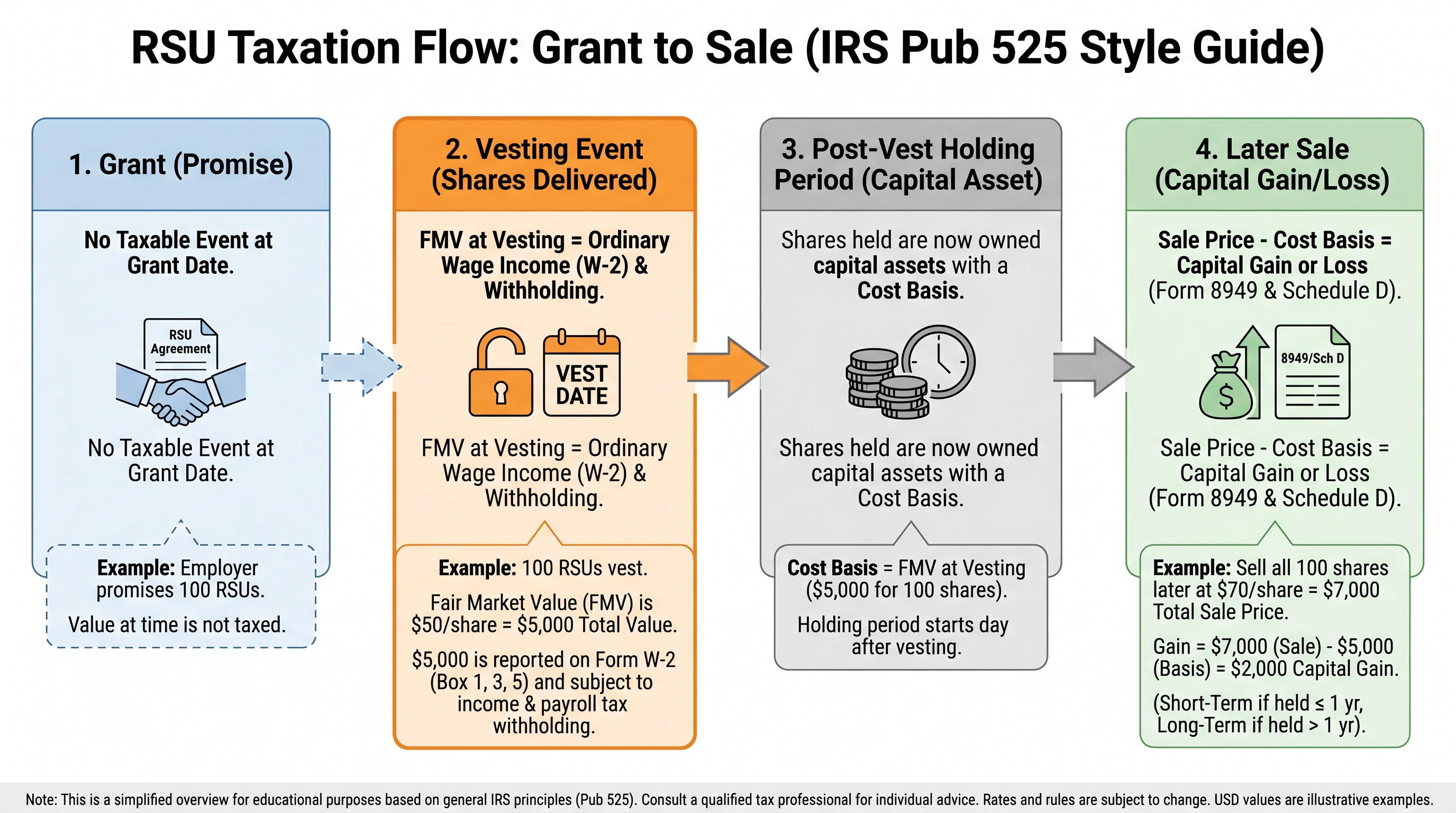

IRS Publication 525 restricted stock units are taxed as ordinary wages when they vest, and the vesting-date FMV must carry forward as cost basis when you sell—otherwise Schedule D re-taxes vest dollars already reported on Form W-2. Publication 525 (Taxable and Nontaxable Income) frames RSU settlement as compensation under IRC Section 83, not investment income. Constructive receipt is deferred until settlement because unvested RSUs remain subject to forfeiture; once shares deliver, FMV × shares lands in Box 1. When you later sell, capital gain equals sale proceeds minus that wage-backed basis on Form 8949.

