Executive Summary

I live in France and my US employer’s RSUs vest here—what should I expect?

Expect French taxation on the equity component that French rules treat as employment or similar income for your facts, usually with withholding or payroll coordination through your employer’s French entity or a shadow payroll. The taxable event and the applicable social charges depend on plan design and whether French qualified regimes apply. If you are a US citizen or green card holder, you will also report the income on a US return and typically coordinate French tax with Form 1116—subject to limitations.

US tech workers in Paris, Lyon, or remote from France increasingly receive US parent-company equity—RSUs, non-qualified stock options, and occasionally ISOs (ISOs are a US creature; they do not “import” into French law as ISOs). If you are French tax resident, you must map those awards onto French income tax and social contribution rules first, then—if you are a US person—layer US worldwide taxation and foreign tax credits.

Start from our general France equity compensation guide for BSPCE, PFU, and local vocabulary. For US-side mechanics (ISO vs NSO, AMT concepts), see ISO vs NSO. For cross-border framing beyond France, see international equity tax planning and relocating with equity.

The bottom line: The hard part is not the acronym on your grant—it is timing (when France sees income), character (wage-like vs investment return), and who reports first (French payroll vs US payroll vs broker). Assume nothing from your US grant letter without a French-side review.1

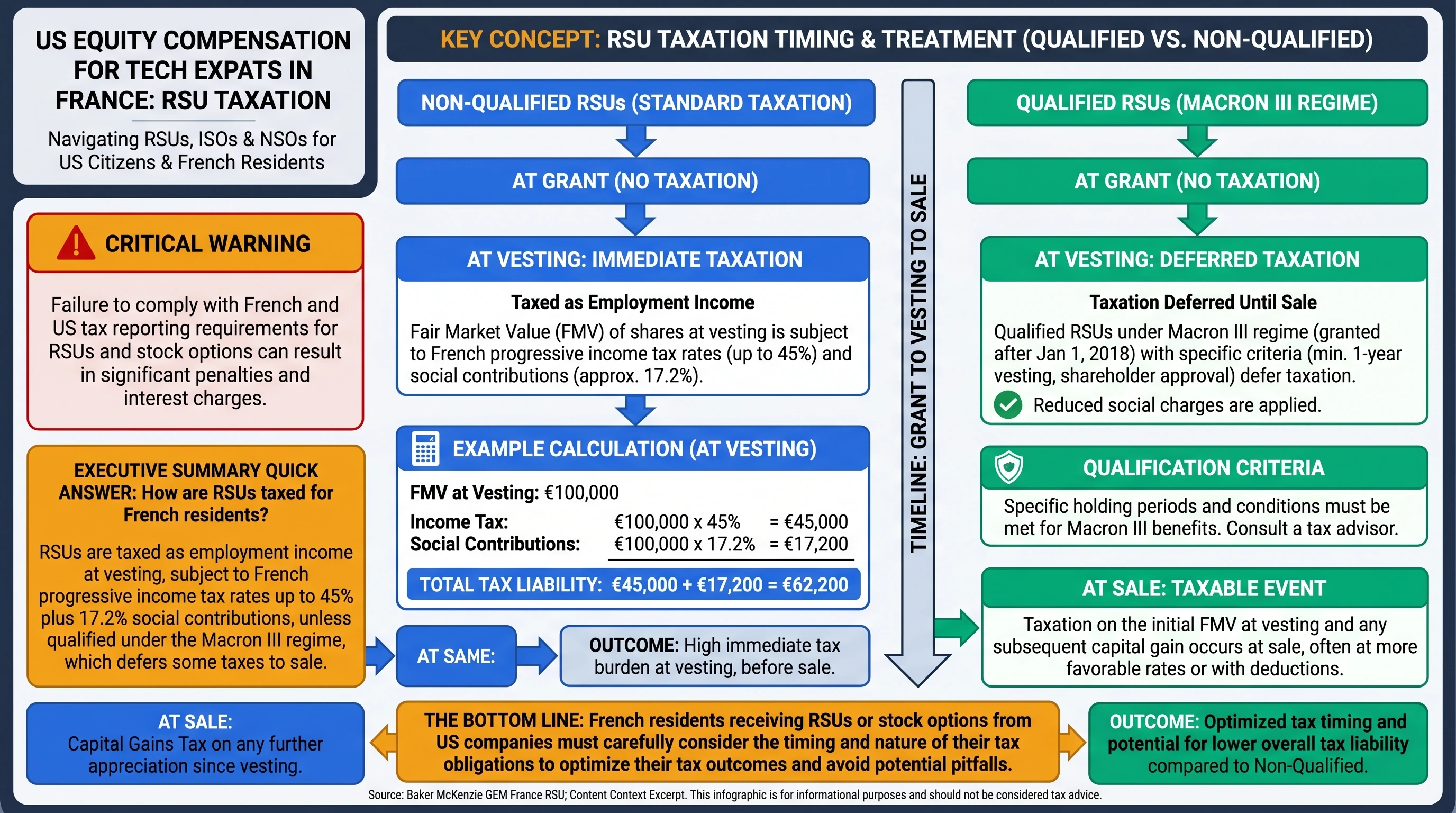

Critical Warning: Articles that quote a single “45% + 17.2%” stack on the full vest are misleading for most taxpayers because French income tax is progressive and social charges depend on income category and year. Use this guide for concepts, not a final liability number.2

RSU Taxation for French Residents

Timing: vest, delivery, and payroll reporting

For many US plans, RSUs trigger ordinary wage treatment in the US at vest for federal purposes. In France, the taxable moment is determined under French rules for employee awards—often tied to delivery, transferability, and forfeiture conditions, and to how your employer runs French payroll (or a shadow payroll) for residents.

What to collect from your employer each vest:

| Document | Why it matters |

|---|---|

