Executive Summary

How does moving affect taxes on my stock options and RSUs?

When you relocate, tax depends on sourcing rules. For state tax: income is typically sourced where you performed the work that earned it. Vesting RSUs or exercising options while in California can mean California tax even after you move. For international moves: your new country of residence may tax worldwide income; tax treaties determine relief. Exit taxes may apply when relinquishing US residency.

Relocating with equity compensation is one of the most complex tax scenarios. State sourcing rules can tax you in a state you've left. International moves trigger exit taxes, treaty questions, and dual filing. A single vesting event timed wrong can cost tens of thousands.[^1] This guide outlines the key issues.

The bottom line: Sourcing determines where income is taxed. Work location and timing of vesting/exercise matter more than where you live when the event occurs. Plan moves around vesting dates when possible.[^2]

Critical Warning: California and other high-tax states aggressively assert sourcing on equity income. If you worked in California when the equity was earned (even years ago), California may claim tax on vesting. Document your work location meticulously.[^3]

State Sourcing: The Basics

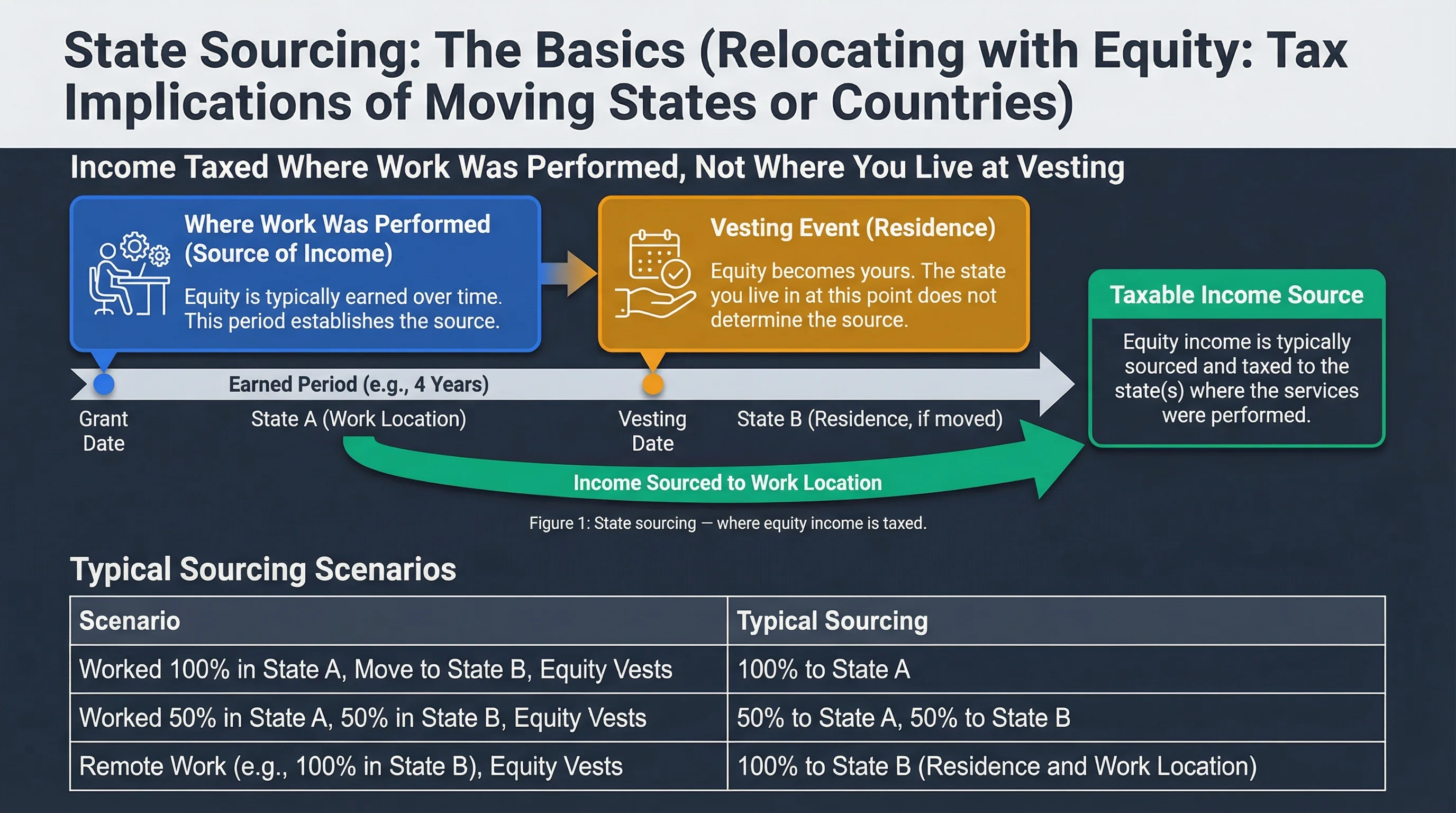

Where Is Equity Income Taxed?