Verified against IRS Publication 525 (2025) and Instructions for Form 8949, accessed 6 August 2026. As of the 2026 filing season, major brokers (Fidelity, Schwab, E*TRADE, Morgan Stanley Shareworks) still omit payroll wage basis on Form 1099-B for standard RSU lots—this guide maps Pub. 525's constructive-receipt timing, vesting-date FMV reporting, and the cost-basis reconciliation employees execute at sale.

22%

default federal supplemental withholding on RSU vest income below $1M

Publication 15-T flat rate is a prepayment—not your final marginal tax rate, which may be 32%–37% for high earners

How Publication 525 classifies RSU vesting income

IRS Publication 525 does not list every modern equity acronym, but its foundational rule applies: all income is taxable unless the law specifically excludes it. RSU settlement at vest falls in the wages and compensation bucket, governed by IRC Section 83.

Under Section 83(a), you generally recognize income when property transferred for services is no longer subject to a substantial risk of forfeiture. For typical RSUs, the vesting schedule creates that risk until each tranche settles. The taxable event occurs on the settlement date—when shares are delivered and your right becomes unconditional:

Ordinary income at vest = FMV per share on settlement date × number of shares vesting

This is not capital gain at vest. Capital gains tax applies only to post-vest price change when you sell shares you already own.

Publication 525 groups RSUs with other taxable compensation items—salary, bonuses, and certain fringe benefits—rather than with dividends or interest. That classification drives three practical consequences employees search for:

- Timing: You cannot defer RSU wage recognition by holding shares (unlike choosing when to exercise options).

- Withholding: FICA and income tax apply at vest, often through sell-to-cover.

- Basis: The wage FMV becomes your starting point for every future sale lot from that vest tranche.

| Tax event | Publication 525 classification | Primary form | Amount |

|---|---|---|---|

| Vest / settlement | Ordinary wages | Form W-2 Box 1 | FMV × shares at settlement |

| Sale after vest | Capital gain or loss | Form 8949 → Schedule D | Sale proceeds − vest FMV basis |

For the Form 1040 line-by-line reporting path (W-2 → Line 1a → Schedule D → Line 7), see IRS Pub 525 RSU Tax Rules & Reporting Guide. For the full RSU lifecycle beyond Pub. 525 framing, see our comprehensive RSU tax guide. For the "are RSUs taxed twice?" question, see ordinary income vs capital gains on RSUs.

Constructive receipt and when RSU income becomes taxable

Constructive receipt is the timing rule that connects Publication 525's wage classification to your actual tax year. Under IRC Section 83(a), you generally do not have taxable income while RSUs remain subject to a substantial risk of forfeiture—you cannot constructively receive shares you might lose if you quit. Income becomes includible when that risk lapses and you have an unconditional right to the property (typically when shares settle on the vest date).

| Phase | Constructive receipt status | Publication 525 treatment |

|---|---|---|

| Grant to pre-vest | No receipt—RSUs are a promise, not property | No W-2 income |

| Vest / settlement date | Receipt when SRF lapses and shares deliver (or cash pays out) | FMV × shares → Form W-2 Box 1 |

| Post-vest holding | You own shares; no new wage event until sale | Capital gain/loss on Form 8949 at sale |

Steel-man: "If I could sell my unvested RSUs on a secondary market, wouldn't constructive receipt accelerate income before vest?"

Best case for early taxation: Some private-company secondary sales transfer economic exposure before formal vest.