| Vest confirmation (shares, FMV, FX) | Reconcile EUR inclusion vs broker |

| French payslip / tax-at-source summary | Shows French wage reporting and withholdings |

| Plan summary (qualified vs non-qualified in France) | Determines whether “Macron”-style benefits could apply |

“Macron law” RSUs (high level only)

France has enacted several waves of employee-share incentives (commonly discussed as Macron I / II / III in practitioner materials). Qualified grants can change when income tax and certain social consequences occur compared with “plain” free shares. Most US multinational RSU programs do not automatically satisfy French qualification tests (holding periods, grant caps, shareholder approvals, issuer size/tests). Treat marketing slides as a hypothesis until a French payroll/tax team confirms.

| If your grant is… | Practical posture |

|---|---|

| Likely non-qualified in France | Expect wage-like taxation at the French taxable event; focus on payroll withholding and EUR reporting |

| Potentially qualified | You need a determination letter-level review—eligibility is easy to get wrong |

Worked illustration (progressive tax, simplified)

Suppose €40,000 of RSU value is treated as French ordinary income for the year after other salary, and suppose (purely illustrative) that the marginal income tax slice on those euros is 30% and employee social charges on that employment component sum to ~10% for the scenario (rates change; this is not a quote for your payslip).

Illustrative French income tax on the RSU slice: €40,000 × 30% = €12,000

Illustrative employee social charges on that slice: €40,000 × 10% = €4,000

Total (illustrative): €16,000

Compare that to the wrong shortcut “45% + 17.2% on everything,” which overstates tax for many families because it ignores brackets, credits, household composition, and income categories.

Cross-border vesting while resident in France

If you vest while French resident but performed services in multiple countries during the earning period, sourcing can split taxation. The analysis is not a 50/50 guess—it depends on days, employer charge, treaty employment article, and payroll location. If you are in this bucket, you are past free internet guidance; bring your calendar and assignment letters to a specialist.

High-level map of how US equity awards interact with French and US reporting layers—always confirm plan-specific facts with a cross-border advisor.

