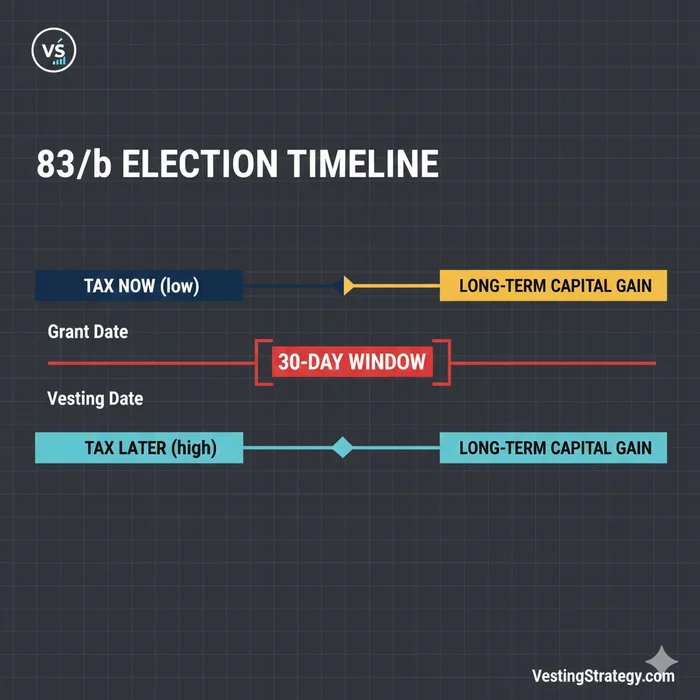

The IRS 83(b) election 30 days rule means you must file a written Section 83(b) election no later than 30 calendar days after the date property is transferred to you—not 30 business days, and not 30 days from when you “feel ready.” For restricted stock and early-exercised unvested shares, that transfer date is the anchor every calendar, Certified Mail receipt, and employer copy must match. Miss the window and you generally cannot obtain Section 83(b) timing for that transfer; there is no routine IRS extension.

This page is built for procedural proof: an interactive deadline calculator, a mail-by buffer, copy-paste Certified Mail instructions, and checklists you can execute the same day Stock Admin confirms your transfer date. For deadline math plus a completed election letter PDF, use the dedicated Section 83(b) Election Deadline Calculator.

83(b) deadline & Certified Mail tracker

Enter the Section 83 transfer date Stock Administration confirms (not board approval date). The calculator counts 30 calendar days after transfer—the same window described in IRC §83(b) and Treasury Regulation §1.83-2.

Select a transfer date to see your last day to file and a recommended mail-by date (five calendar days before the deadline).

IRS mailing address — verify on IRS.gov before you seal

Treasury Regulation §1.83-2 requires filing with the Internal Revenue Service office where you file your federal return. Pull the ZIP+4 from the Form 15620 PDF instructions or the active Form 1040 Where To File table for 2026. Profile selected: I file Form 1040 in the U.S. (no special status).

Certified Mail instructions (copy to your checklist)

- At the post office, request USPS Certified Mail® with Return Receipt (or electronic Return Receipt) for the IRS original.

- Outer envelope routing line (example): ATTN: Section 83(b) Election — [Your legal name]

- Inside: signed original election (Form 15620 or equivalent), optional cover sheet.

- Retain the Certified Mail receipt and export/save the tracking barcode PDF the same day.

- Section 83 transfer date on file: [transfer date]. Statutory filing deadline (30 calendar days after transfer): [IRS deadline].

- Furnish the employer/service-provider copy separately and keep proof of delivery (portal screenshot or certified mail).

Execution checklist

Educational tool only. Calendar math follows the common practitioner reading of “30 days after transfer” as 30 calendar days. Confirm counting conventions, electronic filing options, and Section 7502 postmark facts with your CPA or tax attorney.

Why deadline anxiety shows up in search (and what actually fixes it)

Google queries like “irs 83(b) election 30 days” rarely ask for theory. They ask: What is my last day? Does Saturday count? If I mail Certified on day 29 but IRS scans on day 32, am I OK? Which ZIP code?

Strategy articles explain whether to elect. This tracker answers whether you still have time and how to document mailing if you do.

| Reader fear | What this tracker supplies |

|---|---|

| Wrong start date | Forces confirmation of transfer date, not grant approval |

| Off-by-one counting | Calendar math with explicit last filing day |

| Postmark vs. receipt | Links to IRC §7502 concepts and when to call counsel |

| Envelope roulette | Checklist + official instruction links for current-year addresses |

| “I mailed something” | Checkbox trail for receipts, employer copy, and return attachment |

Critical Warning: Section 83(b) elections are irrevocable once valid. Accelerating income without a validated election can create catastrophic tax mismatches if shares later forfeiture or the company fails. Model downside cases before you mail—not after.

