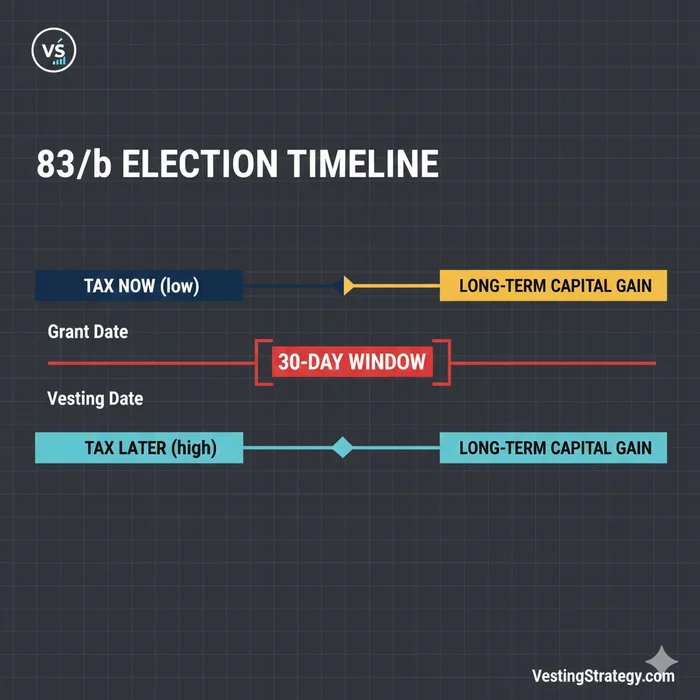

The IRS 83(b) election for restricted stock within 30 days must be an official, signed filing with the Internal Revenue Service—typically IRS Form 15620 (April 2025 revision) or a written statement that satisfies Treasury Regulation §1.83-2—mailed to the same IRS service center where you file your federal income tax return, with a copy furnished to your employer and a copy attached to your Form 1040 for the year of transfer. You have 30 calendar days from the Section 83 transfer date (not your offer letter date). Missing that window generally forecloses the election for that transfer.

This guide is the execution playbook for searches like irs 83b election restricted stock 30 days official: model language, mailing addresses, and Certified Mail compliance—not whether you should accelerate income (see strategic overview).

30calendar days — statutory filing window from property transfer (IRC §83(b))Verified against IRS Form 15620 instructions (April 2025), accessed 21 May 2026.

Who must file (and who should stop reading)

| Award / fact pattern | File an official §83(b) with the IRS? |

|---|---|

| Restricted stock transferred subject to vesting | Yes—if you elect within 30 days of transfer |

| Early exercise of options with unvested shares issued | Often yes—election tied to share transfer date |

| Classic RSUs (no stock at grant) | Usually no—see RSU ineligibility guide |

| Fully vested stock at transfer with no substantial risk of forfeiture | Generally unnecessary—different Section 83 path |

Section 83(b) election means you choose to include the bargain element in gross income at transfer instead of waiting for vesting under Section 83(a). The election is irrevocable once valid—model downside (forfeiture, company failure) before you mail.

Official filing package (what the IRS expects)

Treasury Regulation §1.83-2 and IRS Form 15620 align on the same factual disclosures. As of the April 2025 Form 15620 revision, the Service publishes a structured form; you may instead file a written statement that meets the regulation if every required fact is present.1

What counts as an official IRS 83(b) election for restricted stock?

A signed election filed with the IRS no later than 30 days after the property transfer date, stating that you elect under Section 83(b), describing the property and restrictions, and reporting fair market value (without regard to lapse restrictions), amount paid, and taxable year. IRS Form 15620 is the published format; a compliant letter can also work. You must furnish copies as the regulation requires and should attach a copy to your federal return for the transfer year.

Required contents (check against Form 15620 boxes)

| Item | Form 15620 box | Regulation concept |

|---|---|---|

| Legal name, TIN, address | Box 1 | Taxpayer identification |

| Property description & quantity | Box 2 | e.g., “25,000 shares of Class B common stock of Acme Robotics, Inc.” |

| Transfer date | Box 3 | Starts the 30-day clock |

| Taxable year of election | Box 4 | Year that includes Box 3 date |

| Restrictions (vesting, repurchase) | Box 5 | Substantial risk of forfeiture narrative |

| FMV at transfer (per share × qty) | Box 6 | Without regard to lapse restrictions per Treas. Reg. §1.83-3(i) |

| Amount paid | Box 7 | Purchase price / exercise price aggregate |

| Income amount (FMV − paid) | Box 8 | Compensation element you are accelerating |

| Service recipient (employer) | Box 9 | Optional on form but copy still required to employer2 |

Critical Warning: FMV must match your company’s 409A (private) or market price (public) methodology—Stock Administration and your CPA should sign off on the number before you ink the election.