US Stock Options While French Resident: NSOs vs ISOs (and why BSPCE is different)

NSOs (non-qualified US options)

US NSOs are the common option type at public tech companies. Economically, the spread at exercise is ordinary compensation in the US. In France, exercise gains on employer options are often analyzed as employment income when French wage-income tests are met—but the taxable event, FX, and social treatment are French questions.

Practical checklist at exercise:

| Step | Question |

|---|---|

| 1 | Was exercise reported on French payroll in EUR, or only US payroll? |

| 2 | Do you have a same-day sale (cashless exercise) generating broker proceeds? |

| 3 | Are shares restricted after exercise (repurchase/lock-up) affecting French timing? |

For US tax mechanics on the spread and withholding, read ISO vs NSO alongside this page.

ISOs (incentive stock options)

ISOs matter for US AMT and holding-period tests. France does not “recognize ISOs.” You may have no US ordinary wage income on a qualifying ISO exercise for regular US tax, while France may still see a taxable employment benefit at exercise or sale depending on facts. That mismatch is where professionals earn their fees: US AMT, French wage taxation, and later sale taxation do not line up neatly.

BSPCE is not “your US option, but French qualified”

BSPCE is a French startup instrument with its own eligibility rules. It is not the same as a US ISO/NSO because you live in France. If you have BSPCE, use our France equity guide. If you have US options, do not assume BSPCE benefits apply.

| Instrument | Typical employer | First question |

|---|---|---|

| US NSO/ISO | US listed parent | French payroll + US exercise reporting |

| BSPCE | French qualifying startup | French qualification tests |

| French “Macron” free shares | French issuer / specific plans | Holding period + employer social charges |

US–France treaty: employment income, residency, and why “Article 15” is not the whole story

The US–France income tax treaty (PDF) is primarily a tie-breaker and relief document: it helps determine which country may tax first and how to reduce double taxation—it does not replace French payroll law or US Form 1040 reporting.

| Topic | Practical takeaway |

|---|---|

| Residency / tie-breaker | If you might be resident under both domestic tests, the treaty’s tie-breaker can pick a single treaty residence for many purposes |

| Employment income | Compensation for work performed is often taxed where the services are rendered—remote work from France for a US employer is a modern flashpoint |

| Relief from double taxation | Mechanisms exist (credit/exemption articles), but timing and income character must match US rules to claim benefits cleanly |

Treaty analysis is not “RSUs are always French-sourced.” Your grant terms, payroll location, days in country, and corporate structure matter.

US side for expats: foreign tax credit (and where FEIE usually does not help)

Foreign tax credit (Form 1116)

Most US citizens in France use the foreign tax credit to reduce US tax on income that France also taxes. IRS Publication 514 explains credit limits, sourcing, and the foreign tax definition.

Why credits feel “broken” sometimes:

| Friction | What it means |

|---|---|

| Timing mismatch | France and the US may recognize income in different years |

| Basket rules | Passive vs general limitation can split your credit |

| Withholding ≠ final tax | US rules care about accrued foreign tax in many cases |

FEIE (Form 2555) — use carefully

The foreign earned income exclusion can help earned wages from foreign employers in some facts—but equity compensation is often not cleanly excluded, and FEIE can interact poorly with FTC planning. If your advisor mentions FEIE, ask explicitly how it applies to RSU/option income in your specific payroll setup.

After the wage layer: PFU vs progressive tax on listed share gains (orientation)

France’s PFU (often called flat tax) is a bundled approach many taxpayers use for certain investment income, with components that commonly include 12.8% income tax plus social levies (historically discussed as 17.2% in aggregate PFU framing—verify current law for your year). You may elect taxation at progressive income tax rates instead if that is better for your overall return—the election is global for eligible investment income categories for the year, not “per stock.”