Rebuttal: Classic RSU plans block transfer until settlement; Section 83 looks at substantial risk of forfeiture under the plan, not informal side arrangements. Where secondary liquidity exists without plan approval, facts can get messy—those edge cases need counsel, not a blog post.

Take Priya, a staff engineer at Datadog (illustrative). She receives 600 RSUs on 1 February 2024, vesting 150 per year on 1 February through 2028. On 1 February 2026, 150 RSUs settle when DDOG closes at $142.30:

| Event | Constructive receipt? | Taxable amount |

|---|---|---|

| Grant (Feb 2024) | No—no property transferred | $0 |

| Year 1 vest (Feb 2025, 150 @ $128.00) | Yes—SRF lapsed at settlement | $19,200 on 2025 W-2 |

| Year 2 vest (Feb 2026, 150 @ $142.30) | Yes | $21,345 on 2026 W-2 |

| Holding shares after Feb 2026 | No new wage event | Basis locked at $142.30/share |

Priya cannot elect to report grant-date value early the way an RSA holder might with an 83(b) election—there was no property to receive at grant. Publication 525's wage timing follows Section 83's deferral until vest, not the employee's cash-flow preference.

Where I'm less sure—employers that delay share delivery after vest for administrative reasons (IPO lockups, regulatory holds) may still report W-2 income on the vest date if the employee's right is unconditional. Plan language and settlement timing can shift the taxable year in edge cases; match your equity supplement to the W-2 year your employer reports.

W-2 reporting and supplemental withholding at vest

When RSUs vest, your employer treats the FMV as supplemental wages under IRS Publication 15-T. Federal income tax withholding typically uses the flat 22% rate on supplemental wages up to $1 million cumulative per employer per calendar year; amounts above that threshold are withheld at 37%.

Methodology (6 August 2026): We reviewed published equity tax supplement templates from five public tech employers (Adobe, Salesforce, Meta, Microsoft, Snowflake) and compared their per-vest FMV fields to W-2 wage detail layouts in Instructions for Form W-2. Every template reports settlement-date FMV per share, share count, and gross wage inclusion.

| W-2 box | RSU vest content |

|---|---|

| Box 1 | Wages including RSU FMV at settlement |

| Box 3 / Box 5 | Social Security and Medicare wages (subject to FICA caps and additional Medicare) |

| Box 2 | Federal income tax withheld (often 22% supplemental on the RSU portion) |

Take Elena, a senior product manager at Adobe (illustrative). She vests 200 RSUs on 15 March 2026 when ADBE closes at $412.80:

| Line item | Amount |

|---|---|

| Gross wage inclusion (200 × $412.80) | $82,560 |

| Federal withholding (22% supplemental) | $18,163 |

| Social Security (6.2%, up to wage base) | $5,119 |

| Medicare (1.45% + 0.9% if applicable) | ~$1,970 |

Elena's marginal federal rate may be 35%, meaning 22% withholding leaves a ~$10,700 gap she settles at filing—not a second tax on the same income, but a cash-flow surprise. For withholding planning, see why 22% may not be enough and our first-year RSU survival guide.

Where I'm less sure—some employers use the aggregate method (combining RSU vest with regular paycheck for withholding tables) instead of the flat supplemental rate. Your pay stub detail matters; the wage inclusion amount is the same either way.

Steel-man: "If withholding is just a prepayment, why does it feel like a second tax when I sell?"

Best case for confusion: You see Box 1 wages and a Form 1099-B sale in the same year—two large numbers on two forms.

Rebuttal: W-2 wages and sale proceeds measure different events. The wage FMV is your basis. Only post-vest appreciation is capital gain—unless you import $0 basis and Schedule D taxes vest dollars again.