Model language (Form 15620–aligned)

The IRS does not require magic words beyond electing under §83(b) and supplying the facts above. Practitioners often mirror Form 15620 so examiners see a familiar layout. Below is illustrative narrative structure—do not file without customizing numbers and names.

Election Under Section 83(b) of the Internal Revenue Code

The undersigned taxpayer hereby elects, pursuant to § 83(b) of the Internal Revenue Code,

to include in gross income as compensation for services the excess (if any) of the fair

market value of the property described below over the amount paid for the property.

1. Taxpayer: [Legal name], TIN [SSN/ITIN], [mailing address]

2. Property: [Quantity] shares of [class] common stock of [issuer legal name]

3. Date transferred: [MM/DD/YYYY]

4. Taxable year: [Calendar year 20XX]

5. Restrictions: [Vesting schedule; repurchase/forfeiture if employment ends]

6. FMV at transfer: $[X.XX] per share × [N] shares = $[total]

7. Amount paid: $[total exercise/purchase price]

8. Amount to include in gross income: $[Box 6 total minus Box 7 total]

Copies furnished to [employer legal name] as required under Treasury Regulation §1.83-2.

Signature: _________________________ Date: _________________________

For a fill-in draft, use the interactive tool on IRS 83(b) form generator & mailing checklist after your dates and FMV are locked.

Interactive Section 83(b) election letter (draft)

Fill in the fields below to generate election language aligned with the informational items commonly included under Treasury Regulation §1.83-2. This is not personalized tax advice — have a CPA or tax attorney review facts, valuation, and filing method before you file.

Taxpayer

Your TIN stays in this browser tab only — nothing you type here is sent to VestingStrategy servers.

Property & employer copies

IRS mailing address — verify before you seal the envelope

Treasury Regulation §1.83-2 requires filing with the Internal Revenue Service location where you file your federal income tax returns. The campus and ZIP+4 can change by tax year and filing category, so pull the address from the current IRS instructions for Form 15620 (PDF) or the "Where To File" tables in the Form 1040 instructions that match your residency and whether you are enclosing a payment.

On the envelope, many preparers write a routing line such as: ATTN: Section 83(b) Election — [Your name]

Certified Mail execution checklist (paper filing)

Toggle items as you complete them. Certified Mail is widely used to document the mailing date for IRS correspondence — it does not lengthen the statutory 30-day window.

Preview generated letter text

Election Under Section 83(b) of the Internal Revenue Code The undersigned taxpayer hereby elects under Section 83(b) of the Internal Revenue Code to include in gross income as compensation the excess (if any) of the fair market value of the property described below over the amount paid for such property, determined as of the date the property was transferred. 1. Name of taxpayer: [your legal name] 2. Address of taxpayer: [street, city, ST ZIP] 3. Taxpayer identification number: [SSN or ITIN] 4. Description of property with respect to which the election is made: [number of shares] shares of [class of shares] stock of [issuer legal name]. 5. Date on which property was transferred: [transfer date] 6. Taxable year for which election is made: 2026 7. Nature of restrictions to which the property is subject: [describe vesting, repurchase, forfeiture, etc.] 8. Fair market value at time of transfer (determined without regard to restrictions): [FMV per share on transfer date] 9. Amount paid for the property: [total amount paid for the shares] The undersigned taxpayer will file this election with the Internal Revenue Service office with which the taxpayer files their annual federal income tax returns no later than 30 days after the date the property was transferred to the taxpayer. Copies of this election have been furnished to the person for whom the taxpayer performed the services as required under Treasury Regulation §1.83-2(d): [employer / service recipient] [employer mailing address] Signature of taxpayer: ________________________________ Date signed: ________________________________ ( Sign and date after printing — ink signature typically required for paper filing )

Where to mail (IRS service center addresses)

Form 15620 instructions (April 2025) direct you to mail the completed election to the IRS office with which the person who performs the services files a federal income tax return.3 That means your Form 1040 “Where To File” address for the active tax year—not a random “Austin TX” meme from an old blog post. For a state-by-state mailing directory, certified-mail checklist, and expat ZIP (73301-0215 vs 73301-0002), see Where to Mail Your 83(b) Election: IRS Addresses.