Most states source compensation to where the work was performed that earned it—not where you live when it vests.

Figure 1: State sourcing — where equity income is taxed.

| Scenario | Typical Sourcing |

|---|---|

| Worked in CA, vest in TX | CA may tax (income earned in CA) |

| Worked in NY, vest after moving to FL | NY may tax |

| Worked remotely in WA, vest in WA | WA taxes (no state income tax) |

California's "Tail Tax"

California is particularly aggressive. If you earned equity through California work, the state may tax vesting income years after you leave—even if you've established residency elsewhere.

Mitigation: Some employees delay vesting until after establishing clear non-CA residency and documenting work performed outside CA. Consult a tax advisor—rules are complex.

Related Guides: California Tax on Equity Compensation, Equity Compensation for Remote Workers: Multi-State Tax.

International Relocation

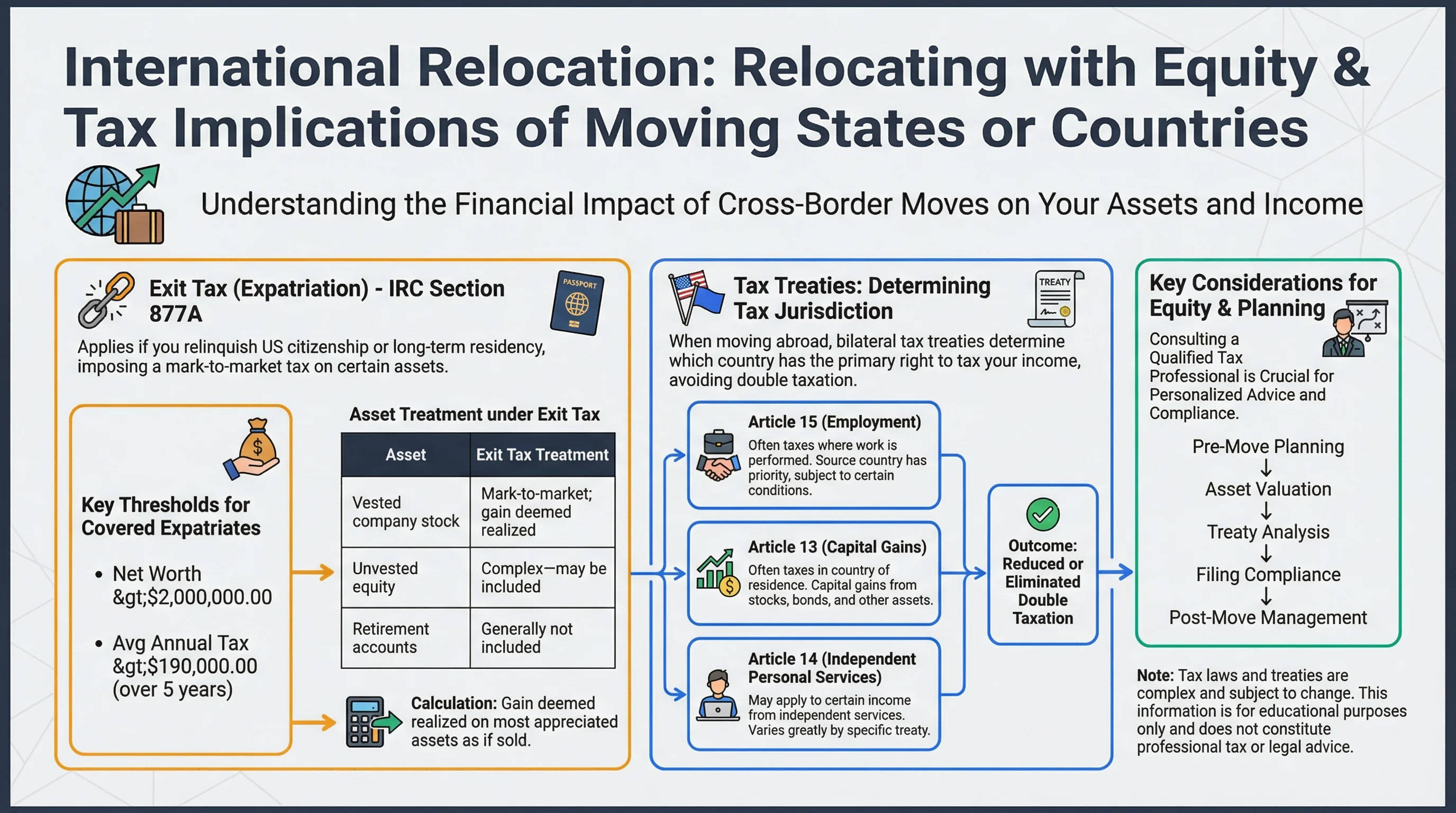

Exit Tax (Expatriation)

If you relinquish US citizenship or long-term residency, IRC Section 877A imposes an "exit tax" on certain assets, including appreciated stock. Thresholds apply (e.g., net worth >$2M or average annual tax >$190K over 5 years).

| Asset | Exit Tax Treatment |

|---|---|

| Vested company stock | Mark-to-market; gain deemed realized |

| Unvested equity | Complex—may be included |

| Retirement accounts | Generally not included |

Tax Treaties

When you move abroad, tax treaties determine which country taxes your income:

- Article 15 (Employment): Often taxes where work is performed

- Article 13 (Capital Gains): Often taxes in country of residence

- Article 14 (Independent Personal Services): May apply to certain situations

Treaty relief can avoid double taxation. You may need to file Form 8833 to claim treaty benefits.

