Executive Summary

Why does Form 1099-B show $0 cost basis for my RSU sale—and how do I fix Form 8949?

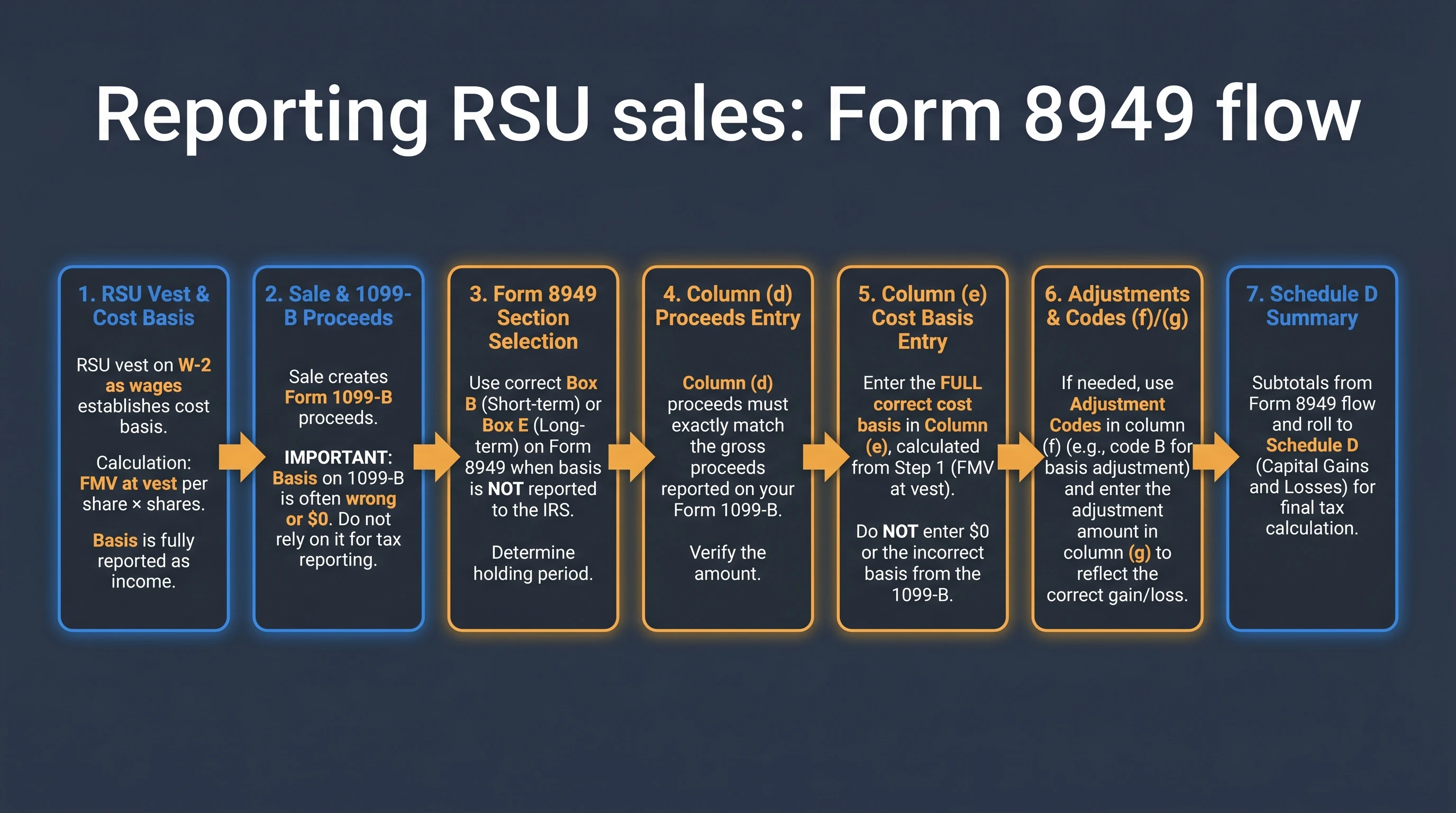

RSUs normally trigger wage income at vest based on fair market value; brokers may still print $0 or incomplete basis on Form 1099-B because they did not incorporate that payroll layer. On Form 8949, keep proceeds in column (d) consistent with the broker filing when required, then enter your true basis in column (e)—typically vest FMV × shares sold for that lot—and use columns (f) and (g) when instructions call for an adjustment explanation. That prevents taxing the same vest dollars again as capital gain.

If your equity dashboard shows Restricted Stock Units, your brain correctly remembers tax at vest. Your brokerage feed, unfortunately, often behaves like amnesia at sale time—dumping $0 into imported tax rows and quietly manufacturing fake capital gains. This guide pairs a free RSU Tax Basis Adjuster calculator with the filing logic that keeps Form 8949, Schedule D, and Form W-2 telling one coherent story. For the calculator-first walkthrough with step-by-step Form 8949 entries, see RSU Adjusted Cost Basis Calculator (Form 8949). For Publication 525 framing of the same Form 1099-B basis adjustment, see IRS Pub 525 RSU Tax Basis Adjustment Guide.1

For the full filing choreography (boxes, holding periods, Schedule D tie-out), continue to How to Report RSU Sales on Form 8949 and Schedule D and Cost Basis for Equity Compensation—this article emphasizes numbers + visuals for the double-taxation failure mode.