Original research: tech-employee state → IRS campus (Form 1040, no payment enclosed)

Methodology: On 21 May 2026, we pulled the IRS “Where to file paper tax returns” tables for calendar year 2025 individual Form 1040 returns without an enclosed payment, for states that dominate U.S. tech equity grants. We normalized city/ZIP to three campuses. Always re-verify before sealing the envelope—IRS tables change.

| State (tech hubs) | IRS campus (1040, no payment) | ZIP+4 (representative) | Source row checked |

|---|---|---|---|

| California | Ogden, UT | 84201-0002 | CA 1040 |

| Washington | Ogden, UT | 84201-0002 | WA 1040 |

| New York | Kansas City, MO | 64999-0002 | NY 1040 |

| Texas | Austin, TX | 73301-0002 | TX 1040 |

| Massachusetts | Kansas City, MO | 64999-0002 | MA 1040 |

| Colorado | Ogden, UT | 84201-0002 | CO 1040 |

| Illinois | Kansas City, MO | 64999-0002 | IL 1040 |

| Florida | Austin, TX | 73301-0002 | FL 1040 |

| Georgia | Austin, TX | 73301-0002 | GA 1040 |

| New Jersey | Kansas City, MO | 64999-0002 | NJ 1040 |

Source: IRS Where To File — accessed 21 May 2026.

{

"@context": "https://schema.org",

"@type": "Dataset",

"name": "Section 83(b) IRS campus routing for tech-hub states (Form 1040, 2025 tables)",

"description": "Normalized IRS service-center destinations for paper Form 1040 filings without payment, used to route Section 83(b) elections mailed with Form 15620, as of May 2026.",

"creator": { "@type": "Organization", "name": "VestingStrategy.com Research" },

"datePublished": "2026-05-21",

"license": "https://creativecommons.org/licenses/by/4.0/",

"isAccessibleForFree": true,

"url": "https://www.vestingstrategy.com/guides/how-to-file-official-section-83b-election-with-irs/#dataset-83b-campus-routing",

"distribution": [

{

"@type": "DataDownload",

"encodingFormat": "text/html",

"contentUrl": "https://www.vestingstrategy.com/guides/how-to-file-official-section-83b-election-with-irs/#dataset-83b-campus-routing"

}

]

}

Envelope addressing tips:

| Line | Suggested text |

|---|---|

| Attention | Section 83(b) Election — [Taxpayer name] |

| Recipient | Department of the Treasury, Internal Revenue Service |

| City/state/ZIP | Campus from table above (match your residence) |

| Return address | Your mailing address (required for Certified Mail) |

Where I'm less sure—international addresses, ITIN-only filers, and military statuses sometimes route to specialized campuses; a one-line cover letter prepared by counsel beats guessing.

The 30-day deadline (official timing rules)

| Rule | Official source | Practical note |

|---|---|---|

| Clock starts | Transfer of property under Section 83 | Confirm date with Stock Admin in writing |

| Duration | 30 days | Calendar days—not “business days only” |

| Weekend/holiday on day 30 | IRC §7503 per Form 15620 instructions | Timely if postmarked next succeeding day that is not Sat/Sun/legal holiday4 |

| Extensions | None for late §83(b) in routine cases | Do not rely on “reasonable cause” folklore |

Use the 83(b) deadline & mailing tracker to compute last filing day and a mail-by buffer—we still recommend filing by day 25 when possible.

Certified Mail compliance (proof, not a deadline extender)

Certified Mail does not extend the 30-day substantive window—it creates third-party evidence that USPS accepted your envelope on a particular date. That matters because IRC §7502 can, in qualifying U.S. Postal Service mailings, treat a timely postmark as timely filing even if IRS processing arrives later—fact patterns get litigated; do not treat social media as authority.5

Filing proof methods for Section 83(b) elections

Compared for a U.S. employee mailing a paper election near the statutory deadline (May 2026 practitioner norms).

| Attribute | USPS Certified Mail | USPS Priority Mail | Hand delivery to campus |

|---|---|---|---|

| Third-party acceptance timestamp | Strong (PS Form 3800) | Tracking only | Varies—get stamped receipt if available |

| IRC §7502 postmark analysis | Commonly relied on | Validate with counsel | Different rules |

| Cost (approx.) | ~$4–$8 + postage | ~$10–$20 | Travel cost |

| Our default recommendation | Yes for most employees | Only with CPA sign-off near deadline | Rare |

Post office script (copy/paste)

# At USPS counter (illustrative — confirm fees at post office, May 2026)

# 1. Place signed original election + optional cover sheet in envelope

# 2. Request "Certified Mail" + "Return Receipt" (electronic PDF if offered)

# 3. Keep PS Form 3800 receipt; photograph envelope with label visible

# 4. Export tracking PDF same day; store with duplicate signed PDF

Deep dive on postmarks vs. receipt: Official 83(b) 30-day deadline & mailing rules.

