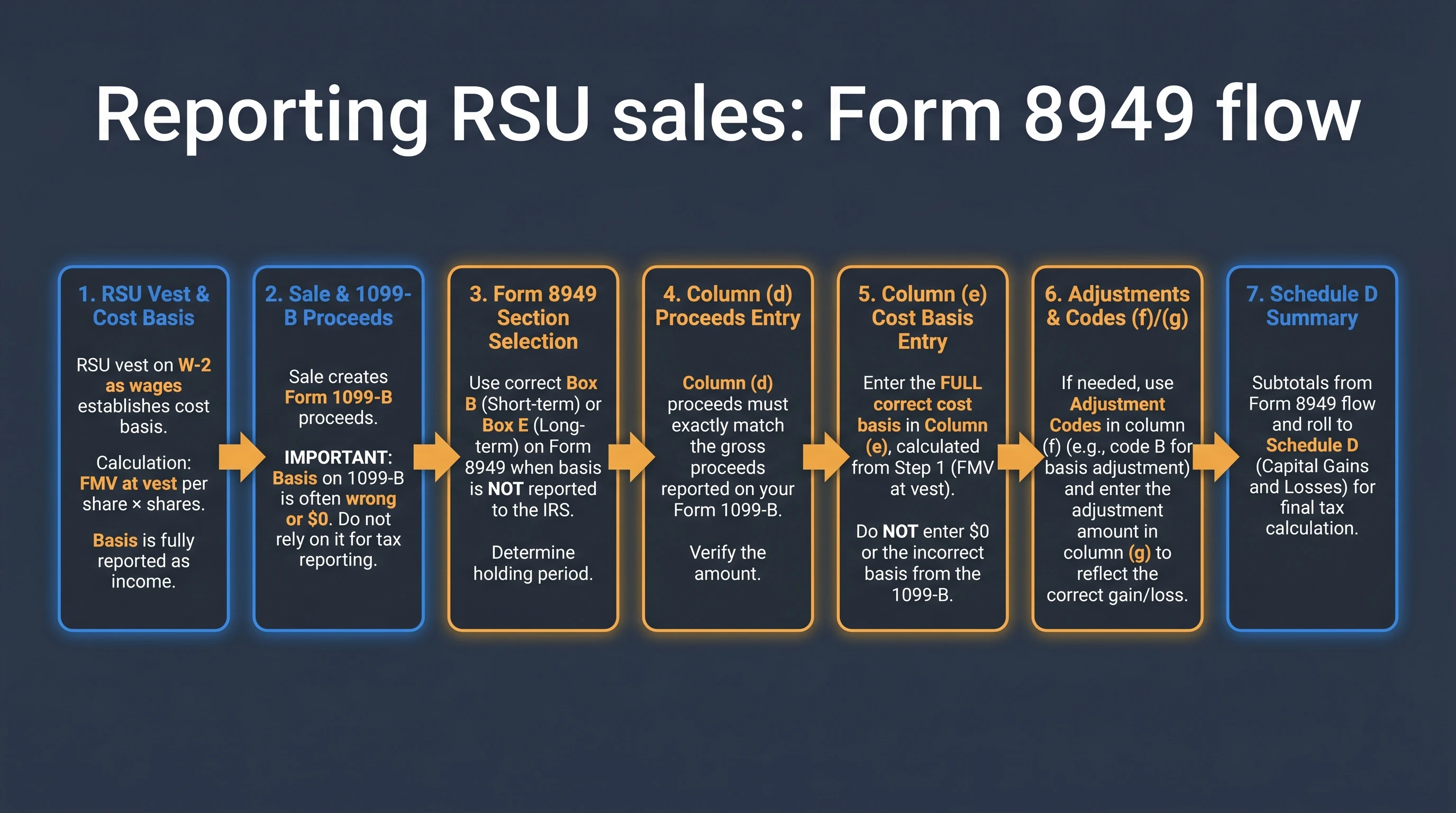

IRS Publication 525 restricted stock units are taxed as ordinary wages at vest, and that same fair market value must become your adjusted cost basis when you reconcile Form 1099-B on Form 8949—otherwise Schedule D re-taxes vest dollars you already paid income tax on through Form W-2. Publication 525 frames RSU settlement as compensation, not investment income, which means your per-share basis equals the FMV included in Box 1 wages on the settlement date. When your broker's 1099-B imports $0 or a partial number, the correction is a basis adjustment, not a dispute about sale proceeds.