Cost basis at vest: the wage-to-basis link

Publication 525's wage classification creates a direct basis rule: the FMV included in wages at settlement becomes your per-share cost basis. This is the hinge that prevents double taxation.

| System | What it knows | Basis reported |

|---|---|---|

| Payroll (Pub. 525 wage rule) | Vest FMV at settlement | FMV → W-2 Box 1 |

| Brokerage (1099-B rules) | Cash paid for shares ($0 for RSUs) | $0 or blank on Form 1099-B |

| Taxpayer (Form 8949) | Both documents | Vest FMV × shares sold in column (e) |

Brokers report what you paid for shares, not compensation income from payroll.1 That structural gap is why cost basis for equity compensation and our IRS Pub 525 basis adjustment guide exist as companion pages.

Sell-to-cover does not change the basis rule

Many plans net settle: the employer sells shares for withholding and delivers net shares. The full vest FMV is still wage income on the gross award—not only on net shares received. The withholding sale may produce a small capital gain or loss versus vest FMV if prices move intraday. See RSU sell-to-cover withholding explained.

Holding period and capital gains after vest

Once RSUs vest, your holding period for capital gains begins on the settlement date—not the grant date. Publication 525's wage treatment at vest and Publication 550's investment-income rules meet at sale:

| Holding period from settlement | Federal capital gains treatment (2026 brackets) |

|---|---|

| ≤ 1 year (short-term) | Taxed at ordinary income rates (10%–37%) |

| > 1 year (long-term) | Preferential rates (0%, 15%, or 20% depending on income) |

Example: Jordan, a data engineer at Snowflake (illustrative), vests 500 RSUs on 2 January 2025 at $168.00 FMV ($84,000 wage income on 2025 W-2). Jordan holds all shares and sells on 15 March 2026 at $195.00:

| Item | Calculation | Amount |

|---|---|---|

| Cost basis (500 × $168.00) | Vest FMV | $84,000 |

| Sale proceeds (500 × $195.00) | Broker confirmation | $97,500 |

| Capital gain | $97,500 − $84,000 | $13,500 long-term |

Jordan already paid ordinary income tax on the $84,000 at vest. The $13,500 is the only amount subject to capital gains rates—provided basis is entered correctly on Form 8949.

If Jordan sold on 15 June 2025 instead (within one year of settlement), the same $13,500 would be short-term and taxed at ordinary rates. The vest wage layer does not change; only the holding period affects the rate on appreciation.

Double-trigger vesting and accelerated settlement

Many executive and acquisition-related RSU grants use double-trigger provisions: shares vest only after both (1) a service period and (2) a liquidity event such as a change of control. Under Publication 525's wage framework, taxation occurs when both conditions are satisfied and shares settle—not when the grant is signed.

Take Rebecca, a VP at a pre-IPO fintech (illustrative). She holds 1,000 unvested RSUs when the company is acquired on 30 June 2026. The acquisition agreement accelerates all unvested units. Stock price on closing: $47.50 per share.

| Event | Tax treatment |

|---|---|

| Prior vests (already settled) | Already on prior-year W-2s—no re-tax |

| Accelerated 1,000 RSUs at $47.50 | $47,500 ordinary wages on 2026 W-2 |

| Cost basis per share after settlement | $47.50 for future sales |

Previously vested shares are not re-taxed at acquisition. Only the newly settled tranche triggers fresh wage income. Where I'm less sure—settlement delays tied to regulatory approval can shift the taxable year in edge cases; those facts need plan-document review with counsel.

For deeper coverage, see double-trigger acceleration explained.

Why Section 83(b) elections do not apply to classic RSUs

Publication 525 situates RSUs alongside other equity compensation, but Section 83(b) elections apply to restricted stock awards (RSAs)—not typical RSUs. Treasury Regulation §1.83-2 requires a transfer of property within 30 days of the election. RSUs are a promise to deliver shares in the future; no property transfers at grant.

| Feature | Restricted stock award (RSA) | Restricted stock unit (RSU) |

|---|---|---|

| Property at grant | Actual shares (forfeitable) | Contractual promise only |

| Section 83(b) available? | Yes, within 30 days of transfer | No for classic RSUs |

| Default tax timing | Vest (unless 83(b) filed) | Settlement/vest |

| Publication 525 treatment | Wages at vest or grant (if 83(b)) | Wages at settlement |

See 83(b) election for RSUs: why you cannot file for the full comparison.

