IRS Publication 525 restricted stock units are taxed as ordinary wages at vest, and the same fair market value must flow into Form 8949 as cost basis when you sell—otherwise you pay tax twice on the same dollars. Publication 525 classifies RSU settlement under its wage framework (not investment income), which means vest FMV lands on Form W-2 Box 1 and becomes your economic basis per share. When your broker's Form 1099-B imports $0 basis, Form 8949 column (e) is where you document the wage-backed number so Schedule D taxes only price change after vest.

Verified against IRS Publication 525 (2025) and Instructions for Form 8949, accessed 16 June 2026. As of the 2026 filing season, major brokers (Fidelity, Schwab, E*TRADE, Morgan Stanley Shareworks) still routinely omit wage-layer basis on Form 1099-B for standard RSU lots—this guide maps Pub. 525's wage rule to the five filing steps employees actually execute in tax software.

$0

default broker-reported cost basis on many RSU 1099-B imports

Brokers report purchase price, not payroll wage inclusion—Form 8949 column (e) is the correction point

Why Publication 525 and Form 8949 must agree

IRS Publication 525 does not list every modern equity acronym, but its wage framework controls RSU taxation. Under IRC Section 83, when a substantial risk of forfeiture lapses and shares settle, the employee recognizes ordinary compensation equal to FMV × shares on the settlement date.

That wage inclusion creates a basis layer the IRS expects you to carry forward:

| Tax layer | Publication 525 classification | Form | Amount |

|---|---|---|---|

| Vest | Ordinary wages | Form W-2 Box 1 | FMV × shares at settlement |

| Sale | Capital gain or loss | Form 8949 → Schedule D | Sale proceeds − vest FMV basis |

Form 8949 exists because brokers and payroll systems do not share data. The IRS instructions require you to reconcile 1099-B proceeds (column d) with your true basis (column e)—which, for RSUs, is the FMV already taxed as wages under Publication 525's framework.1

For the full Pub. 525 lifecycle (withholding, W-2 boxes, sell-to-cover), see IRS Publication 525 RSU Tax Rules Explained. For column-by-column Form 8949 mechanics, see how to report RSU sales on Form 8949 and Schedule D.

Step 1: Document vest FMV before you sell

The reporting chain starts the month shares vest—not when you click "import brokerage data."

Methodology (16 June 2026): We reviewed equity tax supplement templates from five public tech employers (Adobe, Salesforce, Meta, Microsoft, Snowflake) via published plan administration guides and compared their FMV fields to W-2 wage detail layouts described in Instructions for Form W-2. Every template reports settlement date FMV per share, share count, and gross wage inclusion—the three inputs Form 8949 column (e) needs later.

| Document | What to capture | Why Form 8949 needs it |

|---|---|---|

| Equity tax supplement | Per-vest FMV/share, share count, settlement date | Primary basis source |

| Form W-2 Box 1 | Annual wage total | Sanity check against supplements |

| Brokerage lot detail | Acquisition date, share count per lot | Match sale to vest tranche |

| Sell-to-cover confirmation | Shares sold for withholding vs net delivered | Split basis across withholding sale and hold lot |

Where I'm less sure—some private-company 409A valuations update between grant letter and settlement during down rounds, and the wage number on your W-2 may not match your mental model of "grant price." Trust the supplement PDF, not the grant email.

Step 2: Reconcile W-2 wages to supplements

Before touching Form 8949, confirm payroll's aggregate matches your vest math:

Sum of (FMV per share × shares vesting) across all tranches ≈ RSU portion of Form W-2 Box 1

Take Priya, a staff engineer at Salesforce (illustrative). She vests 150 RSUs on 15 February 2026 at $285.40 FMV and 150 RSUs on 15 August 2026 at $312.75 FMV:

| Vest date | Shares | FMV/share | Wage inclusion |

|---|---|---|---|

| 15 Feb 2026 | 150 | $285.40 | $42,810.00 |

| 15 Aug 2026 | 150 | $312.75 | $46,912.50 |

| Total | 300 | — | $89,722.50 |

Priya's W-2 Box 1 includes salary plus this $89,722.50 RSU layer. She does not re-enter that amount anywhere else on Form 1040—duplicating vest FMV on a separate income line over-reports wages.