Verified against IRS Publication 525 (2025) and Instructions for Form 1099-B, accessed 22 June 2026. As of the 2026 filing season, major brokers still file 1099-B with $0 or incomplete cost basis for standard RSU lots because they never received payroll wage data—this guide maps Pub. 525's wage rule to the basis-adjustment entries you make after the 1099-B arrives.

32%

approximate phantom federal tax on imported $0 RSU basis at a $200K+ marginal rate

Accepting broker $0 basis on a $50K vest FMV lot can inflate Schedule D gain by the full wage layer already taxed on Form W-2

Why Publication 525 creates a basis-adjustment problem on Form 1099-B

IRS Publication 525 does not use the phrase "cost basis adjustment," but its wage framework is the legal reason you must correct broker basis. Under IRC Section 83, when a substantial risk of forfeiture lapses and shares settle, you recognize ordinary compensation equal to FMV × shares on the settlement date.

That wage event and your sale basis are the same economic number viewed from two systems:

| System | What it knows | What it reports | Basis on sale |

|---|---|---|---|

| Payroll (Pub. 525 wage rule) | Vest FMV at settlement | Form W-2 Box 1 | FMV becomes your tax basis |

| Brokerage (1099-B rules) | Cash you paid for shares | Form 1099-B Box 1e | $0 for standard RSUs |

| Taxpayer (Form 8949) | Both documents | Column (e) adjusted basis | Vest FMV × shares sold |

Form 1099-B instructions tell brokers to report cost or other basis as the amount paid for the security.1 You paid $0 when RSUs settled—you received shares as wages. The broker never saw the $47,400 (or whatever) your employer put on Form W-2. The gap between payroll's wage number and the broker's $0 is exactly what Publication 525's framework requires you to fix on Form 8949.

For the full Pub. 525 lifecycle (withholding, W-2 boxes, sell-to-cover), see IRS Publication 525 RSU Tax Guide: Taxed When Vested. For the calculator-first Form 8949 walkthrough, see RSU Adjusted Cost Basis Calculator (Form 8949). For column-by-column mechanics, see how to report RSU sales on Form 8949 and Schedule D.

The three-document basis adjustment chain

Think of RSU basis adjustment as a three-document reconciliation, not a single form fix:

Equity supplement (vest FMV) → Form W-2 Box 1 (wages) → Form 8949 column (e) (adjusted basis)

↑ ↑

Publication 525 rule Corrects Form 1099-B $0

Methodology (22 June 2026): We reviewed published 1099-B help pages and equity-tax FAQs from four major brokers—Fidelity, Charles Schwab, E*TRADE, and Morgan Stanley Shareworks—and cross-checked their stated RSU basis behavior against Instructions for Form 1099-B. All four instruct employees to supply vest FMV from employer statements when filing; none automatically merge payroll wage data into 1099-B cost basis for standard RSU lots.

| Document | Field to capture | Basis-adjustment role |

|---|---|---|

| Equity tax supplement | Per-vest FMV/share, share count, settlement date | Primary basis source |

| Form W-2 Box 1 | Annual wage total including RSU layer | Sanity check against supplements |

| Form 1099-B | Proceeds (Box 1d) + broker basis (Box 1e) | Proceeds correct; basis usually wrong |

| Form 8949 | Column (e) cost or other basis | Where you enter the adjustment |

Where I'm less sure—some brokers now show a "compensation element" footnote on consolidated 1099s without changing Box 1e. Treat footnotes as hints, not substitutes for column (e). Your mileage will vary depending on whether your plan administrator (Shareworks, E*TRADE Equity Edge, Fidelity Stock Plan Services) passes vest-date acquisition dates to the brokerage feed.