Source: IRS Publication 519

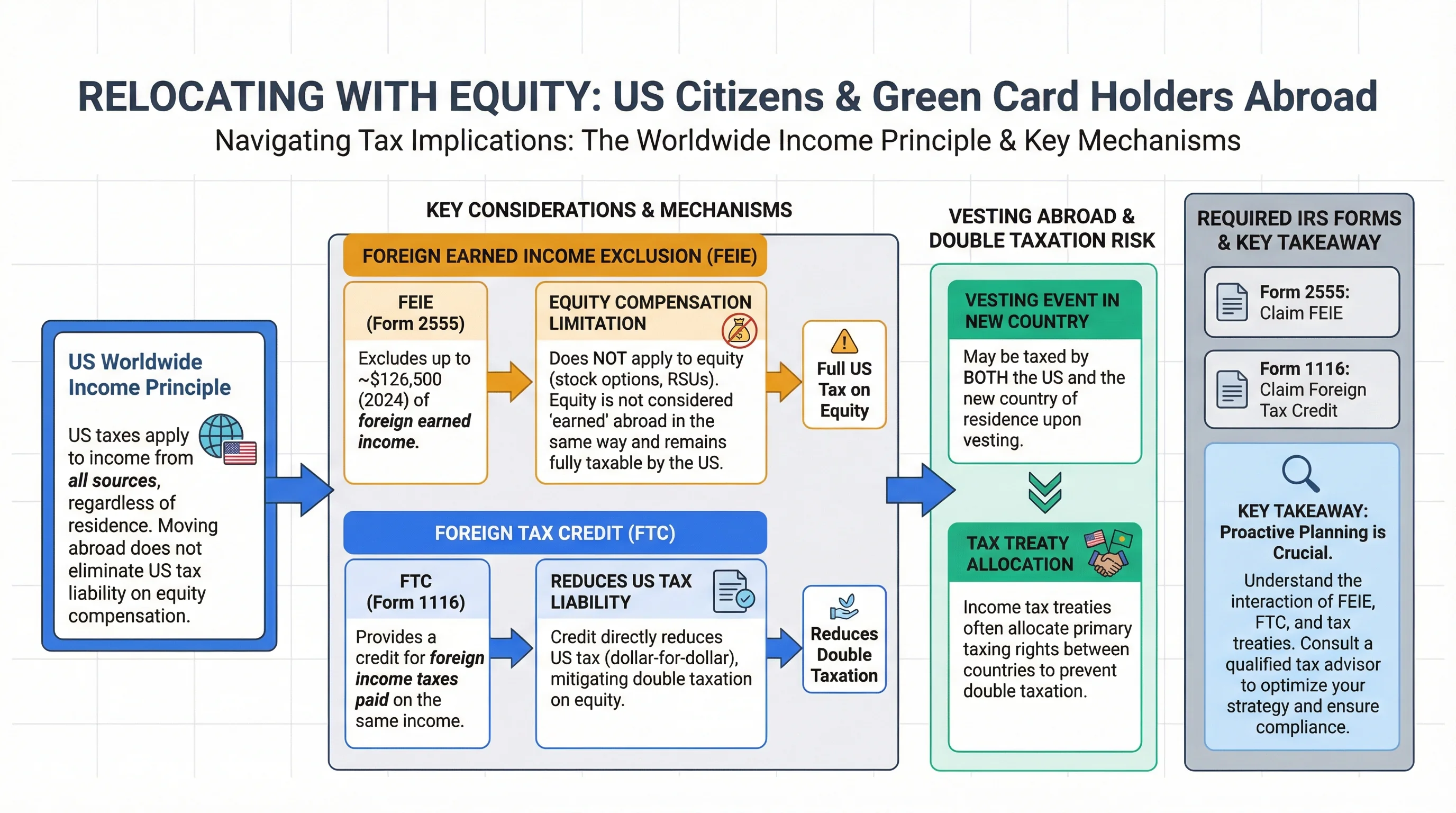

US Citizens and Green Card Holders Abroad

The US taxes worldwide income regardless of where you live. Moving abroad does not eliminate US tax on equity.

| Consideration | Impact |

|---|---|

| Foreign Earned Income Exclusion | Up to ~$126,500 (2024)—does not apply to equity compensation (it's not "earned" abroad in the same way) |

| Foreign Tax Credit | Credit for foreign taxes paid—reduces US tax |

| Form 2555 | Claim FEIE; Form 1116 for foreign tax credit |

| Vesting abroad | May be taxed by both US and new country—treaty may allocate |

Figure 2: International relocation — exit tax and treaty considerations.

Planning Strategies

Before a State Move

| Strategy | Rationale |

|---|---|

| Time vesting | Vest after establishing residency in no-tax state (e.g., TX, FL, WA) if work was performed there |

| Document work location | Keep records of where you worked each day—critical for sourcing disputes |

| Consider acceleration | If M&A is likely, model single-trigger tax in current vs new state |

Before an International Move

| Strategy | Rationale |

|---|---|

| Exercise options before leaving | Simplify—realize gain in US; may reduce foreign complexity |

| Delay vesting | If new country has lower rates or exemption—but treaty and residency rules matter |

| Plan exit tax | If expatriating, model mark-to-market impact |

| Consult treaty | Understand which country taxes what |

Figure 3: Planning strategies — before state or international moves.

Key Takeaways

- State sourcing taxes income where work was performed—not necessarily where you live at vesting

- California and other high-tax states assert aggressive sourcing on equity

- International moves trigger exit taxes, treaty questions, and dual filing for US persons