Critical Warning: Tax software that blindly trusts brokerage CSV imports can duplicate taxation economically—ordinary income on vest already landed on Form W-2, while overstated capital gain on sale hikes investor taxes absent manual overrides documented per IRS instructions.2

Where the double-tax illusion comes from

| Ledger | What it remembers | Typical RSU blind spot |

|---|---|---|

| Payroll / W-2 | FMV taxed as wages when RSUs vest and settle | Employee stops thinking about it by February of the next year |

| Brokerage Form 1099-B | Proceeds + broker-tracked basis | Basis often $0 or excludes compensation layer |

| Your Form 8949 | Reconciliation bridge | Must reconstruct wage basis—imports skip this |

Planning move: Treat vest confirmations (FMV per share, share counts, settlement dates) as mandatory attachments in the same folder as trade confirmations.

Use the RSU Tax Basis Adjuster (interactive)

The RSU Tax Basis Adjuster estimates:

| Output | Meaning |

|---|---|

| Correct adjusted basis / share | Vest FMV already taxed as wages (your baseline before appreciation) |

| Broker-reported basis / share | What many imports default to—often 0 |

| Capital gain delta | Phantom gain if you accept the broker basis vs using wage-backed basis |

Enter sale price, FMV per share at vest for the shares sold, optional 1099-B basis, and share count to see totals. The tool is educational—confirm lot IDs, multi-vest layering, and fees with your statements or adviser.

Visual: wage layer vs brokerage import

Imagine you vested 100 shares at $180.00 FMV, taxed on payroll, then sold later at $210.00:

W-2 wage layer (already taxed): $180.00 / share → included in ordinary income at vest

Broker import basis (failure mode): $0.00 / share → phantom gain if accepted

True economic gain on sale: $210 − $180 = $30 / share (pre-fees illustration)

Phantom gain if basis left at $0: $210 − $0 = $210 / share (incorrect)

That $180 wedge is not “extra complicated theory”—it is the same dollars HR already ran through withholding. Form 8949’s job is to stop them from being taxed again as capital gain.3

Mapping inputs to Form 8949 columns (conceptual)

| Column | RSU sanity check |

|---|---|

| (d) Proceeds | Match broker totals per reconciliation rules unless a narrow exception applies |

| (e) Cost or other basis | Vest FMV basis for shares sold (aggregate across lots carefully) |

| (f)/(g) Adjustments | Use when instructions require codes/amounts to explain broker vs taxpayer basis gaps |

Checkbox choice (Part I Box B short-term vs Part II Box E long-term) follows holding period counting from acquisition through sale—usually the day after settlement through disposition per annual instructions.4

Sell-to-cover and multiple vests (short caveats)

- Sell-to-cover can split economics across withholding sales vs investment lots—tie each sale row to the correct vest ID instead of averaging from memory.

- Multiple vests mean multiple FMVs; FIFO is common but not universal—match employer supplemental PDFs.

Deep dives: RSU sell-to-cover withholding and RSU withholding gaps.

Figure 1: Payroll wage inclusion at vest feeds your true basis; brokerage proceeds still reconcile on Form 8949 before Schedule D totals.

Frequently Asked Questions

Is RSU double taxation on Form 8949 real?

Answer: Economically, yes—if you leave broker basis at $0, you risk taxing vest income twice (once as wages, again as overstated capital gain). Fixing basis on Form 8949 aligns with the wage inclusion already reported.5

Does IRS Publication 525 say RSU vesting is taxable?

Answer: Publication 525 summarizes compensation frameworks—including restricted stock and RSU wage inclusion concepts—that underpin why basis should reflect income already recognized.6

What if my 1099-B shows a nonzero basis that still looks wrong?

Answer: Reconcile against equity tax supplements; brokers may carry transfer or incomplete legacy basis. Your adjustment story must still satisfy Form 8949 instructions for the relevant checkbox column family.

Do state returns follow the same basis logic?

Answer: Often conceptually similar, but state sourcing (especially moves mid-year) may split wage vs sale reporting—pair federal fixes with multi-state equity guidance when relevant.

Where can I estimate taxes before April?

Answer: Use RSU Tax Estimator for vest ordinary income context alongside this basis tool for after-sale capital reporting.

Footnotes

Primary Sources

| Source | Role |

|---|---|

| About Form 8949 | Reconciliation purpose |

| Instructions for Form 8949 | Checkbox grids, columns, exceptions |

| About Schedule D | Capital gain roll-forward |

| Publication 525 | Compensation vs investment framing |

| Publication 550 | Basis/capital asset concepts |

Disclaimer

This guide is general education only—not individualized tax, legal, or investment advice. IRS instructions and brokerage formats change; read current PDFs, retain source PDFs, and engage a CPA or EA familiar with equity compensation before filing.

Footnotes

-

IRS overview—Form 8949 reconciles broker statements with taxpayer reporting before Schedule D aggregation. irs.gov/forms-pubs/about-form-8949 ↩

-

Import pitfalls mirror double-tax explainer for RSUs narrative—wage vs brokerage disconnect. ↩

-

Basis reconstruction themes align with Form 1099-B equity guide examples. ↩

-

Holding-period conventions summarized annually in Instructions for Form 8949—verify each filing season. irs.gov/instructions/i8949 ↩

-

Conceptual overlap with cost basis deep dive adjustment commentary. ↩

-

IRS Publication 525—taxable compensation overview. irs.gov/publications/p525 ↩