California equity sourcing rules require you to split RSU and stock-option wage income between California and other states using service days in a defined lookback period—not simply your residence on the vest or exercise date. If you performed services in California during that period, the Franchise Tax Board (FTB) can tax a pro-rata share of compensation income even after you relocate to Texas, Washington, or abroad, subject to credits and your filing status.

Verified against FTB Publication 1004 (Rev. 11-2023) and IRS Publication 525 (2025), accessed 25 May 2026. As of May 2026, core California sourcing mechanics for equity compensation have not changed in the FTB materials we reviewed—proposed wealth taxes and PTET extensions are separate from day-based wage sourcing.

13.3%

top California PIT rate (including Mental Health Services Tax over $1M)

Illustrative marginal stack on large equity vests for high earners—federal and payroll taxes are additional

California sources stock option and restricted stock wage income using the ratio of California workdays to total workdays during the applicable period—not only where you live when shares vest or you exercise.

How California sourcing differs from “where I live today”

Equity sourcing answers which state may tax the wage layer of your RSU vest or option exercise. Residency answers whether you are a California resident for the year and therefore potentially taxable on worldwide income. Relocation guides often blur the two; California audits frequently start by reconciling payroll residency flags against day logs.

| Concept | What it controls | Typical mistake |

|---|---|---|

| Residency | Full-year vs part-year vs nonresident return | Assuming Texas domicile ends California wage sourcing on old grants |

| Sourcing | Percent of wage income allocated to CA | Counting only days in the vest year, not the full performance period |

| Withholding | Cash withheld on paycheck | Treating flat supplemental rates as your true California liability |

For the multi-state frame, pair this guide with state income tax nexus for remote workers and equity compensation for remote workers. If FTB matching notices are the concern, read California FTB equity audits: multi-state RSU sourcing. For the Source Day formula and step-by-step math, read California Source Day Formula for RSUs & Stock Options; this article is the relocation-first deep dive tied to the calculator.

Original research: allocation period matrix (FTB Pub 1004 framing)

Methodology (25 May 2026): We extracted the workday-ratio examples and period labels from FTB Publication 1004 (Rev. 11-2023), normalized them into a single comparison matrix, and mapped each row to the inputs our California Equity Source Days Calculator expects (total wage income, California days, total days). We did not re-interpret unpublished FTB private letter rulings—employer payroll vendors sometimes use different day conventions.

| Equity type | Income event (wage layer) | Period in Pub 1004 examples | Calculator inputs |

|---|---|---|---|

| RSUs / restricted stock | FMV at vest (less amount paid, if any) | Purchase/grant → vesting | CA days & total days over same window |

| NSOs | Spread at exercise (FMV − strike) | Grant → exercise | Same; income = spread dollars |

| ISOs (qualifying) | No regular wage at exercise | N/A for wage sourcing at exercise | AMT adjustment is federal; CA taxes ISO spread at exercise for state purposes in many cases |

| ISOs (disqualifying) | Wage income on disqualifying disposition | Facts-specific; often exercise-to-sale overlap | Treat like wage event; confirm with CPA |

| Sale after vest/exercise | Capital gain/loss | Residency at sale matters for residents | Sourcing of prior wage layer already fixed |

Source: FTB Publication 1004 equity compensation sections; see Primary Sources table below.