The transfer date: the only input that matters

Treasury Regulation §1.83-2 ties the election to property transferred subject to a substantial risk of forfeiture. Practically, that means the date your company’s records show you received restricted shares (or shares from an early exercise), not:

| Date people guess | Usually wrong for the 83(b) clock? |

|---|---|

| Board approval of the grant | Often yes—approval can precede issuance |

| Offer letter “grant date” | Often yes—language may not match transfer |

| Exercise request submitted | Often yes—transfer may occur on settlement |

| Payroll “grant ID” in portal | Verify—may be informational only |

Action: Email Stock Administration: “What is the Section 83 transfer date that starts my 83(b) window for [grant ID]?” Save the reply PDF in your equity folder.

Does the IRS 83(b) election deadline use calendar days or business days?

Tax professionals generally read IRC Section 83(b) and Treasury Regulation §1.83-2 as requiring filing within 30 calendar days after the transfer date. Weekends and federal holidays do not automatically push the deadline to the next business day for every delivery method. If your last day falls on a Sunday, mail earlier in the week with Certified Mail rather than assuming a Monday extension.

How the calculator counts your 30-day window

The tracker adds 30 calendar days to the transfer date you enter. That matches how most practitioners operationalize “within thirty days after the date of transfer” for planning purposes.

Example:

| Event | Date |

|---|---|

| Section 83 transfer (confirmed) | March 15, 2026 |

| Last day to file (transfer + 30 days) | April 14, 2026 |

| Recommended mail-by (5-day buffer) | April 9, 2026 |

If you receive shares on January 31, adding 30 calendar days lands on March 2 (not “one month later” by eyeballing). Always let software count—especially across February.

The mail-by buffer is not a law; it is logistics. Certified Mail lines, post office hours, weather, and the risk of debating Section 7502 on your actual last day all argue for filing before day 30.

Certified Mail: what to do at the post office (step-by-step)

The Internal Revenue Code does not require Certified Mail. Employees use it because it creates third-party evidence of when USPS accepted the envelope—useful if IRS processing timestamps arrive later than your postmark.

| Step | Detail |

|---|---|

| 1 | Print two wet-ink signed originals: IRS + permanent file (plus scans) |

| 2 | Confirm IRS address from current Form 15620 PDF or Form 1040 “Where To File” |

| 3 | Outer label routing line, e.g. ATTN: Section 83(b) Election — [Name] |

| 4 | Request USPS Certified Mail with Return Receipt (or electronic Return Receipt) |

| 5 | Pay, retain the receipt, photograph it, export tracking PDF same day |

| 6 | Furnish employer copy separately; keep portal screenshot or mail proof |

The tracker above generates a numbered Certified Mail script you can copy into Notes or email to counsel.

IRC Section 7502: postmark vs. IRS receipt (high level)

Timely mailing treated as timely filing under IRC §7502 can, for qualifying U.S. Postal Service mailings, treat a document as filed on the postmark date even if the IRS receives it later—when statutory and regulatory conditions are met.1

| Concept | Plain-language takeaway |

|---|---|

| Postmark on or before deadline | May protect timely filing for qualifying USPS mail |

| IRS receipt after deadline | Not automatically fatal if §7502 applies |

| Private carrier tracking | Analyzed differently—do not assume USPS outcomes |

| Day-30 heroics | Call a CPA or tax attorney before relying on edge cases |

Important: Section 7502 disputes are fact-specific. This article explains why employees buy Certified Mail—not a guarantee your facts win an audit.

Employer / service-provider copy (separate workstream)

Treasury Regulation §1.83-2 expects you to furnish a copy to the person for whom you performed services (typically your employer).2

| Task | Evidence to keep |

|---|---|

| Upload to equity portal | Screenshot with timestamp + ticket number |

| Email to Stock Admin | Sent folder PDF + read receipt if available |

| Physical mail to company | Certified Mail or courier proof |

Missing the employer copy is not interchangeable with missing the IRS copy. If you discover an omission, do not improvise retroactive fixes—escalate to counsel and Stock Admin.

Pair this tracker with the rest of your filing stack

| Stage | Resource on VestingStrategy |

|---|---|

| Should I elect? | Section 83(b): strategic overview + 83(b) break-even tool |

| Draft the letter | IRS 83(b) form generator & mailing checklist |

| Operational filing steps | How to file an 83(b) within 30 days |

| Deep mailing law | Official 83(b) 30-day deadline & mailing rules |

| Award-type traps | Why you cannot file 83(b) on standard RSUs |

Early exercise and founder shares: same clock, higher stakes

Early-exercised unvested option stock and founder restricted stock use the same 30-day window measured from share transfer. The dollars at risk differ:

| Profile | Why deadline proof matters more |

|---|---|

| Founder | FMV may stay low at transfer—but forfeiture without a valid election still hurts |

| Early exercise (NSO/ISO) | AMT and payroll taxes may accompany the election year |

| Late-stage RSA | FMV may be material—estimated tax payments spike |

Read early exercise strategies for exercise timing, then return here to freeze the transfer date before you sign paperwork.