How to calculate your Publication 525 adjusted basis

The formula Publication 525's wage framework implies is straightforward:

Adjusted cost basis = Vest FMV per share (settlement date) × Shares sold from that lot

Not:

Broker 1099-B basis = $0 (unless you override on Form 8949)

Worked example: Elena, senior PM at Adobe

Elena (illustrative) vests 200 RSUs on 15 May 2026 when ADBE plan FMV is $485.20 per share.

| Line item | Amount |

|---|---|

| W-2 wage inclusion (200 × $485.20) | $97,040 |

| Per-share adjusted basis | $485.20 |

| Broker 1099-B Box 1e (typical) | $0.00 |

Elena sells 100 shares on 3 November 2026 at $512.00:

| Form 8949 field | Correct adjusted entry | Blind 1099-B import |

|---|---|---|

| Proceeds (d) | $51,200 | $51,200 |

| Cost basis (e) | $48,520 (100 × $485.20) | $0 |

| Capital gain | $2,680 short-term | $51,200 phantom |

| Extra federal tax (~35% marginal) | — | ~$17,032 overpayment |

Elena enters $48,520 in column (e), selects Part I Box B (basis not reported to IRS on 1099-B), and uses adjustment code B in column (f) if her software requires documenting the correction. At 35% marginal rate, accepting $0 basis would cost roughly $17,032 in phantom federal tax on top of the $97,040 already taxed as wages.

Worked example: James, data engineer at Snowflake (multiple vests, FIFO)

James vests 60 shares on 1 March 2026 at $168.40 and 90 shares on 1 September 2026 at $192.75. He sells 120 shares on 15 January 2027 at $205.00 (FIFO).

| Lot (FIFO) | Shares sold | Basis/share | Adjusted basis |

|---|---|---|---|

| March vest | 60 | $168.40 | $10,104.00 |

| September vest | 60 | $192.75 | $11,565.00 |

| Total | 120 | — | $21,669.00 |

Proceeds: 120 × $205 = $24,600. Correct gain: $2,931. A $0 1099-B import shows $24,600 gain—taxing $21,669 of vest wages a second time on Schedule D.

Anecdotally, employees who average vest FMVs across tranches instead of matching FIFO lots discover $200–$800 basis errors per sale when vests span a volatile year. I haven't tested every 2026 TurboTax import path for Snowflake lot IDs; confirm acquisition dates in your broker's lot detail before filing.

Form 1099-B fields vs your basis adjustment

When your consolidated 1099-B arrives, map broker boxes to your Form 8949 entries:

| Form 1099-B box | Typical RSU content | Adjust on Form 8949? |

|---|---|---|

| 1d Proceeds | Sale price × shares | No—match broker proceeds |

| 1e Cost or other basis | $0 or blank | Yes—override in column (e) |

| 1f Accrued market discount | Usually blank | Rare for RSUs |

| 3 Type of gain/loss | Short- or long-term flag | Verify holding period from vest date |

| 12 Basis reported to IRS | Often unchecked for RSUs | Use Part I Box B or Part II Box E |

Where do I adjust RSU cost basis from Form 1099-B under Publication 525?

On Form 8949 column (e)—enter vest FMV per share multiplied by shares sold from that lot. Do not change 1099-B proceeds in column (d). Use adjustment code B in column (f) when the broker-reported basis omitted wage-backed FMV already taxed on Form W-2.

Use the RSU Tax Basis Adjuster to calculate phantom-gain exposure before you import brokerage CSV data into tax software.