- Document work location; plan vesting timing around moves when possible

- Always consult a tax advisor for relocation—rules are jurisdiction-specific

Frequently Asked Questions

If I move to Texas, do I still owe California tax on RSUs that vest after I leave?

Answer: Possibly. California sources income to where you performed the work. If the RSUs were earned through California work, CA may tax the vesting even after you've left. Document your work location and consult a tax advisor.

Does the Foreign Earned Income Exclusion apply to RSU vesting?

Answer: Generally no. The FEIE applies to earned income from services performed abroad. RSU vesting is compensation for past services—sourcing can be complex. Consult a tax professional.

What is the exit tax threshold for expatriation?

Answer: IRC Section 877A applies if your average annual net income tax for the 5 years before expatriation exceeds ~$190K (2024), or if your net worth exceeds ~$2M. Thresholds are adjusted for inflation.

Can I avoid state tax by moving right before vesting?

Answer: Not necessarily. Sourcing looks at where you earned the income (work performed), not where you live at vesting. If you earned it in a high-tax state, that state may still tax it.

Where can I find my country's tax treaty with the US?

Answer: IRS publishes treaties at irs.gov/businesses/international-businesses/united-states-income-tax-treaties-a-to-z.

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRS Publication 519 | Reference | https://www.irs.gov/publications/p519 |

| California FTB | State | https://www.ftb.ca.gov |

| U.S. Tax Treaties | Reference | IRS Treaties |

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Always consult a qualified tax professional before making decisions based on this information.