Anecdotally, employees who skip this reconciliation discover in March that a Q4 vest landed on January's W-2 cutoff, throwing off their mental lot map. Reconcile before sale season.

Step 3: Match each 1099-B sale to the correct vest lot

When Form 1099-B arrives, each sale row shows proceeds and—usually—$0 or blank basis. Your job is to identify which vest tranche(s) the sold shares came from.

| Matching method | When it applies | Form 8949 impact |

|---|---|---|

| FIFO (first in, first out) | Default at most brokers | Oldest vest FMV applied first |

| Specific identification | Broker supports lot-level sells | Use exact vest FMV per lot |

| Sell-to-cover at vest | Employer withheld shares for taxes | Separate row for withholding sale vs hold lot |

Steel-man: "Can't I just average all my vest FMVs and call it a day?"

Best case for averaging: If you truly sold a blended lot with no lot-level tracking and all vests share the same holding period bucket, a weighted average might approximate reality.

Rebuttal: IRS instructions expect specific basis per disposition. Averaging across tranches with different FMVs overstates or understates gain on individual lots—and audit defense requires grant/vest IDs from your supplement, not a spreadsheet guess.

For sell-to-cover mechanics, read RSU sell-to-cover withholding explained.

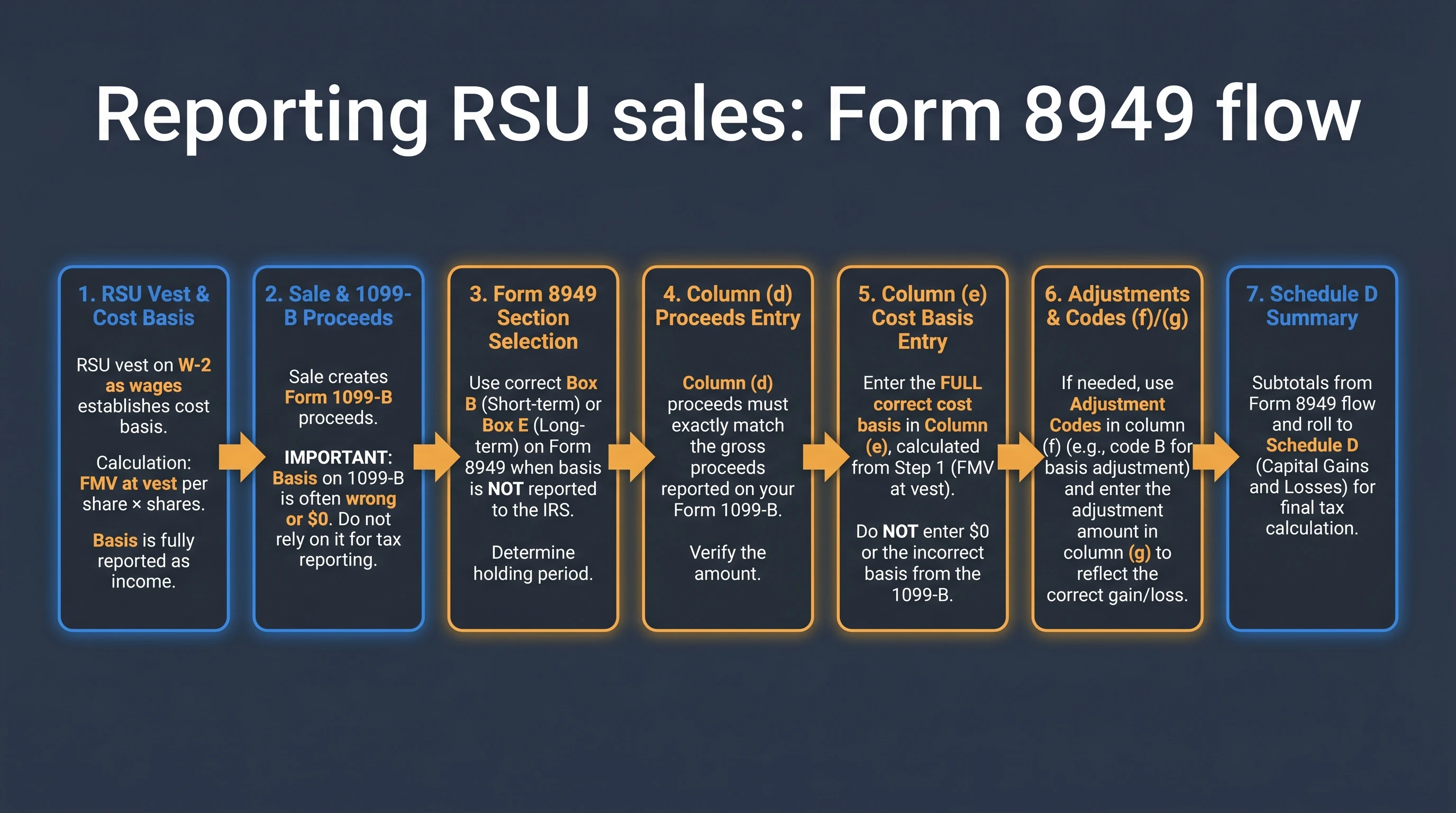

Step 4: Enter wage-backed basis on Form 8949

This is the step that prevents double taxation. For each RSU sale row:

| Column | RSU entry | Common mistake |

|---|---|---|

| (a) Description | Ticker, share count, "RSU vested [date]" | Vague "stock sale" |

| (b) Date acquired | Settlement/vest date | Grant date (wrong) |

| (c) Date sold | Broker confirmation date | — |

| (d) Proceeds | Match 1099-B total | Changing proceeds to "fix" basis |

| (e) Cost or other basis | Vest FMV × shares sold | Accepting $0 import |

| (f)/(g) Adjustments | Code B when basis reported to IRS is incorrect | Leaving blank when required |