RSUs: mid-vest relocation and the service-day fraction

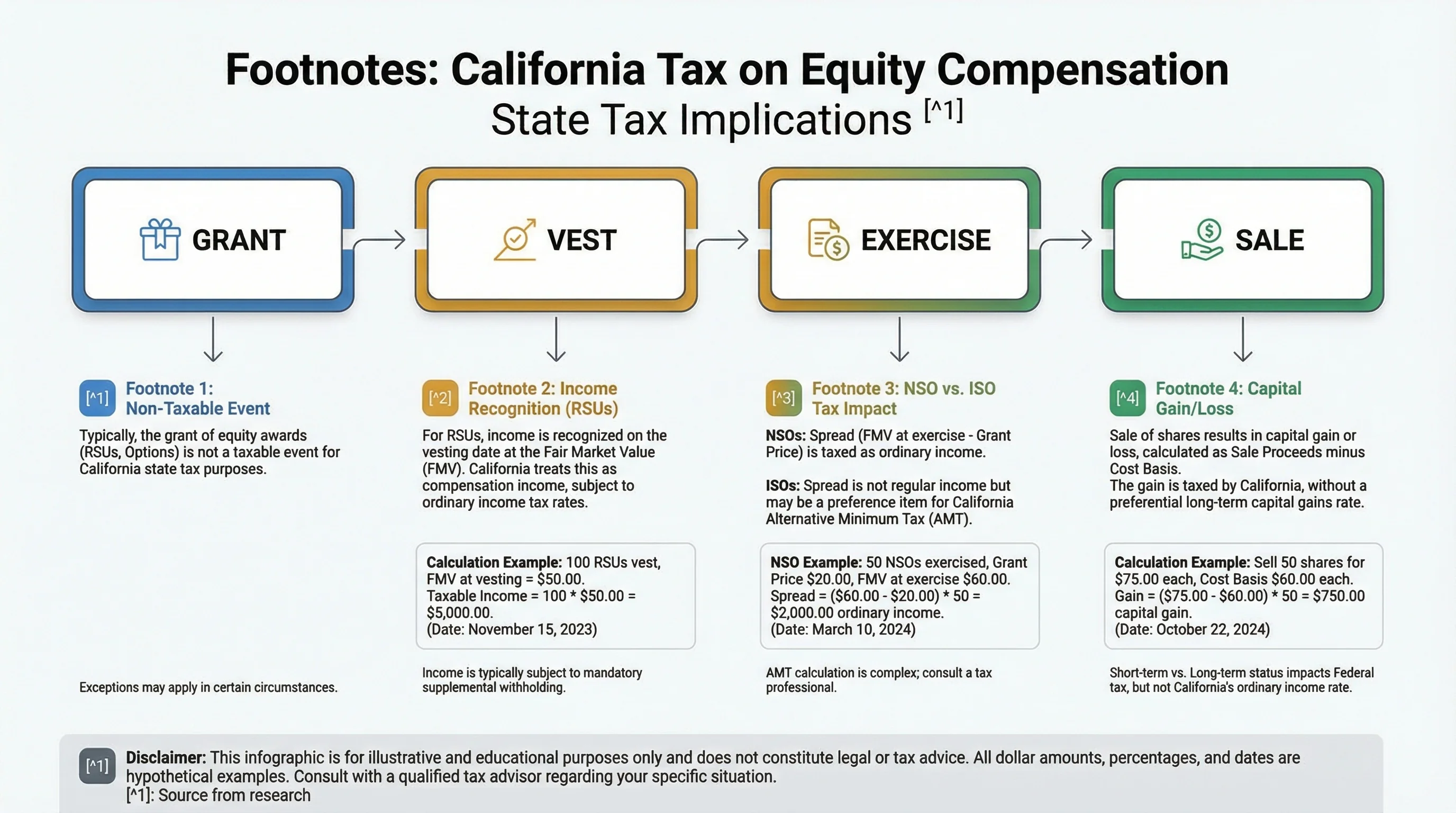

When RSUs vest through U.S. payroll, the fair market value at settlement is generally ordinary wages for federal and California purposes under IRC Section 83. California then asks: what fraction of those wages relate to services performed in California during the vesting period?

Worked example — Priya, Stripe → Austin

Scenario (illustrative, not Stripe payroll advice): Priya received 4,000 RSUs in March 2022 while working in San Francisco. She relocated to Austin on 1 October 2025. 1,000 RSUs vest on 15 March 2026 at $85 per share ($85,000 wage income).

| Input | Value |

|---|---|

| Total service days (grant → vest) | 1,000 |

| California service days | 700 |

| California sourcing ratio | 70% |

| California-sourced wages | $59,500 |

Priya may be a Texas resident in 2026, but California can still assert tax on the $59,500 sourced portion (and she may seek a credit in Texas for taxes paid to other states—Texas has no income tax, so there is no automatic offset). Where I'm less sure without her exact W-2: whether her employer’s payroll system used the same 1,000-day denominator or a calendar-year shortcut—mismatches between employer reporting and your return are common audit friction.

Run the ratio: California Equity Source Days Calculator with equity income 85000, CA days 700, total days 1000.

I moved out of California—why does FTB still tax my RSU vest?

Because California equity sourcing rules look at where you performed services while the RSU was earning out, not only where you live on vest day. If a large share of grant-to-vest workdays were in California, FTB can tax that percentage of vest wages even as a nonresident or part-year resident, reported on Form 540NR with appropriate credits.