Important: The wage taxation at vest/exercise and the PFU/progressive taxation on later share price appreciation are different layers. This is the same conceptual split as our RSU double-tax myth guide—but French categories are not identical to US rules. For the US-only baseline on RSU wage inclusion, see also comprehensive RSU taxation.

| Question for your filing | Why it matters |

|---|---|

| Were shares listed at sale? | PFU/progressive mechanics differ from some unlisted cases |

| Did you hold long enough for any rebate regime? | Holding-period discounts have changed over recent reforms |

| Do you file jointly with a spouse holding securities? | Household elections can dominate |

For France’s domestic vocabulary (BSPCE, PFU, prélèvements), keep France equity compensation open in another tab.

Frequently Asked Questions

I am a US citizen living in France—do I pay tax twice on the same RSU vest?

Answer: You may owe tax to both countries on the same economic income, but the US system usually mitigates double taxation through the foreign tax credit (and occasionally treaty-dependent positions). The mitigation is rarely “automatic payroll perfection”—FX, timing, and Form 1116 baskets matter.

Source: IRS Publication 514 — Foreign Tax Credit

Does France tax US ISOs as ISOs?

Answer: No. ISO is a US statutory category. France analyzes the facts under French wage and securities rules. You can still have US AMT complexity even when France treats an exercise as employment income in EUR.

Source: ISO vs NSO (US framework)

What is the “Macron law” chatter I hear about French RSUs?

Answer: France has enacted several employee-share incentive packages (often called Macron I/II/III in practice). Qualified grants can change timing and social charge mechanics compared with plain grants. US multinational RSUs often do not qualify without specific French legal structuring—verify instead of assuming.

Source: Legifrance — consolidated French law research

Where should I start for purely French domestic mechanics (BSPCE, PFU, social charges)?

Answer: Use our pillar page on France equity compensation for local vocabulary, then return here for the US grant + French residence overlay.

Source: VestingStrategy — France equity guide

Can I use the Foreign Earned Income Exclusion to hide RSU income from the IRS?

Answer: Generally no—and trying to force RSU/option income into FEIE without a careful analysis is a common mistake. Many equity items are not “foreign earned income” in the sense practitioners use for exclusion planning, and FEIE can interact poorly with FTC optimization.

Source: IRS — Foreign Earned Income Exclusion

How do I think about PFU vs progressive tax on a US tech salary + equity?

Answer: Employment equity is usually taxed through wage mechanisms first. PFU often matters for later investment returns on listed securities, subject to annual elections and household rules. The “30%” headline is not a substitute for modeling your full return.

Source: impots.gouv.fr — particuliers

I work remotely from France for a US employer—what is the first compliance question?

Answer: Whether your employer has a French payroll / permanent establishment analysis and how social contributions are allocated. Equity is downstream of that employment fact pattern.

Source: OECD Model Tax Convention commentary (background)

What documents should I keep for a US–France equity vesting year?

Answer: Vest statements, French and US payslips, broker trade confirmations, corporate FX rates used by payroll, prior-year US and French returns, and any treaty position memos from your advisor.

Source: IRS — Recordkeeping

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| impots.gouv.fr | Official (France) | https://www.impots.gouv.fr/particulier |

| Legifrance | Official (France) | https://www.legifrance.gouv.fr/ |

| US–France tax treaty (IRS PDF) | Treaty | https://www.irs.gov/pub/irs-trty/france.pdf |

| IRS Publication 514 | IRS guidance | https://www.irs.gov/publications/p514 |

| IRS — Foreign Earned Income Exclusion | IRS guidance | https://www.irs.gov/individuals/international-taxpayers/foreign-earned-income-exclusion |

Disclaimer: This guide is for general education only and is not individualized tax, legal, or investment advice. Tax rules change, and your facts (employer plan design, residency, treaty status, payroll reporting) may differ. Consult a qualified tax professional before making decisions.

Footnotes

-

For US FTC mechanics, see IRS Publication 514 — Foreign Tax Credit (https://www.irs.gov/publications/p514). ↩

-

French marginal rates are progressive; social charges vary by income category—verify annually on impots.gouv.fr. ↩