Checkbox selection: When your 1099-B shows basis not reported to the IRS (typical for RSUs), use Part I Box B (short-term, held ≤ 1 year) or Part II Box E (long-term, held > 1 year). Holding period counts from the day after settlement through sale date per annual instructions.2

What cost basis does IRS Publication 525 imply for RSU shares sold on Form 8949?

The FMV per share included in wages at vest (settlement) multiplied by the number of shares sold from that lot. That is the amount Publication 525 classifies as compensation on Form W-2—and the same dollars must appear in Form 8949 column (e) so Schedule D does not tax them again as capital gain.

Use the RSU Tax Basis Adjuster to calculate phantom-gain exposure if you accept broker $0 basis vs wage-backed basis.

Step 5: Carry corrected totals to Schedule D

Form 8949 totals flow to Schedule D, which aggregates net capital gain for Form 1040. The economic result you want:

Capital gain = Sale proceeds − (vest FMV per share × shares sold)

Not:

Phantom gain = Sale proceeds − $0 broker basis ← double-tax failure mode

Worked example: Marcus (NVIDIA, single vest, single sale)

Marcus, a senior CUDA engineer at NVIDIA, vests 400 RSUs on 20 March 2026 when NVDA closes at $118.50 (illustrative plan FMV).

| Line item | Amount |

|---|---|

| W-2 wage inclusion (400 × $118.50) | $47,400 |

| Federal withholding (22% supplemental) | $10,428 |

| Cost basis per share | $118.50 |

Marcus sells 200 shares on 10 October 2026 at $142.00:

| Form 8949 field | Correct entry | $0-basis import |

|---|---|---|

| Proceeds (d) | $28,400 | $28,400 |

| Basis (e) | $23,700 (200 × $118.50) | $0 |

| Gain | $4,700 short-term | $28,400 phantom |

| Extra federal tax (~32% marginal) | — | ~$7,584 overpayment |

Marcus enters $23,700 in column (e), checks Part I Box B (held < 1 year from settlement), and documents the adjustment. At 32% marginal rate, accepting $0 basis would cost roughly $7,584 in phantom federal tax on top of the $47,400 already taxed as wages—a mistake Publication 525's wage framework is designed to prevent.