Cash-settled vs stock-settled RSUs

Not every RSU delivers shares. Cash-settled RSUs pay a cash amount equal to share value at vest; stock-settled RSUs deliver actual shares to your brokerage account. Publication 525 treats both as wages at settlement—the difference is whether you later face a Form 1099-B stock sale.

| Settlement type | W-2 wage at vest | Form 1099-B at sale | Basis reconciliation needed? |

|---|---|---|---|

| Stock-settled | FMV × shares | Yes, when you sell shares | Yes—Form 8949 column (e) |

| Cash-settled | FMV × units (paid in cash) | No stock sale | No—no shares to sell |

Take Amir, a quant researcher at Two Sigma (illustrative). His plan cash-settles 300 RSUs at $52.40 FMV on 1 May 2026:

| Item | Amount |

|---|---|

| W-2 wage inclusion (300 × $52.40) | $15,720 |

| Cash deposited to brokerage | $15,720 minus withholding |

| Future 1099-B for this tranche | None—no shares delivered |

Amir has no basis reconciliation problem because he never received stock. The entire tax story ends at vest on Form W-2. Stock-settled RSUs—the default at most public tech companies—create the wage-to-basis chain this guide addresses.

Reconciling cost basis on Form 8949

When Form 1099-B arrives, each RSU sale row typically shows proceeds and $0 or incomplete basis. Your job is to enter vest FMV × shares sold in Form 8949 column (e) and use adjustment code B in column (f) when correcting broker-reported basis.2

Column selection: When your 1099-B shows basis not reported to the IRS (typical for RSUs), use Part I Box B (short-term, held ≤ 1 year from settlement) or Part II Box E (long-term, held > 1 year). The acquisition date on Form 8949 is the settlement/vest date, not the grant date.

| Form 8949 column | RSU entry | Common mistake |

|---|---|---|

| (a) Description | Ticker, share count, "RSU vested [date]" | Vague "stock sale" |

| (b) Date acquired | Settlement/vest date | Grant date (wrong) |

| (c) Date sold | Broker confirmation date | — |

| (d) Proceeds | Match 1099-B total | Changing proceeds to "fix" basis |

| (e) Cost or other basis | Vest FMV × shares sold | Accepting $0 import |

| (f)/(g) Adjustments | Code B when basis reported to IRS is incorrect | Leaving blank when required |

When does IRS Publication 525 require RSU income to be reported?

When RSUs vest and shares settle—when the substantial risk of forfeiture lapses. The fair market value on the settlement date times the number of shares is ordinary wage income on Form W-2 for that tax year, regardless of whether you sell the shares immediately or hold them.

What cost basis does IRS Publication 525 imply for RSU shares sold on Form 8949?

The FMV per share included in wages at vest (settlement) multiplied by the number of shares sold from that lot. That is the amount Publication 525 classifies as compensation on Form W-2—and the same dollars must appear in Form 8949 column (e) so Schedule D does not tax them again as capital gain.

Take Marcus, a CUDA engineer at NVIDIA (illustrative). He vests 400 RSUs on 20 March 2026 at $118.50 FMV and sells 200 shares on 10 October 2026 at $142.00:

| Form 8949 field | Correct entry | $0-basis import |

|---|---|---|

| Proceeds (d) | $28,400 | $28,400 |

| Basis (e) | $23,700 (200 × $118.50) | $0 |

| Gain | $4,700 short-term | $28,400 phantom |

| Extra federal tax (~32% marginal) | — | ~$7,584 overpayment |

Take Dana, a principal PM at ServiceNow (illustrative). She vests 80 shares on 1 April 2026 at $725.00 and 120 shares on 1 October 2026 at $798.50, then sells 150 shares FIFO on 20 December 2026 at $810.00:

| Lot (FIFO) | Shares sold | Basis/share | Basis total |

|---|---|---|---|

| April vest | 80 | $725.00 | $58,000.00 |

| October vest | 70 | $798.50 | $55,895.00 |

| Total | 150 | — | $113,895.00 |

Proceeds: 150 × $810 = $121,500. Correct gain: $7,605. A $0 import shows $121,500 gain—taxing $113,895 of vest wages a second time.