International and ITIN filers: same 30 days, extra envelope discipline

Nonresident or ITIN taxpayers still face the federal 30-day requirement for U.S. Section 83 property. Additional wrinkles include:

- Address lines on Form 1040 instructions vs. actual residency

- Cover letters explaining ITIN status when counsel recommends

- Employer withholding systems that may not know you filed until you forward proof

See Section 83(b) for expats for jurisdictional context—then use this tracker for U.S. mailing proof.

What happens if the tracker shows “past deadline”

| Scenario | Typical tax outcome (high level) |

|---|---|

| No election filed within 30 days | Income generally follows Section 83(a) timing (often at vesting/forfeiture lapse) |

| Election postmarked day 31 | Usually invalid for that transfer in routine practice |

| You discover the miss years later | No standard DIY cure—counsel may discuss PLR paths (expensive, uncertain) |

Emotional but true: Intent does not extend statutory windows. Calendar discipline is cheaper than forensic postmark litigation.

If Certified Mail shows delivery after day 30 but I mailed on day 29, is my 83(b) election valid?

Sometimes a timely USPS postmark can support timely filing under IRC Section 7502 even if IRS processing occurs later—but the analysis is fact-specific and can be contested. Preserve the post office receipt, Certified Mail label, and tracking exports, then involve a qualified tax professional immediately. Do not assume social-media anecdotes match your envelope facts.

Records to keep for seven-plus years

Audits and company diligence rarely question your election in the grant year—they question it at exit, IPO, or acquisition when basis and capital gains storytelling matter.

| Document | Why retain it |

|---|---|

| Stock Admin email confirming transfer date | Proves which 30-day window applied |

| Certified Mail receipt + barcode PDF | Postmark / Section 7502 defense package |

| Scanned signed election (IRS + file copy) | Shows content actually mailed |

| Employer copy proof (portal / mail) | Shows Reg. §1.83-2 copy step |

| Form 1040 as filed with election attached | Confirms return-year attachment |

| 409A / FMV support for grant date | Corroborates bargain element you elected into |

Store a single folder (cloud + offline) labeled 83(b) – [Company] – [Grant ID] – [Year]. Future you—and your CPA—should not reconstruct facts from memory.

State taxes and payroll: deadline success is not the whole bill

Filing on time solves federal timing under Section 83(b). It does not automatically solve:

| Layer | What still requires planning |

|---|---|

| State income tax | Some states conform to federal 83(b); others have sourcing quirks for movers |

| Estimated taxes | Bargain element may require quarterly payments the same year |

| Payroll reporting | Employers may not update systems until you forward proof |

| AMT (ISO early exercise) | Parallel AMT projection—see AMT planning |

California residents and recent movers should read New York / state equity guides when workdays span multiple jurisdictions in the grant year.

Electronic filing: do not assume e-file replaces mail without counsel sign-off

IRS publishing cycles occasionally expand digital pathways for Form 15620. Operationally, many employees still:

- Print and sign a paper election

- Mail the IRS original with proof

- Attach a duplicate to the paper or e-filed Form 1040 per preparer workflow

If your CPA confirms an IRS-authorized electronic submission for your tax year, follow their checklist exactly—do not duplicate-mail unless instructed. When in doubt, default to paper + Certified Mail + this tracker’s receipts.

Treat Stock Admin’s transfer confirmation as the first deliverable in your 30-day sprint—without it, every online calculator (including this one) is only guessing.

Pre-flight checklist (print or copy to Notes)

- Stock Admin confirmed Section 83 transfer date in writing

- Tracker shows last filing day and mail-by dates in your calendar

- Election drafted (form generator) and reviewed by CPA/counsel

- Two wet-ink originals printed; scans saved

- IRS address verified on current IRS PDF for this tax year

- USPS Certified Mail receipt + tracking PDF stored

- Employer copy delivered with timestamped proof

- CPA flagged to attach election to the correct Form 1040 year

Related reading

- IRS 83(b) Election Form Generator & Mailing Checklist — draft election language

- The Official 83(b) Election 30-Day Deadline & Mailing Rules — IRC §7502 depth

- How to file a Section 83(b) election within 30 days — required statement contents

- Restricted Stock Awards (RSAs) tax guide — when 83(b) is common

- AMT planning for stock options — ISO/AMT after early exercise

Footnotes

Primary sources

| Source | URL |

|---|---|

| IRC Section 83(b) | Cornell LII |

| Treasury Regulation §1.83-2 | Cornell LII CFR |

| IRC Section 7502 | Cornell LII |

| IRS Form 15620 | IRS PDF |

| IRS Publication 525 | IRS.gov |

Disclaimer: This guide and interactive tracker are educational only and are not tax, legal, or financial advice. Section 83(b) elections are irrevocable, accelerate income, and interact with AMT, payroll taxes, state taxes, and immigration status. Confirm transfer dates, addresses, delivery methods, and counting conventions with a qualified CPA, enrolled agent, or tax attorney before you mail or upload anything.