Stock options: NSOs and ISOs on the move

Nonqualified stock options (NSOs)

NSOs generate wage income at exercise equal to the spread. Publication 1004’s NSO example uses grant date through exercise date for the day ratio. Relocating between grant and exercise splits the spread the same way RSUs split vest wages—only the event date and dollar base change.

Incentive stock options (ISOs)

ISOs add layers:

- Federal regular tax: Often no wage income at exercise if you meet ISO holding rules.

- Federal AMT: Bargain element may be an AMT preference item—see AMT planning for stock options.

- California: California does not conform to federal ISO deferral the same way; the spread at exercise can be California ordinary income even when federal wages look quiet.

Worked example — Marcus, Coinbase ISO exercise while part-year resident

Marcus exercised 2,000 ISOs in June 2026 (strike $12, FMV $48, spread $36/share, $72,000 California wage concept). He was a California resident January–April 2026, then Nevada resident. Grant-to-exercise workdays: 800 total, 500 in California → 62.5% California sourcing → $45,000 California-sourced wage income (illustrative). Federal AMT may still apply separately; Marcus needs a dual ledger, not a single “I moved so I'm done” story.

NSO vs ISO — California relocation friction (wage layer)

Recommended: Neither — plan both

| Feature | NSO | ISO (exercise year) |

|---|---|---|

| Wage income timing | Spread at exercise | CA often taxes spread at exercise; federal may defer wages |

| Day-ratio period (Pub 1004 style) | Grant → exercise | Grant → exercise for sourcing examples |

| Relocate before event | Lowers CA ratio if future work is out of state | Same ratio logic; AMT still complicates cash |

| Primary planning tool | Source-days calculator + W-2 reconciliation | Calculator + Form 6251 modeling |

Residents, nonresidents, and part-year returns

| Filing posture | California return | Equity wage income |

|---|---|---|

| Full-year resident | Form 540 | Worldwide wages; Schedule CA may adjust |

| Part-year resident | Form 540 + part-year schedule | Blend of resident worldwide + sourcing adjustments |

| Nonresident | Form 540NR | Only California-sourced wages |

Form 540NR is where many relocators first see California tax after leaving. Your W-2 Box 16 (state wages) may show California amounts even when you believe you are fully resident elsewhere—because payroll allocated using an employer ratio.

Withholding, estimated tax, and the cash-flow gap

California withholding on equity wages can use flat supplemental-style mechanics that do not equal your true 13.3% marginal exposure when Mental Health Services Tax applies. Federal 22% supplemental withholding has the same “cash flow ≠ liability” problem.

| Event | Risk |

|---|---|

| Large Q4 vest after moving | Too few pay periods to fix CA withholding |

| Multi-state W-2 | Box 16 totals may not match your calculated ratio |

| ISO exercise + AMT | Federal and CA cash needs diverge |

Position: For anyone with >$200k annual equity income and a mid-year relocation, modeling California-sourced dollars per grant in May–June (not April 15 only) is the right call—use the calculator outputs as inputs to estimated tax payments, not as filed numbers.

Steel-man: “I’m a remote worker now—California can’t touch me”

Best case for the skeptic: You established bona fide residency outside California, your employer reclassified payroll to another state, you perform zero California services after the move, and future grants are entirely earned in the new location. For new grants after the move, California sourcing should trend toward 0% if days are truly elsewhere and documentation is clean.

Why that story often fails for tech employees: Legacy grants still carry California workdays from years of HQ or hybrid work in the Bay Area. FTB Publication 1004 explicitly illustrates tax on nonresidents with majority California workdays in the grant-to-vest or grant-to-exercise window. Employers may continue to withhold California tax on vest until you prove a different ratio—anecdotally, payroll teams default to conservative California percentages until employees supply day schedules.

Rebuttal: Treat California equity sourcing rules as grant-specific ledgers. Each vest and each exercise gets its own denominator. Moving to Austin on 1 October does not erase January–September California days already baked into a March vest ratio.

Steel-man: “My employer already withheld California tax—I'm done”

Best case: Payroll used the correct grant-to-vest day ratio, your W-2 Box 16 matches FTB expectations, and you are not part-year resident in a way that triggers additional tax on worldwide income.