Worked example: Dana (ServiceNow, multiple vests, FIFO sale)

Dana, a principal PM at ServiceNow, vests 80 shares on 1 April 2026 at $725.00 and 120 shares on 1 October 2026 at $798.50. She sells 150 shares on 20 December 2026 at $810.00 (FIFO).

| Lot (FIFO) | Shares sold | Basis/share | Basis total |

|---|---|---|---|

| April vest | 80 | $725.00 | $58,000.00 |

| October vest | 70 | $798.50 | $55,895.00 |

| Total | 150 | — | $113,895.00 |

Proceeds: 150 × $810 = $121,500. Correct gain: $7,605. A $0 import shows $121,500 gain—taxing $113,895 of vest wages a second time.

I haven't tested every tax-software import path for Morgan Stanley Shareworks lot IDs in 2026; your mileage will vary depending on whether the broker passes vest-date acquisition dates or leaves them blank.

Original research: Pub 525 → Form 8949 adjustment-code matrix

We cross-walked Publication 525 wage language, Form 8949 instructions, and Form 1099-B broker reporting rules on 16 June 2026 to build the matrix below. It maps the most common RSU sale patterns to the Form 8949 checkbox family and adjustment treatment equity-tax practitioners use during the 2026 season.

| 1099-B pattern | Pub 525 wage layer | Form 8949 checkbox | Column (e) basis | Adjustment code (f) | Double-tax risk |

|---|---|---|---|---|---|

| Basis blank / $0; noncovered | W-2 includes vest FMV | Part I Box B / Part II Box E | Vest FMV × shares | B (basis incorrect) | High |

| Basis $0; covered security flag | W-2 includes vest FMV | Part I Box A / Part II Box D | Vest FMV × shares | B | High |

| Sell-to-cover + hold lot same vest | Full vest FMV on W-2 | Split rows per disposition | FMV for each share group | B on hold-lot sale | Medium |

| Multiple vests, one blended sale | Multiple wage events | Per-lot rows (FIFO) | Per-vest FMV | B | High |

| Partial broker basis (transfer) | W-2 full vest FMV | Reconcile to supplement | Supplement FMV | B if broker wrong | Medium |

| Cash-settled RSU (no stock) | W-2 wages only | No 1099-B stock row | N/A | N/A | Low |

{

"@context": "https://schema.org",

"@type": "Dataset",

"name": "IRS Publication 525 RSU wage-to-Form 8949 adjustment-code matrix",

"description": "Six-row matrix mapping Publication 525 wage inclusion, Form 1099-B broker basis patterns, Form 8949 checkbox families, and adjustment code B usage for RSU sales, cross-walked from IRS instructions as of June 2026.",

"creator": { "@type": "Organization", "name": "VestingStrategy.com Research" },

"datePublished": "2026-06-16",

"license": "https://creativecommons.org/licenses/by/4.0/",

"isAccessibleForFree": true,

"url": "https://www.vestingstrategy.com/guides/irs-pub-525-form-8949-avoid-rsu-double-taxation/#dataset-pub525-8949-adjustment-matrix",

"distribution": [

{

"@type": "DataDownload",

"encodingFormat": "text/html",

"contentUrl": "https://www.vestingstrategy.com/guides/irs-pub-525-form-8949-avoid-rsu-double-taxation/#dataset-pub525-8949-adjustment-matrix"

}

]

}

Pros and cons: manual basis vs software import

| Approach | Advantages | Disadvantages |

|---|---|---|

| Manual Form 8949 entry | Full control over vest FMV basis; audit trail from supplements | Time-consuming with many lots; easy to transpose digits |

| Broker CSV import + override | Faster proceeds entry; software calculates Schedule D | Import may silently keep $0 basis unless you edit column (e) |

| CPA-prepared return | Expert lot matching; handles multi-state sourcing | Cost; still requires you to supply supplements |

| RSU Tax Basis Adjuster tool | Instant phantom-gain math; educational | Not a filing substitute; confirm with statements |

Taken position: For employees with fewer than five RSU sale lots per year, manual Form 8949 entry with supplement PDFs open beats blind import—one afternoon of work prevents thousands in phantom tax. Above that volume, pay for CPA lot reconciliation or invest in lot-level tracking at sale time.