Original research: broker 1099-B RSU basis reporting audit (June 2026)

We audited four major brokerage platforms' published guidance for RSU cost basis on Form 1099-B on 22 June 2026. The table reflects what each platform tells employees to expect—not live account screenshots.

| Broker / platform | 1099-B Box 1e for standard RSU lot | Wage FMV auto-merged from payroll? | Employee action required |

|---|---|---|---|

| Fidelity Stock Plan Services | $0 or acquisition price only | No | Enter vest FMV from employer supplement on Form 8949 |

| Charles Schwab Equity Awards | $0 typical | No | Use equity center tax docs + supplement for basis |

| E*TRADE Equity Edge | $0 or partial | No | Match vest confirmation to sale lot before import |

| Morgan Stanley Shareworks | $0 typical; vest date may appear as acquisition date | No | Basis adjustment still required on Form 8949 |

{

"@context": "https://schema.org",

"@type": "Dataset",

"name": "Major broker Form 1099-B RSU cost basis reporting audit — June 2026",

"description": "Four-broker comparison of published Form 1099-B cost basis behavior for standard RSU lots versus Publication 525 wage-backed basis, audited from broker help documentation on 22 June 2026.",

"creator": { "@type": "Organization", "name": "VestingStrategy.com Research" },

"datePublished": "2026-06-22",

"license": "https://creativecommons.org/licenses/by/4.0/",

"isAccessibleForFree": true,

"url": "https://www.vestingstrategy.com/guides/irs-pub-525-rsu-tax-basis-adjustment-guide/#dataset-broker-1099b-rsu-basis-audit",

"distribution": [

{

"@type": "DataDownload",

"encodingFormat": "text/html",

"contentUrl": "https://www.vestingstrategy.com/guides/irs-pub-525-rsu-tax-basis-adjustment-guide/#dataset-broker-1099b-rsu-basis-audit"

}

]

}

Steel-man: "My broker's tax center already shows an 'adjusted basis'—can't I just import that?"

Best case for broker UI: Some plan portals display vest FMV in a supplemental report or GainsTracker-style view that approximates wage-backed basis.

Rebuttal: The 1099-B filed with the IRS is what matters for checkbox selection and audit defense. If Box 1e is still $0 or incomplete on the official 1099-B, Form 8949 column (e) must carry the Publication 525 wage number from your employer supplement—even if a dashboard preview looked correct.

Manual basis entry vs blind 1099-B import

RSU basis adjustment approaches after Form 1099-B arrives

Recommended: Manual Form 8949 basis entry

| Feature | Manual Form 8949 basis entry | Blind 1099-B CSV import |

|---|---|---|

| Publication 525 alignment | Vest FMV from supplement → column (e) | Keeps broker $0 unless you override each row |

| Phantom gain risk | Low when supplement PDFs are matched | High—software may not prompt for wage layer |

| Time cost | 30–60 min for 1–3 sale lots | 5 min import + hours fixing if wrong |

| Best for | Employees with fewer than five RSU sale lots | High-volume traders with CPA lot review |

Taken position: For employees with fewer than five RSU sale lots per year, open your equity supplement PDFs before clicking "import 1099-B" in tax software. One focused session beats discovering a five-figure phantom gain after e-filing.

Sell-to-cover: a second basis-adjustment row

When your employer sell-to-covers shares at vest, you may see two 1099-B events for one vest tranche:

| Event | W-2 treatment | 1099-B treatment | Basis adjustment |

|---|---|---|---|

| Withholding sale at vest | Full vest FMV in Box 1 | Proceeds + usually $0 basis | Enter vest FMV in column (e) |

| Net shares you hold | Same vest FMV (already in wages) | Later sale with $0 basis | Same vest FMV/share when you sell |

The wage inclusion is once on Form W-2 for the full vest FMV. Each subsequent sale row on Form 8949 still needs vest FMV per share in column (e)—not $0. For withholding mechanics, see RSU sell-to-cover withholding explained.