Worked example: Priya, early exercise at Databricks (illustrative)

Facts (hypothetical, rounded): Priya is a senior software engineer in California. On 3 March 2026, she early-exercises 40,000 ISOs; the company issues 40,000 unvested common shares the same day. Stock Admin confirms Section 83 transfer date = 3 March 2026. 409A FMV = $4.10/share; exercise price = $0.42/share.

| Step | Priya’s action | Deadline |

|---|---|---|

| 1 | Email Stock Admin: confirm transfer date | 3 Mar 2026 |

| 2 | CPA signs off FMV $4.10; compute income (4.10 − 0.42) × 40,000 = $147,200 | By 25 Mar |

| 3 | Sign Form 15620; duplicate wet-ink copy | By 25 Mar |

| 4 | USPS Certified Mail to Ogden, UT campus (CA 1040 table) | Postmark ≤ 2 Apr 2026 (30th day) |

| 5 | Upload employer copy to equity portal + email confirmation | Same week |

| 6 | Flag CPA to attach copy to 2026 Form 1040 | Tax season 2027 |

Verdict for Priya: File official Form 15620 language—do not rely on a random Notion template. If she misses 2 April 2026 postmark (with §7503 adjustment if applicable), she should assume no §83(b) for that transfer and call counsel immediately—AMT and withholding surprises compound fast after early exercise.

Steel-man: “I can DIY the official filing in an afternoon”

Best case for DIY: You have a single grant, Stock Admin already sent a company-approved 83(b) packet, FMV is trivial (nominal par value), and you are 10+ days before the deadline. Certified Mail plus Form 15620 is mechanically simple; the IRS really does process these every day.

Where DIY breaks: Multi-state moves mid-window, ITIN issuance, divorce community-property quirks, or underpayment penalties when accelerating $100k+ of phantom income. Anecdotally, the expensive mistakes we see in forums are wrong transfer dates and wrong campuses—not missing signature lines.

Our position: DIY mailing is fine for straightforward restricted stock grants if a CPA reviews FMV and restrictions first. Spend professional fees when the bargain element exceeds roughly $25,000 or when ISO/AMT interacts with early exercise—choose counsel over another hour of Reddit.

Working checklist (printable)

Copies and return attachment

| Copy | Recipient | Timing |

|---|---|---|

| Original | IRS service center | ≤ 30 days from transfer |

| Duplicate | Employer / service recipient | Contemporaneous with IRS mailing |

| Duplicate | Your permanent tax records | Same day |

| Duplicate | Attached to Form 1040 for transfer year | Per Treas. Reg. §1.83-22 |

Related guides (pick your layer)

| Need | Guide |

|---|---|

| Deadline math + mail-by buffer | 83(b) deadline & mailing tracker |

| Draft letter + checklist | IRS 83(b) form generator |

| Postmark law (IRC §7502) | Official 30-day deadline & mailing rules |

| Step-by-step filing playbook | How to file a Section 83(b): step-by-step |

| Step-by-step (shorter) | How to file within 30 days |

| Economics / risk | Strategic tax decision |

| RSU trap | Why RSUs usually cannot use 83(b) |

Verdict

For employees searching official filing instructions: treat Form 15620 + correct IRS campus + Certified Mail proof + employer copy as the non-negotiable bundle. File early in the window, verify addresses on IRS.gov for the active tax year, and escalate to a tax attorney when you are on day 28–30 or when accelerated income exceeds your cash on hand. Strategy without execution is worthless; execution without FMV validation is dangerous.

Primary sources

| Authority | Link |

|---|---|

| IRC §83(b) | 26 U.S.C. §83 |

| Treas. Reg. §1.83-2 | 26 CFR §1.83-2 |

| IRS Form 15620 (Apr 2025) | |

| IRS Pub. 525 (restricted property) | IRS.gov |

| IRC §7502 (timely mailing) | 26 U.S.C. §7502 |

| IRC §7503 (weekends/holidays) | 26 U.S.C. §7503 |

Footnotes

Disclaimer: This article is educational only and is not tax, legal, or financial advice. Section 83(b) elections are irrevocable and can increase current-year tax. Confirm transfer dates, FMV, mailing addresses, and payment obligations with a qualified CPA, enrolled agent, or tax attorney before filing.

Footnotes

-

IRS Form 15620 instructions (April 2025) permit Form 15620 or a written statement satisfying Treas. Reg. §1.83-2. ↩

-

Treas. Reg. §1.83-2 describes filing, furnishing copies, and attaching a copy to the income tax return for the year of transfer. ↩ ↩2

-

Form 15620 “Where to File” — mail to the IRS office where the taxpayer files federal income tax returns. ↩

-

Form 15620 “When to File” — IRC §7503 if the 30th day falls on Saturday, Sunday, or legal holiday. ↩

-

IRC §7502 and Treas. Reg. §301.7502-1 — timely mailing treated as timely filing under statutory conditions. ↩