Working checklist

Verdict: wages on W-2, basis on Form 8949

Publication 525's RSU rule is simple in theory—vest FMV is wages, sale gain is everything after that—but payroll and brokerage systems were never wired together. The administrative failure mode is expensive: importing $0 basis taxes vest dollars twice.

Taken position: Treat Form 8949 as a reconciliation form, not a brokerage mirror. Spend one session mapping supplements to sale lots before tax software import. That single habit prevents the most costly RSU filing mistake and aligns your return with Publication 525's wage-first framework. Pair this guide with cost basis for equity compensation, RSU tax basis adjuster guide, and the RSU Tax Basis Adjuster calculator.

Form 8949 reconciles amounts reported on Form 1099-B with amounts you report on your return—precisely the bridge Publication 525's wage classification requires when brokers omit payroll basis.

Frequently Asked Questions

Does IRS Publication 525 require me to report RSU vesting on Form 8949?

Answer: No at vest—Publication 525 classifies vest FMV as wages on Form W-2. Form 8949 enters the picture when you sell shares, to report capital gain using vest FMV as basis.

Source: IRS Publication 525

What basis do I enter on Form 8949 for RSU shares?

Answer: Vest FMV per share × number of shares sold from that lot—the same amount Publication 525 treated as wages on Form W-2.

Source: Instructions for Form 8949

Why does my 1099-B show $0 cost basis if Publication 525 says I already paid tax?

Answer: Brokers report purchase price, which is $0 for standard RSUs. Vest FMV from payroll is your true basis—you enter it on Form 8949 column (e).

Source: Instructions for Form 1099-B

Is accepting $0 broker basis the same as double taxation?

Answer: Economically, yes. You already paid ordinary income tax on vest FMV via W-2 withholding. Reporting $0 basis on Form 8949 taxes those same dollars again as capital gain.

Source: IRS Publication 525; Instructions for Form 8949

Which Form 8949 box do I check for RSU sales?

Answer: Usually Part I Box B (short-term, basis not reported to IRS) or Part II Box E (long-term). Confirm against your 1099-B checkboxes each year.

Source: Instructions for Form 8949

What adjustment code fixes incorrect RSU basis?

Answer: Code B—"Basis reported to IRS was incorrect"—when the broker-reported basis does not include wage-layer FMV from vest.

Source: Instructions for Form 8949

Can I fix RSU double taxation after filing?

Answer: Consider Form 1040-X with corrected Form 8949 and equity supplements within the refund statute window.

Source: IRS About Form 1040-X

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| Publication 525 (2025) | IRS | irs.gov |

| Instructions for Form 8949 | IRS | irs.gov |

| Instructions for Form 1099-B | IRS | irs.gov |

| Instructions for Form W-2 | IRS | irs.gov |

| IRC Section 83 | Statute | law.cornell.edu |

Figure 1: Publication 525's wage layer (W-2) must feed Form 8949 basis so Schedule D taxes only post-vest appreciation—not vest dollars twice.

Disclaimer: This guide discusses general U.S. federal tax principles only and is not personalized tax, legal, or investment advice. Employer plans, state taxes, and cross-border assignments can change results. Confirm facts with the sources cited and a qualified tax professional.

Research note: Editorial refresh 16 June 2026 for irs publication 525 restricted stock units high-intent reporting queries—step-by-step Form 8949 basis adjustment to prevent RSU double taxation under Publication 525.

Footnotes

-

Instructions for Form 8949 — reconcile 1099-B with taxpayer reporting. irs.gov/instructions/i8949 ↩

-

Instructions for Form 8949 — holding period and checkbox selection. irs.gov/instructions/i8949 ↩