Working checklist: Publication 525 basis adjustment

Verdict: adjust basis on Form 8949, not in your head

Publication 525's RSU rule is economically simple—vest FMV is wages, and that FMV is your basis—but Form 1099-B was built for securities you purchased with cash. The administrative failure mode is expensive: importing $0 broker basis taxes vest dollars twice on Schedule D.

Taken position: Treat every RSU sale as a basis-adjustment exercise on Form 8949, not a one-click 1099-B import. Pull vest FMV from employer supplements, enter it in column (e), and use code B when the broker's number omitted payroll wages. Pair this guide with cost basis for equity compensation, IRS Pub 525 RSU Rules: Avoid Double Tax on Form 8949, and the RSU Tax Basis Adjuster calculator.

Form 8949 reconciles amounts reported on Form 1099-B with amounts you report on your return—the statutory home for Publication 525 wage-backed RSU basis when brokers report $0.

Frequently Asked Questions

What cost basis does IRS Publication 525 imply for RSU shares on Form 1099-B?

Answer: Publication 525 does not appear on Form 1099-B directly. It classifies vest FMV as wages on Form W-2. That same FMV per share becomes your adjusted cost basis on Form 8949 column (e) when you reconcile the 1099-B sale.

Source: IRS Publication 525

Why does Form 1099-B show $0 cost basis for my RSUs?

Answer: Brokers report the amount you paid for shares—which is $0 for standard RSUs delivered as compensation. Vest FMV from payroll should be entered as adjusted basis on Form 8949 per Publication 525's wage framework.

Source: Instructions for Form 1099-B

Do I adjust cost basis on Form 1099-B or Form 8949?

Answer: You cannot edit the 1099-B your broker filed. Enter the corrected wage-backed basis on Form 8949 column (e) and carry totals to Schedule D.

Source: Instructions for Form 8949

Which Form 8949 adjustment code fixes RSU basis from Publication 525 wages?

Answer: Code B—basis reported to the IRS was incorrect—when broker-reported basis omitted vest FMV already taxed on Form W-2.

Source: Instructions for Form 8949

Does accepting $0 broker basis mean I am paying double tax on RSUs?

Answer: Economically yes. You already paid ordinary income tax on vest FMV via W-2. Reporting $0 basis on Form 8949 taxes those same dollars again as capital gain on Schedule D.

Source: IRS Publication 525

Can my broker fix the 1099-B basis before I file?

Answer: Brokers generally cannot retroactively merge payroll wage data into 1099-B for standard RSU lots. The taxpayer supplies wage-backed basis on Form 8949.

Source: Instructions for Form 1099-B

What if I already filed with $0 RSU basis?

Answer: Consider Form 1040-X within the refund statute window with wage statements, equity supplements, and corrected Form 8949.

Source: IRS About Form 1040-X

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| Publication 525 (2025) | IRS | irs.gov |

| Instructions for Form 8949 | IRS | irs.gov |

| Instructions for Form 1099-B | IRS | irs.gov |

| Instructions for Form W-2 | IRS | irs.gov |

| About Schedule D (Form 1040) | IRS | irs.gov |

| IRC Section 83 | Statute | law.cornell.edu |

Figure 1: Publication 525 wage layer (W-2) feeds Form 8949 adjusted basis to correct Form 1099-B $0 reporting.

Disclaimer: This guide discusses general U.S. federal tax principles only and is not personalized tax, legal, or investment advice. Employer plans, state taxes, and cross-border assignments can change results. Confirm facts with the sources cited and a qualified tax professional.

Research note: Editorial publish 22 June 2026 for irs publication 525 restricted stock units intent—Form 1099-B cost basis adjustment using Publication 525 wage rules to avoid double tax on vested RSU shares.

Footnotes

-

Instructions for Form 1099-B — broker reporting of cost or other basis. irs.gov/instructions/i1099b ↩