You may need to file with a different allocation and maintain documentation—this is advanced work.

Source: IRS — Form W-2 instructions

Should I make estimated tax payments if I have large RSU vests?

Answer: Often yes, if withholding will not meet safe harbor rules. Underpayment penalties are a function of annualized tax liability, not your feelings about the vest price.

Source: IRS Publication 505

Where can I read more about multi-state equity sourcing?

Answer: Start with our state nexus guide and the multi-state remote worker guide.

Source: Internal guides

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRS — Publication 525 | Federal guidance | irs.gov/publications/p525 |

| IRS — Form W-2 instructions | Federal forms | irs.gov/instructions/iw2w3 |

| IRS — Topic 427 | Federal overview | irs.gov/taxtopics/tc427 |

| NYS — Nonresident income | State guidance | tax.ny.gov |

| NYS — Withholding | State payroll | tax.ny.gov/withholding |

Disclaimer: This guide discusses legal tax compliance and planning concepts only. Tax evasion is illegal and is never recommended. This content is for education and does not constitute tax, legal, or financial advice. Always consult a qualified professional licensed in your jurisdictions.

Footnotes

-

See NYS nonresident and part-year resident guidance and IRS Publication 525 for federal character of income. ↩