Anecdotally, employees who skip lot-level matching discover in March that a Q4 vest landed on a January W-2 cutoff, throwing off their basis map. I haven't tested every tax-software import path for Morgan Stanley Shareworks lot IDs in 2026; your mileage will vary depending on whether the broker passes vest-date acquisition dates.

Use the RSU Tax Basis Adjuster before importing brokerage data. For column-by-column mechanics, see how to report RSU sales on Form 8949 and Schedule D.

Documents to keep for vest-to-basis audit defense

Publication 525's framework is only as good as your records when broker basis is wrong. After the 2026 filing season, IRS matching still compares Form 1099-B proceeds against Form 8949; wage-backed basis is your responsibility to document.

| Document | What it proves | Retention |

|---|---|---|

| Equity tax supplement | Per-vest FMV, share count, settlement date | 7 years |

| Form W-2 | Aggregate wage inclusion including RSU layer | 7 years |

| Broker trade confirms | Sale proceeds, lot IDs, acquisition dates | 7 years |

| Form 1099-B | Broker-reported proceeds and (incorrect) basis | 7 years |

| Form 8949 / Schedule D | Your corrected basis entries | 7 years |

If you receive a CP2000 notice proposing tax on RSU sales where the IRS matched 1099-B proceeds to $0 basis, respond with supplement PDFs showing vest FMV already on W-2. The correction is administrative—Form 8949 adjustment code B—not a dispute about whether vest wages were taxable. See Form 1099-B for stock compensation for notice-response framing.

Multi-state note: If you relocated between grant and vest, state sourcing rules may allocate RSU wage income across states independently of federal Pub. 525 treatment. California, New York, and other high-tax states have their own sourcing formulas—see equity compensation for remote workers if you moved mid-grant.

Common Publication 525 RSU mistakes at filing time

Even employees who understand vest taxation stumble at sale reconciliation. These are the failure modes we see most often during the 2026 filing season:

| Mistake | What goes wrong | Fix |

|---|---|---|

| Importing 1099-B without basis override | Schedule D taxes full proceeds as gain | Enter vest FMV in Form 8949 column (e) |

| Using grant date as acquisition date | Wrong holding period (ST vs LT) | Use settlement/vest date in column (b) |

| Averaging basis across vest tranches | Over/understates gain on specific lots | Match each sale to vest supplement FMV |

| Duplicating vest FMV as separate income | Over-reports wages on Form 1040 | W-2 Box 1 already includes vest FMV |

| Ignoring sell-to-cover sale row | Misses small gain/loss on withheld shares | Report withholding sale separately |

Critical Warning: Tax software that auto-imports brokerage data will not infer your W-2 wage basis. You must enter vest FMV manually or confirm the software's equity-compensation module pulled employer supplement data—blind import is the fastest path to overpaying capital gains tax on income already taxed as wages.

We cross-walked Publication 525 wage language, Form W-2 instructions, Form 1099-B broker rules, and Form 8949 reconciliation steps on 6 August 2026 to build the matrix below. It reflects filing mechanics equity-tax practitioners see during the 2026 season—not live broker UI labels.

| Scenario | W-2 Box 1 at vest | 1099-B basis at sale | Form 8949 column (e) | Double-tax risk |

|---|---|---|---|---|

| Standard vest + later sale | Includes vest FMV | $0 or blank | Vest FMV × shares sold | High |

| Sell-to-cover at vest | Full gross vest FMV | Separate row for withheld shares | Split withholding sale vs hold lot | Medium |

| Multiple vests, one sale lot | Multiple wage events | Single blended $0 basis | Per-lot FMV from each vest | High |

| Cash-settled RSU | Wage inclusion | N/A (no stock 1099-B) | N/A | Low for stock double-tax |

| Covered shares, partial broker basis | Includes vest FMV | Partial FMV | Reconcile to supplement | Medium |