Why withholding ≠ liability: Withholding is a payment on account. If you were under-withheld after a late-year vest, you still owe estimated tax penalties even when you eventually file as a nonresident. If payroll over-withheld because it assumed 100% California sourcing after you moved, you need a refund claim on Form 540NR—not hope that Texas residency fixes it automatically.

Decision guide: relocation timing and documentation

Working checklist (relocation + equity)

Using the California Equity Source Days Calculator

The California Equity Source Days Calculator implements the linear ratio:

California-sourced equity wages = Total wage income × (CA service days ÷ Total service days)

Inputs:

- Equity income to allocate — RSU vest FMV or NSO spread dollars.

- California service days — days worked in California during the period.

- Total service days — denominator for the same period.

Limits (hedged): The tool does not know your employer’s payroll convention, ISO disqualifying facts, or credit ordering with other states. I haven't tested it against every equity administrator export (Carta, Schwab, E*TRADE)—your mileage will vary depending on whether HR counts PTO as workdays.

Pair results with relocating with equity for international moves and New York state tax on equity if you split time between coasts.

Verdict

For tech employees with legacy California workdays and future vests or exercises, California equity sourcing rules are not optional background noise—they are a grant-by-grant tax design problem. The winning workflow is boring: Publication 1004 period → day log → calculator ratio → W-2 reconciliation → 540/540NR with credits. Trying to time a move without running the ratio first is how people end up with a Texas driver's license and a California balance due on a single March vest.

Choose aggressive “vest after move” strategies only when your post-move service days will dominate the denominator and your employer will report accordingly—not because residency alone changes the formula.

Frequently Asked Questions

Do California equity sourcing rules apply if I work remotely from another state for the same employer?

Answer: If the services that earn the RSU or option were performed in California during the sourcing period, California can assert its ratio even if you later work remotely elsewhere. Remote work from Texas does not retroactively reclassify earlier California days. Document where you were physically performing services.

Source: FTB Publication 1004

What allocation period should I use for RSUs?

Answer: FTB Publication 1004 examples use the period from purchase/grant through vesting for restricted stock/RSU wage income. Your employer may use a different administrative convention—align your day log to their method before filing.

Source: FTB Publication 1004

I’m a California nonresident with a Texas W-2 address—do I still file in California?

Answer: If you have California-sourced wage income from equity (positive sourcing ratio), you generally need to file Form 540NR and report that income, then apply credits as applicable. Zero California-sourced income may still require a return depending on gross income thresholds—confirm annually.

Source: California R&TC §17951

How do ISO exercises interact with California sourcing when I relocate?

Answer: California often taxes the ISO spread as compensation for state tax purposes at exercise, while federal regular tax may differ. Sourcing still uses workday ratios over grant-to-exercise in Publication 1004-style examples, and federal AMT may require separate cash planning.

Source: FTB Publication 1004; IRS Topic 427

Can the California Equity Source Days Calculator file my return?

Answer: No. It is an educational allocation model. Use outputs in CPA meetings and estimated tax worksheets, not as a filed position.

Source: VestingStrategy tool disclaimer

Does selling RSUs after leaving California re-trigger wage sourcing?

Answer: The wage layer is generally fixed at vest. Later sales usually raise capital gain/loss questions based on residency at sale and basis—not a new grant-to-vest day ratio. Prior California sourcing on vest wages does not repeat on sale proceeds.

Source: IRS Publication 525; FTB Publication 1004

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| FTB Publication 1004 (Rev. 11-2023) | State guidance | ftb.ca.gov |

| California R&TC §17951 | Statute | leginfo.legislature.ca.gov |

| IRS Publication 525 (2025) | IRS | irs.gov |

| IRC Section 83 | Statute | law.cornell.edu |

| IRS Topic 427 — Stock options | IRS | irs.gov |

Figure 1: Service-day sourcing applies to the wage layer at vest or exercise—not only residency on the event date.

Disclaimer: This guide discusses general U.S. federal and California tax principles only and is not personalized tax, legal, or investment advice. Sourcing facts, employer reporting, and multi-state credits vary. Confirm with the sources cited and a qualified tax professional licensed in California and your residence state.

Research note: Editorial publish 25 May 2026 for california equity sourcing rules intent—allocation matrix sourced from FTB Publication 1004, integrated with the California Equity Source Days Calculator, and cross-linked to multi-state relocation guides.