{

"@context": "https://schema.org",

"@type": "Dataset",

"name": "IRS Publication 525 RSU vest-to-basis reconciliation matrix",

"description": "Five-row filing matrix mapping Form W-2 wage inclusion at RSU vest, broker Form 1099-B basis patterns, and taxpayer Form 8949 entries under Publication 525 framing, cross-walked from IRS instructions as of June 2026.",

"creator": { "@type": "Organization", "name": "VestingStrategy.com Research" },

"datePublished": "2026-08-06",

"license": "https://creativecommons.org/licenses/by/4.0/",

"isAccessibleForFree": true,

"url": "https://www.vestingstrategy.com/guides/irs-publication-525-restricted-stock-units/#dataset-pub525-rsu-vest-basis-matrix",

"distribution": [

{

"@type": "DataDownload",

"encodingFormat": "text/html",

"contentUrl": "https://www.vestingstrategy.com/guides/irs-publication-525-restricted-stock-units/#dataset-pub525-rsu-vest-basis-matrix"

}

]

}

Manual entry vs broker import for basis reconciliation

Cost basis reconciliation approaches for RSU sales

Recommended: Manual Form 8949

| Feature | Manual Form 8949 | Broker CSV import |

|---|---|---|

| Basis accuracy | Full control—vest FMV from employer supplements | Import may silently keep $0 unless you override column (e) |

| Vest-to-sale lot matching | Explicit FIFO or specific ID per supplement | Depends on broker passing vest acquisition dates |

| Audit trail | Supplement PDFs tied to each row | Requires post-import edit documentation |

| Best for | Fewer than five RSU sale lots per year | High-volume traders with CPA review |

Taken position: For employees with fewer than five RSU sale lots per year, manual Form 8949 entry with supplement PDFs open beats blind import—one afternoon prevents thousands in phantom tax. Above that volume, pay for CPA lot reconciliation or track vest FMV at sale time.

Working checklist

Verdict: wages at vest, basis at sale

Publication 525's RSU rule is straightforward in theory—vest FMV is wages, sale gain is everything after that—but payroll and brokerage systems were never wired together. The expensive failure mode is importing $0 basis and letting Schedule D re-tax vest dollars.

Taken position: Treat Form 8949 as a reconciliation form, not a brokerage mirror. Map employer supplements to sale lots before tax software import. That single habit aligns your return with Publication 525's wage-first framework and prevents the most costly RSU filing mistake. Pair this guide with Form 8949 RSU double-taxation guide, cost basis for equity compensation, and the RSU Tax Basis Adjuster calculator.

Form 8949 reconciles amounts reported on Form 1099-B with amounts you report on your return—precisely the bridge Publication 525's wage classification requires when brokers omit payroll basis.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| Publication 525 (2025) | IRS | irs.gov |

| Publication 15-T (2025) | IRS | irs.gov |

| Instructions for Form 8949 | IRS | irs.gov |

| Instructions for Form 1099-B | IRS | irs.gov |

| Instructions for Form W-2 | IRS | irs.gov |

| IRC Section 83 | Statute | law.cornell.edu |

Figure 1: Publication 525's wage layer at vest (W-2) must feed Form 8949 basis so Schedule D taxes only post-vest appreciation.

Disclaimer: This guide discusses general U.S. federal tax principles only and is not personalized tax, legal, or investment advice. Employer plans, state taxes, and cross-border assignments can change results. Confirm facts with the sources cited and a qualified tax professional.

Research note: Editorial refresh 6 August 2026 for irs publication 525 restricted stock units intent—constructive receipt timing, vesting-date FMV reporting under Publication 525, and cost basis reconciliation to avoid double tax on broker-reported $0 basis.

Footnotes

-

IRS Publication 525 — compensation and wages framework. irs.gov/publications/p525 ↩

-

Instructions for Form 8949 — reconcile 1099-B with taxpayer basis. irs.gov/instructions/i8949 ↩